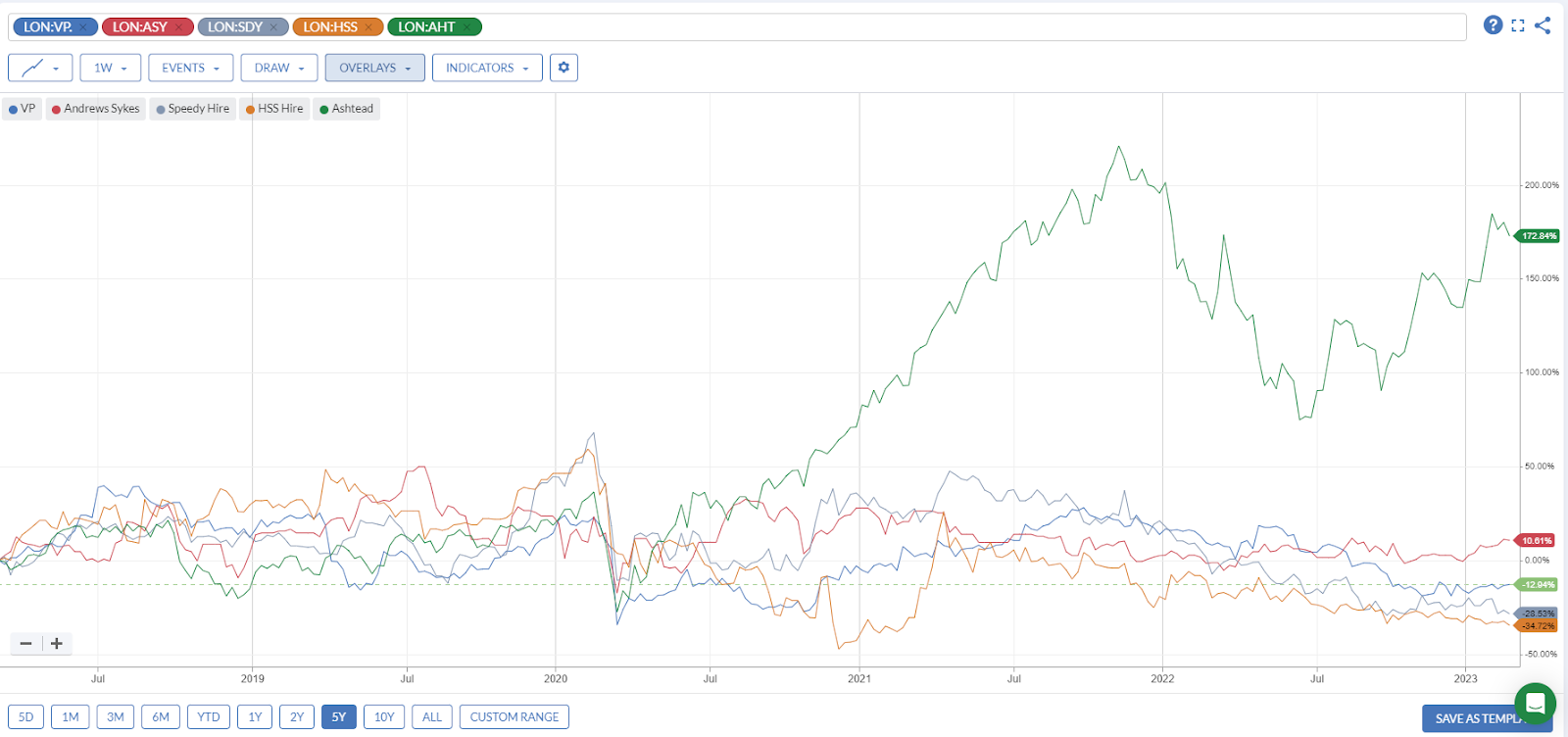

Two things piqued my interest in the small cap hire sector. The first was that HSS Hire (LON:HSS) featured in the screen results from my Price-to-Sales screen. The second was that, since COVID hit, all of the small caps, Andrews Sykes (LON:ASY) HSS Hire (LON:HSS) Speedy Hire (LON:SDY) and VP (LON:VP.) have massively underperformed Ashtead (LON:AHT) , which is the behemoth in the sector:

