Good morning from Paul & Graham! It's a very quiet news day today. Today's report is now finished.

Weekend podcast - was published here (and on podcast platforms) around Saturday lunchtime. I've typed up the written summary, for Stockopedia subscribers only, which is here. Lots of ground covered, as usual!

Mello Monday - is this evening, starting at 17:00. Fund manager Judith MacKenzie is being interviewed, and one of my favourite companies Sanderson Design (LON:SDG) is also presenting.

Agenda

Paul's Section:

Joules (LON:JOUL) - financially distressed special situation. Its update today includes yet another profit warning, and indications that it's going to run out of headroom at end Nov 2022, hence is seeking bridging finance. More detail below, this share looks increasingly precarious, so I'm steering clear.

Loungers (LON:LGRS) [no section below] Quite an interesting development here. This lounge/bars operator thanks it has spotted a gap in the market, and is creating a third format, called “Brightside” - roadside cafes, which evokes Little Chef, focused on comfort food, including all-day breakfasts. Sounds great to me! LGRS management is respected as being best in class operators, so I imagine they’ll probably do well with this new format too. Three sites in the South West have been lined up for spring 2023 opening.

Graham's Section:

Appreciate (LON:APP) (£48m pre-open) - two of my favourite financial stocks are set to combine forces. PayPoint (LON:PAY) has offered 44p for each Appreciate share, in the form of 33p plus a fraction of a PayPoint share. Even though it’s a premium of nearly 70% to the existing Appreciate share price, I suspect that Paypoint will do extremely well out of this. The Appreciate valuation was extraordinarily low, and they are about to start benefiting from higher interest rates. My attention now turns to Paypoint. It’s not quite as cheap as Appreciate was, but I expect it to benefit from this acquisition. As was the case with Appreciate, I suspect that stock market investors also underrate it and undervalue it.

DWF (LON:DWF) (£221m) (-2%) [no section below] - this large professional services company announces an acquisition worth up to £27.7m (including debt). It’s buying a Canadian law firm that earned revenues of £20m (translated from CAD) last year, and adjusted EBITDA of £3m. The deal “marks the next step in DWF's North American strategy and will result in an integrated legal and business services offering in Canada”, while also tying in with DWF’s Chicago operations. The two firms appear to share some of the same clients, and referrals can flow from one to the other.

DWF’s net debt (excluding lease liabilities) was £72m as of April 2022. However, a big chunk of today’s deal will be paid for in the form of newly-issued DWF shares, so the impact on overall leverage should be limited. DWF also reassure shareholders that they expect “deleveraging beyond the current financial year to be driven by profitable growth and strong cash generation”. DWF’s value metrics are extremely cheap at present, but listed law firms can be a bit of a minefield. These shares might be best left to sector specialists. [no section below]

Explanatory notes -

A quick reminder that we don’t recommend any stocks. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps up to about £700m. We avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech).

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to.

Paul’s Section:

Joules (LON:JOUL)

13.7p (pre market open)

Market cap £15m

Joules, the premium British lifestyle group, provides an update in regard to its turnaround plan, and current trading and financial position.

The current year is FY 5/2022.

As we already know, this is now a financially distressed special situation, so high risk.

Today’s update says -

Trading behind expectations (11 weeks to 30 Oct 2022)

Blames macro factors & mild weather (which didn’t seem to hurt larger competitor Next (LON:NXT) which recently reported solid trading)

Advanced discussions with a number of strategic investors (including Tom Joule) re equity raise.

Possible CVA also being planned (a solvent form of restructuring, to get rid of lease liabilities and potentially other liabilities)

Ominous sounding “other options” also being considered, which I suspect might be a pre-pack administration, should they be required - which would wipe out existing equity.

Discussions with bank lender over easing of covenants.

Net debt was £25.7m at end Oct. £11.4m headroom, but £5.6m of this is “trapped cash” with payment providers (which I assume means merchant card processing?)

Bank facility (RCF) set to reduce by £5m at end Nov, which can’t be paid without some bridging finance.

My opinion - this sounds grim. It sounds to me as if the risks have worsened, and there’s an increased chance of existing equity holders being wiped out through heavy dilution, or insolvency. I’d steer clear for now, until it’s either done a refinancing or gone bust.

