It’s the end of November, so it’s time to review stocks added to the SIF Portfolio six months ago, in May. Stocks that no longer qualify for my screen may now be sold. Stocks which continue to qualify will be held, and then reviewed on a monthly basis.

Such frequent trading goes against the grain for many investors, including me. When the portfolio reaches its first anniversary, I may consider extending the six-month minimum holding period, but for now, I’m sticking to the rules. After all, there’s no point in running a rules-based portfolio if you keep changing the rules. Frequent changes make it impossible to say whether any of the rules actually work.

Here’s a list of the four stocks which are under review this week. Each company name is linked to my original article on the company:

- Gold miner Pan African Resources

- Pharma giant GlaxoSmithKline

- Concrete flooring specialist Somero Enterprises

- Packaging group Macfarlane

Pan African Resources

At one point this year, Pan African Resources was the biggest riser in the portfolio. That’s not the case anymore. Pan African’s share price has pulled back with the price of gold, which has fallen by 13% from its 2016 high of $1,375/oz.

Despite this, the SIF portfolio’s holding in Pan African is still worth 25% more than it was six months ago. That’s not a bad performance.

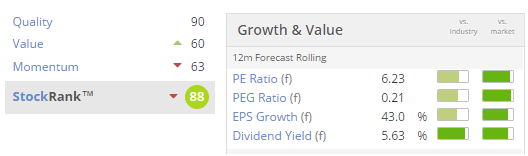

What’s more interesting is that Pan African still qualifies for my screen, so will remain in the portfolio. Although the StockRank has fallen from 98 to 88, Pan African is still highly ranked for quality and looks cheap on current year forecasts:

I have a fairly neutral view on the outlook for gold, but Pan African has performed well this year and further gains may be possible. I’m happy to keep this stock in the portfolio.

Verdict: Hold

Total return so far: +25%

GlaxoSmithKline

GlaxoSmithKline is a relative outlier among the stocks in the SIF Portfolio. It’s both defensive and a big cap stock.

After six months in the portfolio, the pharma giant’s shares have risen by just 2.1%. However, it has provided some welcome defensive quality, plus cash dividends totalling 38p per share. This represents a 2.6% yield on my purchase price of £14.74 per share, pushing the total return on this investment…