This column usually analyses stocks on a company by company basis, but we will take a different approach this week and compare companies within particular sectors. In the consumer cyclicals sector, we contrast Moss Bros with Mothercare. In the financial sector, IG Group goes head to head with Charles Stanley.

Consumer Cyclicals: Moss Bros vs. Mothercare

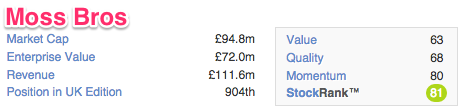

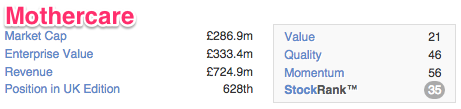

Moss Bros has a StockRank of 81, up 20 from last week, while Mothercare has a StockRank of 35. Last week it was 41. What is Moss Bros doing right? What is Mothercare doing wrong?

Sales growth (Quality)

Both companies have enjoyed different fortunes when it comes to sales growth. Moss Bros has managed to grow revenues each year since 2011. This is thanks partly to online sales. Internet sales doubled over the last half year. They now account for around 7% of total revenues. The company also continues to develop new products, having recently launched a series of sub-brands, including Moss London, Moss 1851 and Moss Esquire. Brokers predict that these products will help the company grow revenues by around 5% in 2014.

The picture is more gloomy for Mothercare, where sales have consistently fallen since 2012 and are expected to fall again in the twelve months to March 2015. Weaker footfall and price cutting have both worked to hit sales and margins.

Productivity (Quality)

Both companies are becoming more productive. Moss Bros has a Piotroski score of 7 out of 9 and is more productive than it was last year. Asset turnover can be used to measure productivity. It shows how effective a company is at using assets to generate revenues. Moss Bros asset turnover is now 1.9, compared to 1.8 last year. The company closed 9 stores for refurbishment last year and another 14 units will be refurbished in the second half of their year. The company’s management team claim that their refurbished stores deliver a sales increase of between 8 to 10 per cent in the first year. Mothercare has a lower Piotroski score of 5 out of 9, but generated a…