This article was written by regular contributor Anton Crabbe. You can read his bio here

Sigma Healthcare (ASX:SIG) are a full line pharmaceutical wholesaler and distributor. They also have a network of independent and franchised pharmacies and healthcare providers across Australia.

SIG have experienced changes over the past decade however recently have been focused on improving their business operationions through IT upgrades, increased warehousing capacity, brand consolidation, and sale of non-core assets.

However when coupled with COVID supply issues, this has led to business disruptions, loss of market share and unfortunately resulted in a net loss in FY22. That considered, it is starting to look like the restructure and streamlining strategy is bearing fruit in FY23, with the company reporting a small net income figure of $3.3m and paying a final dividend of 0.5 cents, fully franked.

As mentioned, FY23 was a busy year for SIG, with the upgrade of their distribution centres and IT systems being completed. Further, they commenced the amalgamation of Amcal and Guardian pharmacy brands, ceased their loss making Cura operations and sold their Wholelife hospitals for $44m.

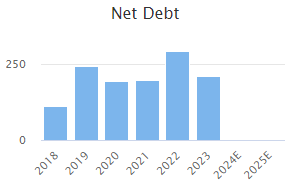

What was encouraging to see was that despite all this, SIG increased reported revenue by 6.2 per cent to $3.7B, whilst also improving margins and cash flow. Furthermore, they reduced Net Debt from the high figure six months ago, but it is still elevated. (more on that in a moment.)

Health, medical and hospital spending continue to increase. This is a huge market and has strong long-term tail winds driven by an aging population and changing health policies. Ideally, if the efficiencies and improvements SIG have recently made continue, SIG are in a prime position to capitalise on these strong sector tailwinds. Adding to this, SIG are planning to enter the higher margin ‘health, beauty and wellness’ product categories and increase their own label offering.

Stock Rank:

Since SIG released their annual FY23 report on 23rd March, their Quality and Value ranks rose on the back of the turnaround in business performance. But it looks like the Momentum rank has decreased more significantly despite a relatively stable price. This is on the back of the Analysts cutting their EPS targets…