Welcome back to The Week Ahead. Headlines are currently dominated by the prospects of a more lasting peace agreement between the US and Iran. Talks are said to be underway ahead of the expiry of the current two-week ceasefire on 22 April.

Thursday night also saw Israel agree a 10-day ceasefire in Lebanon, which it’s hoped may be extended to tie into a wider US-Iran deal.

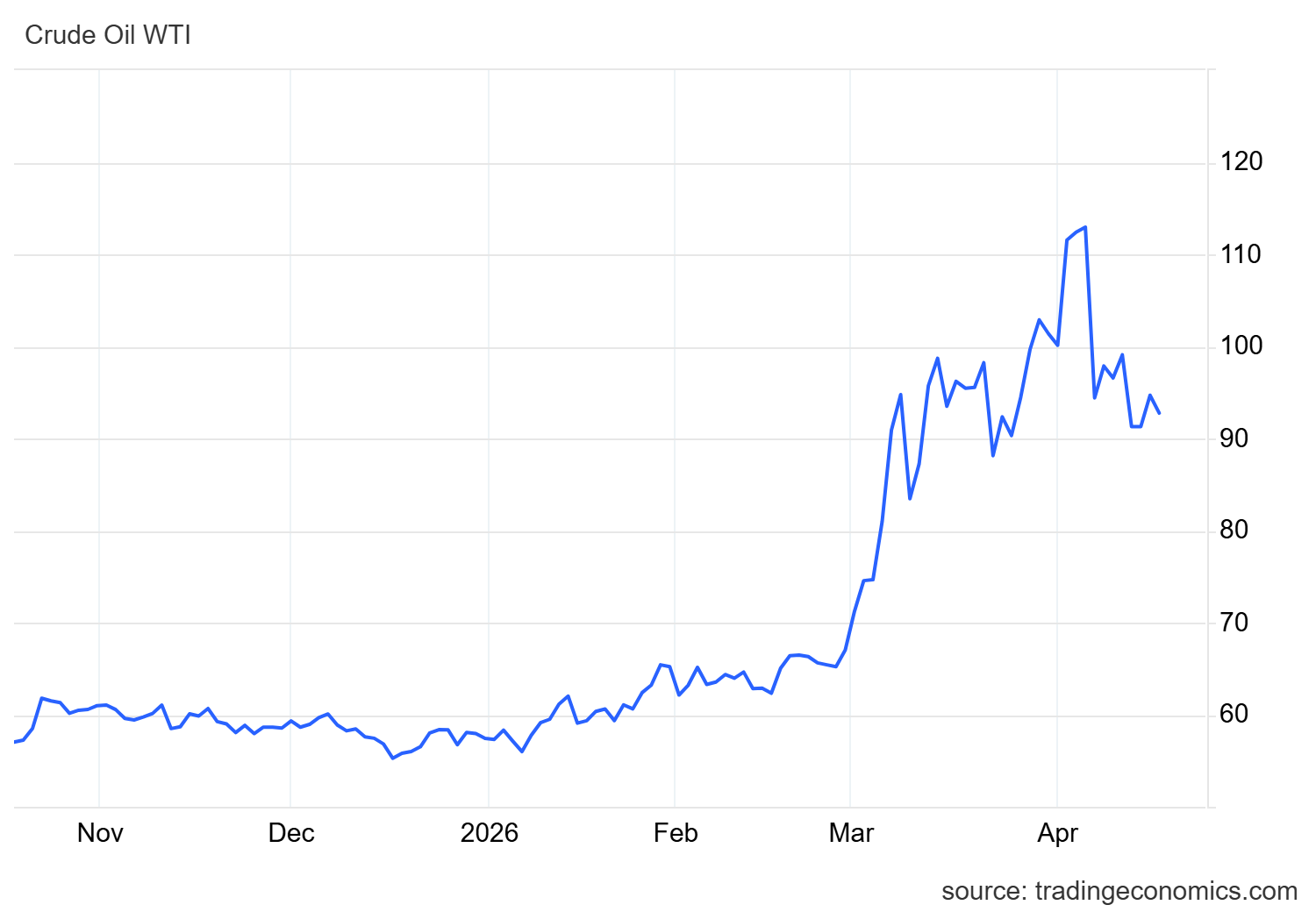

At this time there seems no way to be sure how likely a sustainable peace deal might be. Markets are taking what I’d describe as a relatively optimistic view. Oil prices have dropped back below $100 over the last week…

