Good morning from Paul & Graham!

Apologies for the lack of a podcast this weekend, the creative juices dried up I'm afraid.

Agenda

Paul's Section:

Fulcrum Utility Services (LON:FCRM) - a disastrous convertible loan refinancing, which effectively means the shares are now worth 0.5p or less. The market price of 3.4p should therefore require an immediate ditching of this share, for anyone holding. I'm reporting on this, because it's a warning of what might happen at other companies which need funding at a time when the market is not interested in funding anything that isn't performing well.

Equals (LON:EQLS) - another positive trading update, from this forex services business, with FY 12/2022 forecasts now likely to be beaten c.10% at the revenues line, which could have a nice operationally geared boost to profits. Although I question the adjustments to profit, and large capitalised development spending, so this area needs further research. Overall though, looks well worth a closer look.

RBG Holdings (LON:RBGP) - a profit warning, but from a specific division called LionFish. The core business is performing well. So should we look through this warning as an isolated problem (the best type of profit warning)? Possibly, but a £20m loan on RBGP's balance sheet seems to be specifically linked to LionFish, and it might take time to wind down this operation, which sounds like it's on the cards. Overall, it's difficult to assess risk:reward without more information. So I'm neutral for now, but will keep an eye on it, as there's a possibility of a recovery.

Graham's Section:

A G Barr (LON:BAG) (£560m) - Barr’s announces a £20m acquisition, possibly rising to £32m in two years. It picks up a small Leeds-based drinks company, Boost, that includes the well-known Boost Energy drink. Although the RNS doesn’t tell us the exact conditions required in order for the full £32m to get paid, this still strikes me as a good deal for Barr’s, whose strong balance sheet enables them to use their own cash to fund the deal.

Lindsell Train Investment Trust (LON:LTI) (£213m) - this trust confirms that H1 was a difficult period. It outperformed the MSCI World Index in terms of total return, with the help of a dividend, but its major holding (Lindsell Train Limited, the fund management company) continued to suffer outflows and a reduction in AuM. Manager Nick Train admits that he “must work harder than usual to maintain my native optimism”. I like the investment approach here and wouldn’t worry too much about temporary underperformance. The investees, including LTL, look like great companies to me and I would sleep soundly at night owning them.

Explanatory notes -

A quick reminder that we don’t recommend any stocks. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps up to about £700m. We avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech).

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to.

Paul’s Section:

Fulcrum Utility Services (LON:FCRM)

3.4p (pre market open)

Market cap £14m

Convertible Loan Facility Agreement

The warning signs were previously communicated to the market, which I covered here on 24 Oct 2022 - an admission that the company needed more funding and was in talks with its major shareholders (Harwood Capital, and Bayford & Co, combined owning 58%).

Today’s £6m convertible loan looks onerous, and with a conversion price of a maximum of 0.5p, this could lead to up to 1.2bn of new shares being issued (quadrupling the share count, currently at 399m).

Interest is at 20% p.a., and there are other fees.

Minority shareholders are assured they will be given an open offer at the conversion price.

My opinion - this is a disaster, and an admission that the existing equity is almost worthless.

For that reason, if I held, I’d ditch the lot (if possible) on the opening bell.

It’s another reminder (which is why I’m reporting on it here) that the funding window has slammed shut for small, problem companies. Therefore major shareholders can do what they want, and provide funding on onerous terms, which destroy the value in the existing shares. Hence it makes sense to sell this type of share, salvaging whatever you can, before a bombshell refinancing on onerous terms is announced. Or worse of course (insolvency).

I think it’s a good idea to have a rule that, whenever a company reports it needs more funding, immediately hit the sell button. Conditions are now very bad for small companies needing refinancing.

Harwood Capital often de-lists shares too, so I imagine that could be the next bombshell facing FCRM. It hasn’t worked, so time to just move on. This is a reminder to all of us, to review our portfolios for companies which might need extra funding - the terms of any funding could be disastrous for existing small shareholders, as FCRM looks to be.

It's a reminder that having one or two major shareholders that control the company, increases risk for small shareholders. Harwood Capital seems a particularly aggressive fund that I'm increasingly wary of, if I see it with a large % shareholding at any company.

Equals (LON:EQLS)

97p (up 3% at 08:32)

Market cap £174m

I know there’s a fair bit of reader interest in this company, providing forex services. Its shares have been in an impressive bull run for almost 3 years now, fuelled by positive trading updates.

I reviewed EQLS here in July 2022, following reader requests, and came away impressed.

