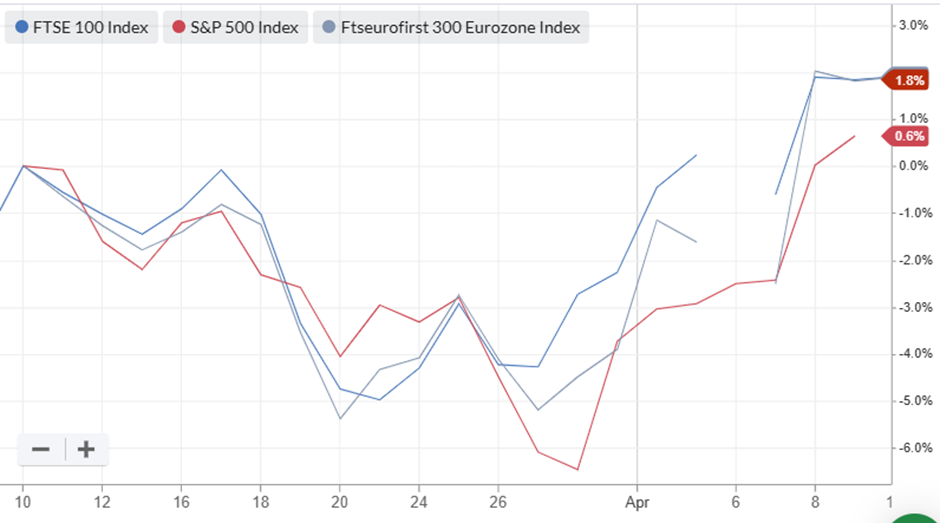

Most indices largely tracking each other this week, and marked by the big rise mid-week in response to the ceasefire announcement:

The truce holds, for now. But with both sides calling each other out for alleged violations of the deal they thought they'd agreed to, it would be unusual not to see more volatility ahead.

Here's what we can look forward to next week:

Economic Calendar

Monday 13 Apr |

||

15:00 |

United States |

Existing Home Sales |

19:00 |

United States |

Budget Statement |

Tuesday 14 Apr |

||

04:00 |

China |

Balance of Trade |

07:00 |

UK |

Retail Sales |

07:00 |

Germany |

Wholesale Price Index |

13:30 |

United States |

Producer Price Index |

Wednesday 15 Apr |

||

10:00 |

Euro Area |

Industrial Production |

15:30 |

United States |

Crude Oil Inventories |

Thursday 16 Apr |

||

04:00 |

China |

GDP |

07:00 |

UK |

GDP |

13:30 |

United States |

Initial Jobless Claims |

14:15 |

United States |

Industrial Production |

Friday 17 Apr |

||

10:00 |

Euro Area |

Balance of Trade |

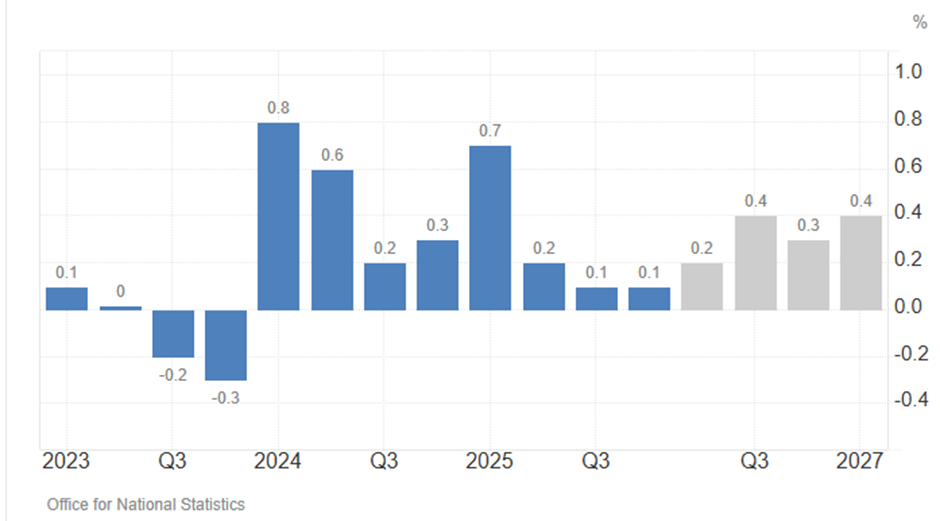

UK GDP

UK GDP growth has been weak at the end of 2025 and into 2026. However, it is forecast to pick up through the year:

[All charts in this section: Trading Economics]

However, global events have the power to upend these forecasts. This week's print may show early signs of the impact these are having.