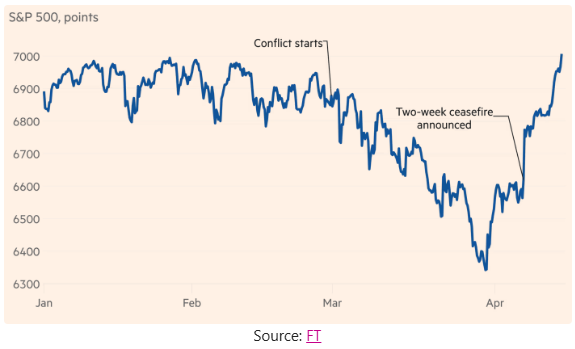

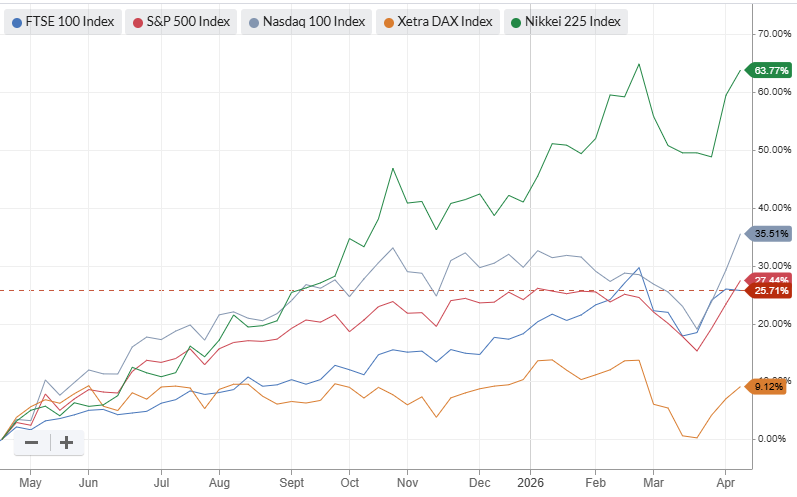

… while market indices have edged higher, with the S&P 500 making new record highs:

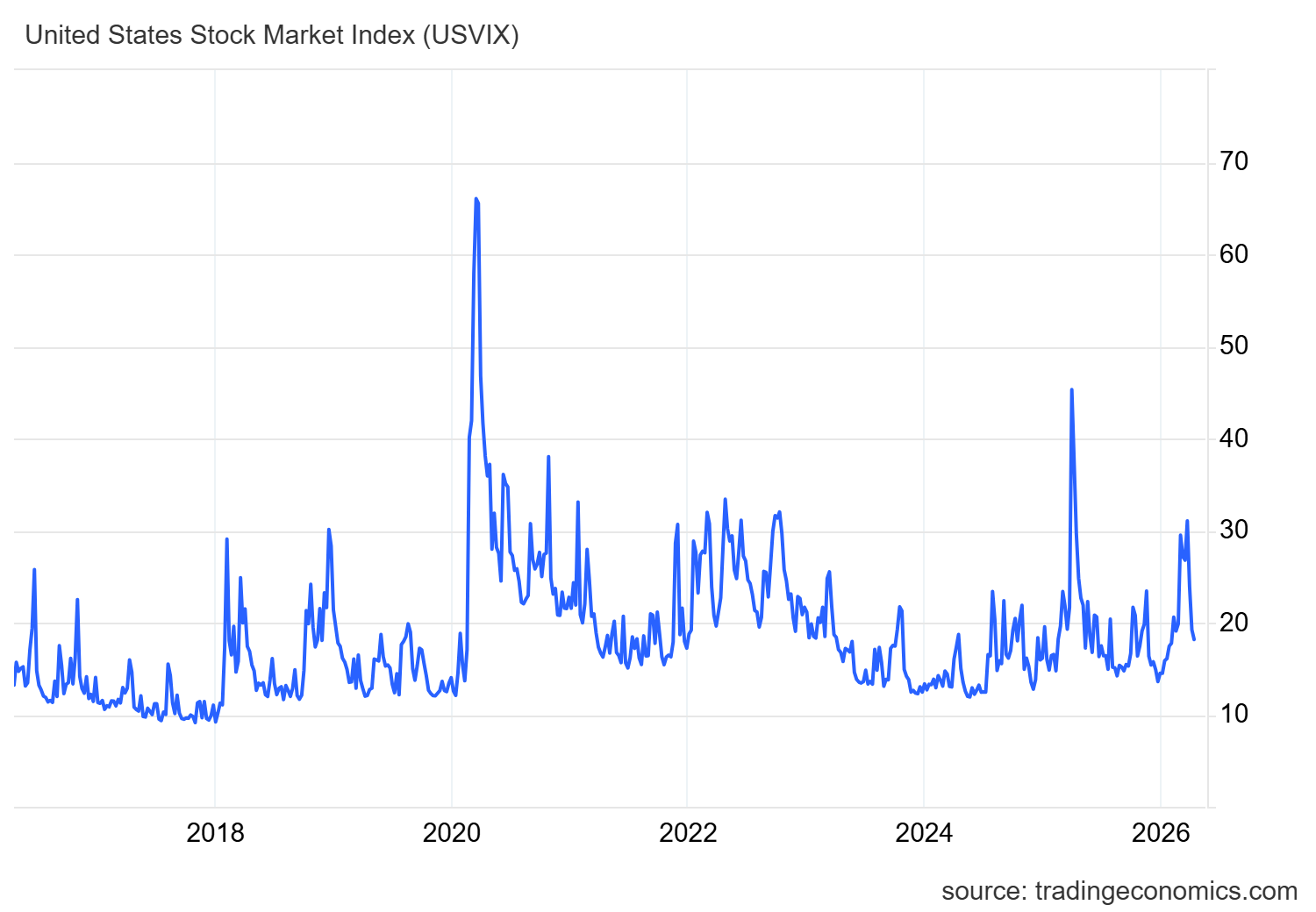

The US VIX volatility index has also continued to decline and now looks remarkably subdued to my eyes. Current levels are hardly any higher than the 10-year average:

Crunch time approaching?

While I am obviously hoping for a deal, I do think there’s a case to be made to suggest that markets are not yet pricing in the risks that could stem from further disruption to global energy supplies.

It’s worth noting that even if Hormuz was reopened fully tomorrow (it won’t be), refilling the global floating pipeline of tankers and resuming normal levels of deliveries would take weeks or even months. In addition, some refinery and terminal capacity in the Gulf has been damaged by bombing and will take much longer to restore.

Current restrictions on oil exports from the Gulf are currently thought to have cut global oil supply by 10%-15%. Unlike during the pandemic period, there has not yet been any corresponding reduction in demand.

While strategic stockpiles and existing inventories have cushioned the impact so far, the final tankers that loaded and sailed before the start of the war are expected to have unloaded by the end of April.

This situation could potentially see fuel shortages to start biting in Asia and Europe in May. That could see non-essential travel and industrial activity curtailed, leading to an economic slowdown.

High domestic production would probably mean that the US escaped any physical shortages until mid-summer, according to analysts. However, US consumers and…