Here’s today’s update -

Equals Group plc (AIM:EQLS), the fast-growing payments group focused on the SME marketplace, is pleased to provide a trading update for the 11 months ended 30 November 2022 (the 'Period').

Various impressive-looking figures are presented, but cutting to the chase -

…the Board expects the Group´s full year results to be ahead of current market expectations.

Ian Strafford-Taylor, Chief Executive Officer, said: "We are extremely pleased to see a 61% increase in our revenues in the 11 months ended 30 November with all segments performing strongly.

Our revenue growth has continued in the face of difficult macro environments and this augurs well for 2023 and beyond.

We continue to invest in people, products and technology to drive our growth strategy and look forward to updating the market in early January with our full year trading statement."

As I mentioned here in July, EQLS seems to be in a sweet spot, and that clearly remains the case.

Broker update - many thanks to Zeus, for providing some numbers in an update note today. Although it hasn’t actually updated its model, but Zeus comments that FY 12/2022 revenues are now likely to beat forecast by about 10%. That could have nice operational gearing to the bottom line, because the gross margin is close to 50%. Hence the extra £5-6m revenues above forecast, would produce c.£3m of extra gross profit. Assuming that all costs remain unchanged, then feasibly this could double forecast profit before tax from £3m to £6m.

Ignore EBITDA here, because it’s inflated by the considerable development spending which is capitalised. Hence any valuation metric based on EBITDA will give an excessive valuation.

A complicating factor is that the broker notes seem to adjust profit before tax to a much larger figure than the £3m statutory PBT (forecast), to c.£10m adj PBT, a huge difference. The forecast EPS of 4.6p is calculated using the larger c.£10m adj PBT figure (less tax). So the main area for further research on this share, is to clarify what the larger adjustments to profit are, and are they reasonable or not?

It seems to be related to the large amount of payroll costs (about 20%) which are being capitalised onto the balance sheet. So I’m raising a flag here that these adjustments to profit need to be properly researched, to justify the current valuation.

My opinion - this looks a bit more complicated that I initially thought. So I’d like to see the full year numbers before forming a definite view on it. The key question concerns the large adjustments to profits, and if they’re reasonable or not? That drives EPS, so determines whether the share price is reasonable or not.

Overall though, I really like the growth that EQLS is producing, and another positive trading update today is really encouraging. It could beat profit forecasts considerably, given the operational gearing. Well worth a closer look, in my view.

There are results presentations recordings on the InvestorMeetCompany website, I might have a watch of the most recent later.

RBG Holdings (LON:RBGP)

66p (down 21% at 10:33)

Market cap £63m

Bad luck to holders here, with a profit warning coming on top of a declining share price trend for the last 18 months or so. As you can see below, it’s now given up almost all the bull run, and is back down near all-time lows again. Could this be a buying opportunity, or are things going badly wrong?

.

RBG Holdings plc (AIM: RBGP), the professional services group, today publishes an update on current trading and outlook.

Looking at its various divisions -

Rosenblatt and Memery Crystal (legal firms) - trading well, and exceeding expectations.

Convex - some revenue deferred into Q1 2023.

Together, these businesses combined have traded “marginally ahead” of expectations. So that looks fine.

LionFish Litigation Finance - this is where the problems have occurred. It’s lost 2 cases, resulting in a £4m write-off. Hence the expected divisional profit of £2.3m for FY 12/2022 will now presumably be a loss of £1.7m .

It sounds like they might wind down this division, reading between the lines. That might be a good idea, as it’s been a flop so far. But I suppose the nature of litigation funding is that some cases will inevitably be lost due to unforeseen reasons. Maybe RBGP bit off more than it could chew, setting up this division and taking on cases that are perhaps too big?

Dividends - sound safe, with confirmation that a second interim divi will be paid.

Balance sheet - reassuring noises are made about financial strength & liquidity. Although looking at its last interim results, I can’t say I’m impressed with the balance sheet, it looks a bit thin, once intangible assets are written off. After the write-off required today, it seems as if NTAV would only be modest. So I’m not sure prioritising dividend payments is the right thing to do.

The £20m loan seems to be from a “large alternative investment firm”, so a key point is that investors need to research the terms (and any covenants) of this facility, which seems to be specifically linked to LionFish, the problem part of the business. That would be a good question to ask management on any webinars or calls - is there any risk to the £20m loan for LionFish funding from the failure of the 2 cases announced today?

Outlook - I wish companies wouldn’t quote EBITDA. It’s so annoying, because the various changes to accounting standards (esp. IFRS 16) mean that we cannot rely on EBITDA as necessarily being a sensible profit benchmark -

RBGLS continues to trade robustly and Convex has a strong pipeline of deals which remain in process. As a result of the case losses in LionFish, the Group now expects adjusted EBITDA to be materially behind current market consensus expectations for 2022 and in a range of between £11.0m-£12.0m. The Board is confident in the medium and long-term outlook of the business.

