Good morning, it's Paul here with Monday's SCVR.

Please see the article header for the companies I'll be reviewing today, which have issued trading updates or results.

Estimated timings - I lost the section on PURP, so had a re-create it from memory. Hence running a bit late. Should be finished by 3pm. Update at 15:42 - today's report is now finished.

.

Hammerson (LON:HMSO)

Share price: 58.3p (down 9% today, at 10:45)

No. shares: 766.3m

Market cap: £446.8m

- Considering a rights issue.

- In advanced discussions to sell its 50% stake in VIA Outlets.

- Approved for£300m loan from Bank of England (CCFF scheme)

- Q3 rent collection improved to over 30% (still sounds awful)

My opinion - this share looks finely balanced, so I'm watching from the sidelines. I held it recently, but sold out once it became clear that the economics of its shopping centres don't work unless footfall returns to normal, and tenants can pay rents that are far too high for market conditions. Nobody knows what the new normal will be though. Hence I feel it's almost impossible to value this share at the moment.

Bigdish (LON:DISH)

(I'm long)

Another day, another operational update!

TGI Fridays has joined its ordering app, as have 500 more M&B sites. Therefore the 1250 new sites announced recently, has become 1850. Seems to be gaining traction in terms of restaurant recruiting. The platform is free at present. Needs to raise more funds this autumn.

Tekmar (LON:TGP)

Share price: 110p (down 3.5% today, at 10:56)

No. shares: 51.3m

Market cap: £56.4m

(I'm long)

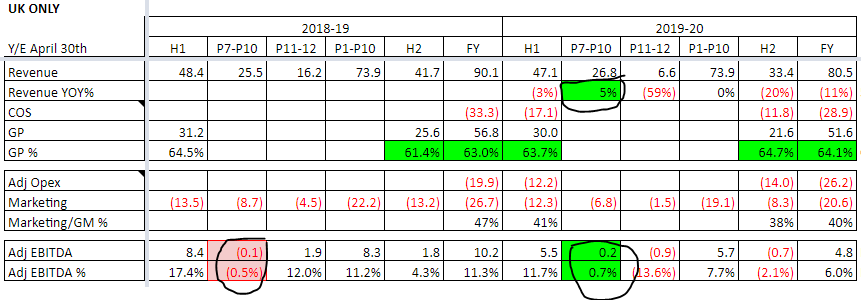

Tekmar Group (AIM: TGP), a leading provider of technology and services for the global offshore energy markets, announces its final results for the year ended 31 March 2020 ("FY20" or the "Period").

I did some research on this company earlier this year, and like the look of it. It's a profitable supplier of niche products mainly for the offshore wind farm sector - cable protectors. It's also diversified into other subsea markets (oil & gas, less than 20% of revenues), and growth is both organic and by acquisition. This is a good growth area. Performance was dented by covid, but the figures overall look quite decent to me in the circumstances.

Our trading update stated we expected…