Graham’s Section:

Appreciate (LON:APP)

Share price: 26.05p (pre-market)

Market cap: £48m

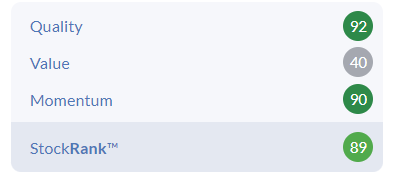

I noted in September that Appreciate, the Liverpool-based gift voucher company, was a potential value investment with a StockRank of 93, and a ValueRank of 87 at the time.

This is a share I owned quite a few years ago (first purchasing it in 2017), but did not hold onto it. It was hit badly by Covid and has been looking to replace senior leadership roles - it does not currently have either a permanent CEO or a permanent CFO.

Investors have had little interest in owning a business that sells High Street vouchers, which has resulted in the following metrics showing up:

However, trading has been good: the September update was encouraging with the Group reporting that it was set up “strongly” for the Christmas period, and the outlook remained in line with prior expectations.

The value on offer has been spotted by another financial stock that I’m a fan of, namely Paypoint (PAY).

Therefore, this is the offer for each Appreciate share:

- 33 pence in cash and

- 0.019 New PayPoint Shares

If the deal goes through, Appreciate’s shareholders will wind up owning 5% of PayPoint.

A PayPoint share was worth 580p last night, and therefore the offer is worth 44p for each Appreciate share.

As pointed out in the RNS, this is a major premium to the existing Appreciate share price, whether measured by last night’s price (68.9% premium) or by the average price over the last three months (63.8% premium).

The deal has to be put to a vote, of course, but already it has been indicated that 23% of shares will vote in favour of the deal.

The Appreciate shareholder base consists mostly of professionally-managed funds who I’m guessing will be glad to see the back of a company with a sub-£50 million market cap:

Comment from Exec Chairman of Appreciate:

"PayPoint's offer represents an attractive premium for Appreciate Group Shareholders providing an opportunity to exit the majority of their shareholdings for cash, whilst participating in the potential upside of the combined Appreciate Group and PayPoint businesses over the long-term.

Comment from Chief Executive of PayPoint:

…the proposed acquisition would jointly target growth in three broad areas: prepayment saving through Park Christmas Savings to support customers with budgeting tools for Christmas and other events; an enlarged full-service offering for gifting, employee rewards and benefits to Appreciate Group's corporate clients; and an extended consumer gifting network for the Love2shop brand.

My view

Even at a premium of nearly 70% to the prevailing Appreciate share price, I suspect that PayPoint is getting a bargain here.

The offer is valued at £83m. As announced in today’s RNS, they are paying 6.2x adjusted EBITDA for the year ended March 2022.

For the current year - FY March 2023 - forecasts suggest that Appreciate’s adjusted pre-tax profit is going to be over £9m. So they are paying barely over nine times that.

They are also buying a bullet-proof balance sheet: Appreciate’s year-end cash was last seen at £20m. Including cash held in trust, average funds held during the year were £179m.

As I was saying back in 2018, when Appreciate was still called “Park Group”, there is an implicit interest rate hedge at this company, since it benefits from higher rates.

PayPoint will know this, and have timed their purchase very nicely as interest rates rise.

There is also the possibility of some valuable synergies, although I’m not sure exactly how it will work. I suppose that consumers who use PayPoint’s terminals might benefit from the traditional Christmas saving scheme offered by Appreciate.

And perhaps it makes sense for Appreciate’s gift voucher business to plug into PayPoint’s existing retail network of convenience stores. It will be interesting to see how the two businesses might cooperate.

However it might work, I believe that the deal will get voted through, because Appreciate’s fund manager shareholders will want to see the back of a holding that has been an awkward one to sit on for the past five years.

Looking forward, I think this deal adds to the attractiveness of PayPoint shares, which already have a very high StockRank and (from my point of view) a cheap valuation:

I was a fan of Appreciate, and a fan of PayPoint, so I’m certainly going to be a fan of the combined business! My most recent PayPoint commentary can be found here.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.