Broker update - many thanks to Singers, for its revised forecasts, which are now showing £10.1m adj EBITDA, £6.9m adj PBT (note the significant difference, hence why I dislike EBITDA so much!), which is 5.8p adj EPS. This is taking into account the losses at LionFish, so hopefully it might be a low water mark, providing there are no further losses at LionFish. This gives a FY 12/2022 PER of 11.5 - it's difficult to justify anything higher than that right now, and professional services businesses don't tend to attract high PERs, due to the inherent conflict of interests between staff and outside shareholders.

My opinion - the core business seems to be performing well, which is the main thing.

LionFish seems to have gone wrong with 2 cases, so I think we need an update on how the remaining cases are looking (it invested in 12 cases in total). This business was launched in May 2020, and I would imagine it might now be wound down, which would take time, several years probably, and require continuing funding for ongoing cases.

The CEO comes across very well on webinars, but obviously will now need to eat some humble pie, and properly explain to investors what has gone wrong, and what she's doing to sort it out, and reassure investors that the problems won’t worsen.

There have also been questions about excessive rewards for Directors at this company, which is often a problem with professional services businesses.

Wasn’t there an issue about the cost of licensing the Rosenblatt brand name? Something has stirred in the back of my mind about that.

All in all, I’ll keep an open mind on this one. It could be a good recovery candidate, but for now the bull case is looking somewhat tarnished, and the reduced share price does look justified I'm afraid.

Graham’s Section:

A G Barr (LON:BAG)

Share price: 500p (-1%)

Market cap: £560m

This is the Scottish drinks group that includes IRN-BRU, Strathmore water, a UK/EU licence from Dr. Pepper to sell Snapple, and a range of other brands.

Today it announces the £20m acquisition of Boost Drinks, to be bought from the founder of Boost and his wife. An additional £12m might be paid, depending on Boost’s revenue and profits over the next two years.

Boost was founded 20 years ago and the existing management team don’t look like they are ready for pipe and slippers just yet. So it’s good to read that they “will continue to lead the business, operating within [A.G. Barr] as a standalone business unit”.

A description of what’s being bought:

The Boost brand, founded in 2001, primarily operates in the high growth functional beverage category spanning energy, sport and protein, with a strong market position in the UK independent retail channel

I don’t believe I have ever drunk their flagship product, which is an energy drink priced at just 65p. I’ll have to keep an eye out for it next time I’m thinking about getting some Lucozade!

They also sell isotonic sports drinks, protein shakes and iced coffee.

And they have “an asset light business model outsourcing production, warehousing and logistics”.

As for the historic financial performance:

For the year ended 31 December 2021 Boost's unaudited statutory revenue and profit before tax were £42.1 million and £1.9 million respectively with gross assets of £12.5 million

My view

I’ve not seen anything to dislike about this deal.

The price tag when measured against earnings is perhaps slightly above average for a company of this small size. A.G. Barr is paying at least 10.5x last year’s PBT, rising to nearly 17x trailing PBT if the full contingent amount is paid in two years. But given that this is the branded drinks sector, perhaps this is reasonable.

Also, if we look at the deal in terms of revenues being bought in, it doesn’t look expensive to me. A.G. Barr is paying less than 0.8x trailing sales, even if the full contingent amount gets paid.

A.G. Barr itself trades at nearly 2x sales.

And within A.G. Barr, I would expect Boost’s profitability to improve. In the words of today’s RNS, Boost will be able to “leverage the Group's established scale and capability”, using all of A.G. Barr’s various resources including their operational infrastructure.

So this deal gets the thumbs up from me.

A.G. Barr reported cash balances of £61m at its most recent interim results, so there is no question about it being able to afford today’s deal.

I had a fresh look at Barr’s in August, with their share price at 543p, and came away with a positive view on the company and its valuation. I retain that view today. Stockopedia gives it a QualityRank of 98.

Lindsell Train Investment Trust (LON:LTI)

Share price: £1062.85 (+1%)

Market cap: £213m

We rarely cover investment trusts in this report but on a day when the RNS feed is quiet, I hope you’ll excuse me for covering this one.

Nick Train, fund manager at Lindsell Train Limited, is someone whose approach I believe in: buying high-conviction stakes in excellent businesses and holding them permanently.