The majority of Ashtead’s business is in the US, so this isn’t a direct comparison. (Although several of the smaller firms have US, European or Middle Eastern operations too.) However, it is clear that there has been a step change in the perception of the businesses post-COVID, with Ashtead now trading at a significant premium to the smaller listed companies:

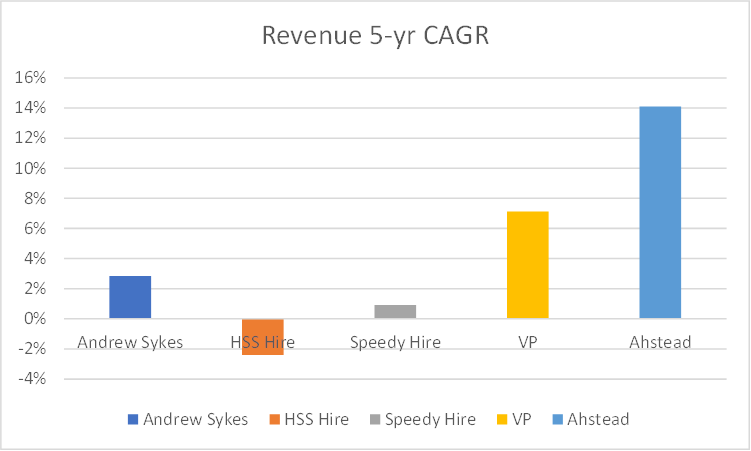

Part of this is justified. Ashtead has had much better revenue growth over the last five years:

The story for EPS growth is the same (excluding HSS Hire (LON:HSS) , where the figures are flattered by a poor starting year):

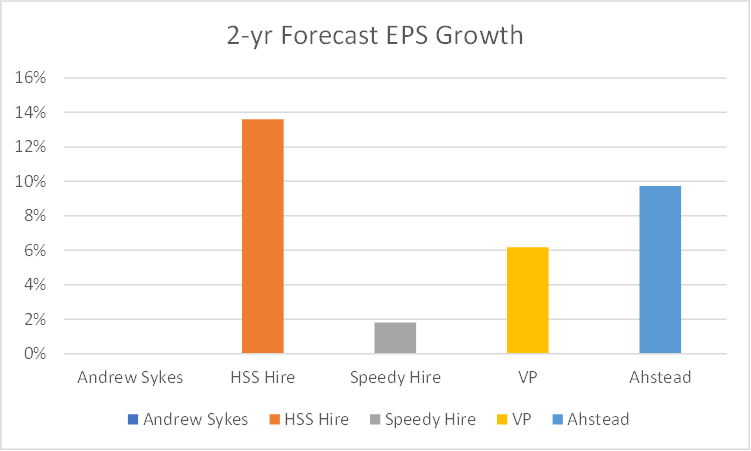

However, if brokers’ forecasts are to be believed, the picture going forward is more mixed:

And further into the future:

(Andrews Sykes has no broker forecasts, hence the lack of values.)

It is only worth paying a high multiple for a company if it will grow earnings rapidly in the future. While history may provide a guide to which companies can do this, the value investor tends to bet on mean reversion over the long term rather than continued momentum. If the rating disparity closed in the future, it would benefit these smaller companies.

In many industries, such as recruitment, the larger companies generate higher margins and are much more highly rated by the market because they benefit from network effects. However, there doesn’t seem to be the same effect at play here. AMA Research describes the sector as” extremely competitive and relatively fragmented”. For example, Statista shows that in 2021 Sunbelt (i.e. Ashtead) had just a 9% UK market share, with Speedy Hire at 7%…