Back in May, I wrote about upmarket fashion firm Burberry (LON:BRBY) and explained why I’d like to add it to the SIF Folio. Only my rules prevented me at the time - the shares weren’t quite cheap enough.

Fast forward four months and the situation has altered slightly. As I haven’t added a stock to the portfolio for four weeks, my rules allow me to relax my valuation criteria slightly. You can see the relaxed version of my buying screen here.

Burberry is now a possible buy, despite the uncertainty triggered by the departure of its chief executive.

However, there’s also a second contender that I must consider this week. FTSE 250-listed Coats (LON:COA) has recently appeared in the results of my primary buying screen. This £1.3bn group is a 200-year old British manufacturing business that appears to have made the transition successfully to the 21st century.

Coats describes itself as the world’s leading industrial thread company. It’s one of the world’s largest suppliers of threads and zippers. In addition to serving the fashion and footwear industries, it produces industrial products used in sectors such as automotive manufacturing and telecoms.

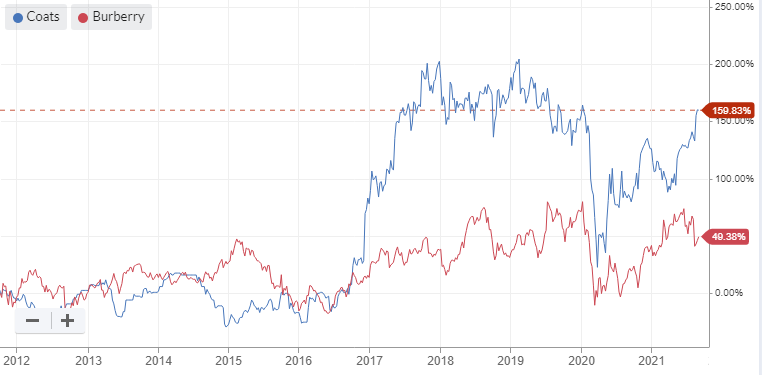

It may seem illogical to consider buying a capital-intensive volume manufacturer instead of a luxury brand. I understand this view. But the reality is that Coats has outperformed Burberry over the last decade by a considerable margin:

So, I’ll look at Coats this week - if I’m happy, I’ll add the shares to SIF. If I’m not, then Burberry might get the green light.

Coats (LON:COA) - a quick recovery

Coats’ inclusion in my screen seems to have been triggered by the group’s half-year results on 3 August. These came shortly after a guidance upgrade on 14 July and revealed that the company’s half-year performance was broadly in line with the first half of 2019.

Revenue: $732m (+4% vs H1 2019)

Operating profit: $97m (-4% vs H1 2019)

Adjusted operating margin: 13% (H1 2019: 14.5%)

Dividend reinstated

The focus for the remainder of the year appears to be on profitability. This seems logical to me given that profits have lagged revenue growth so far this year. The main problem area seems to be the group’s US operations, which are suffering from labour…