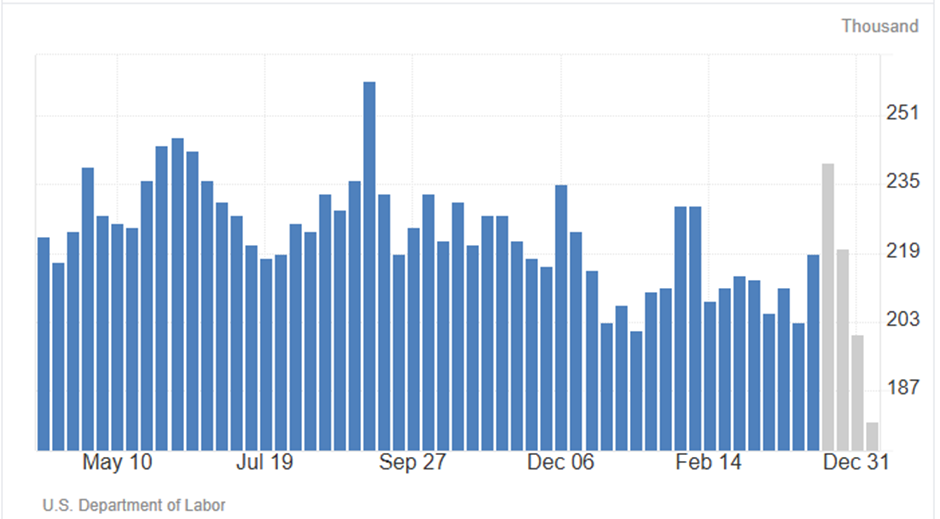

US Employment

With higher fuel prices in the US affecting consumer sentiment, this will start to feed through to employment. Initial claims are expected to rise in the short term:

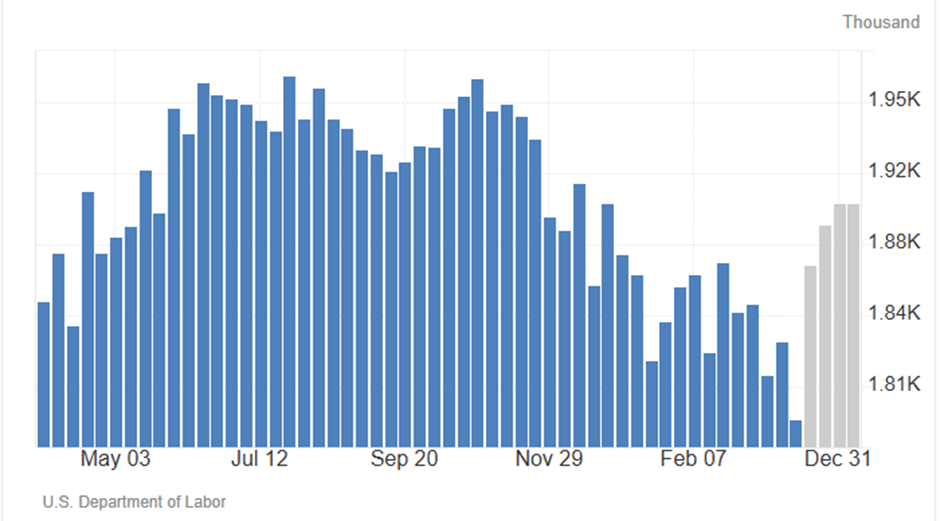

With a knock on impact on continuing claims:

Forecasts are for claims to remain below the levels seen for most of 2025, so any unexpected spike in response to recent global events may be poorly received by markets (and the Trump administration!)

Companies Reporting

| Date | UK Trading Updates & AGMS | UK Financial Results | International… |

|---|