Photo by Alvan Nee on Unsplash

Welcome back to our Stock Pitch series. This week I’m doubling down on my value instincts and looking at a highly-ranked but unloved FTSE 250 stock – a business I see as the pet equivalent of Tesco.

Read on to find out why Pets at Home (LON:PETS) has caught my interest recently as a potential contrarian buy.

Disclosure: at the time of publication, Roland has no position in PETS.

Share price at the time of publication: 193p

Market cap: £860m

The Pitch

Pets at Home was founded in Chester in 1991 and floated on the London market in 2014.

It’s the UK’s largest pet care retailer and one of the largest veterinary groups, with estimated market shares of approximately 25% and 10%, respectively.

The pandemic pet boom fuelled record profits in 2022, but the company has struggled a little since then as demand has normalised post-Covid. Fewer people having new pets means less spending on new accessories and fewer vet checks for young animals.

Pets has also suffered from cost pressure and admits that some of its ranges – notably in nutrition and accessories – have “lacked innovation” and failed to meet customer needs.

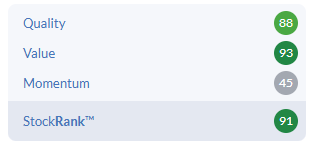

After a valuation overshoot in 2021, the company’s shares have now truly shed their pandemic froth. Pets’ share price has fallen by more than 60% from the all-time high of 505p seen in September 2021 – but its StockRank has been rising recently:

Pets at Home remains a market-leading and profitable business, with a credible turnaround plan and experienced new management. Profits are expected to return to growth this year, too.

On a forward P/E of 12, I think the shares are starting to look undervalued. In my view, this could be an attractive turnaround situation.

The StockRanks agree, with Contrarian styling and high quality and value scores:

The Big Picture

In my view, there are several factors that make this situation attractive right now:

Sticky business model: the company’s platform business model includes retail, online, product subscriptions, vet care and – shortly – pet insurance. Pets’ loyalty club…