For example, if you check out the shareholders at Burberry (LON:BRBY) (in which I have a long position), you’ll find that Lindsell Train Limited is the second-biggest shareholder there with the best part of 6% of the company. It’s not so often you find a medium-sized investment manager with such a meaningful stake in a FTSE-100 stock!

LTL also owns 4.4% of London Stock Exchange (LON:LSEG) and 1.5% of Diageo (LON:DGE) .

The Lindsell Train Investment Trust has been designed in such a way that investors can use it both to own a stake in Lindsell Train Limited (the fund management company) and to own stakes in LTL’s favourite businesses. A very nice combination, if you believe in their approach to doing business. The trust also provides seed money for new fund launches at LTL.

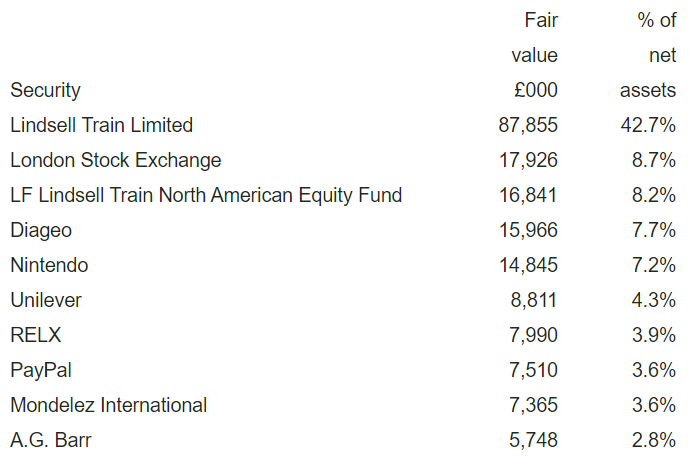

Here are the trust’s top ten holdings. You’ll see that A G Barr (LON:BAG) makes the cut:

The goal of the trust is “to maximise long-term total returns with a minimum objective to maintain the real purchasing power of Sterling capital.” This doesn’t imply any particular benchmark except perhaps inflation as a lower bound.

It expects to have ”a concentrated portfolio of securities with the number of equity investments averaging fifteen companies”. I like investment managers with the courage of their convictions!

Performance: the six months to September were tough for the trust. It had a negative total return (-3%) but thanks to its dividend payment to shareholders, it did outperform the MSCI World Index (an index of stock market returns in the developed countries).

Lindsell Train Limited: assets under management at LTL fell by 10% to £18.6 billion in H1, mostly due to redemptions.

Some commentary explains that LTL’s investment approach is under pressure at the moment:

LTL has suffered from more than two years of disappointing relative performance across all its four equity strategies which, together with widespread outflows from equity funds generally, underlies this loss of FUM. The experience of recent years illustrates the investment risk inherent in a fund management business that has a singular approach to investing... LTL and the Company’s Directors strongly believe that this approach will outperform in the long term, given the Investment Manager’s concentration on companies that should generate consistently higher returns on capital over time. However, the strategy can fall out of favour when it is seen to be generating inferior short-term returns compared with alternative strategies.

Although it increases the risk over short periods of time, I still much prefer fund managers, such as LTL, who have what they describe as a “singular approach”. Instead of trying to be all things to all people, they have a particular strategy and a particular style and they stick to it.

They also note that listed fund managers are on average now being valued at 1.4% of AUM, versus 3.2% a year ago. In round numbers, this means that you now get £70 of AUM for every £1 you invest in a fund manager, versus £30 a year ago. The entire space has been devalued and derated at the same time that AUM has fallen.

This is the basis for my contrarian investment thesis: whenever AUM starts rising again, I also expect that fund manager valuation multiples will revert back towards normal, and for their share prices to make some excellent recoveries.

My view

The trust’s Net Asset Value, as of November 25th, was £1018.46. As with many trusts, the LTI share price seems to be a lot more volatile than the NAV, trading at a discount or a premium depending on the market’s mood:

Since I like their investment style, I wouldn’t mind paying a small premium for this trust but a discount would of course be nice too!

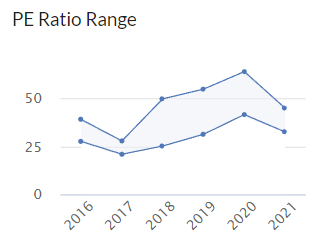

Their top holdings probably did get overvalued to an extent, so a period of underperformance may have become inevitable. London Stock Exchange (LON:LSEG) , for example, was trading at silly PE multiples:

The “quality” investing style favoured by LTL has become a crowded space and it’s about time that “value” outperformed for a while. But over a period of many years, I would still expect LTL, the trust and its investee companies to do well. Thumbs up from me.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.