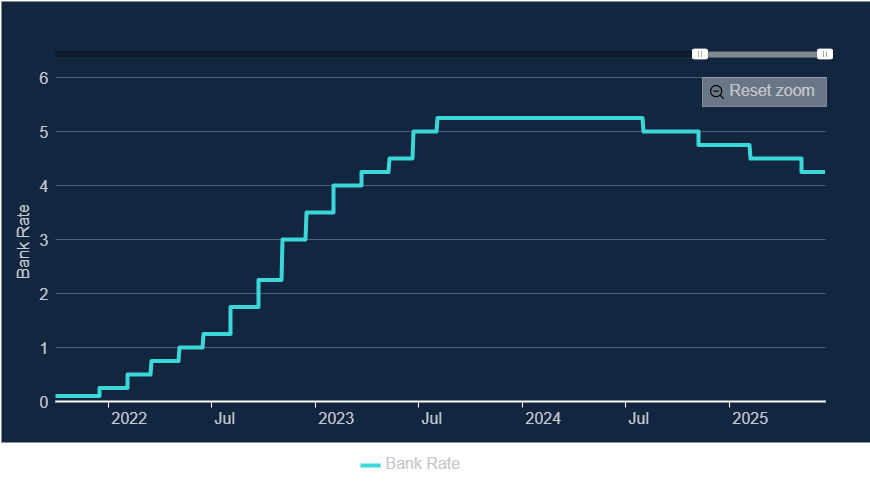

The Bank of England left interest rates unchanged at 4.25% this week, with six members of the Monetary Policy Committee (MPC) voting to hold and three preferring a 0.25% cut.

However, the MPC noted that “underlying UK GDP growth appears to have remained weak” and said it expects to see “a significant slowing” in pay growth over the remainder of the year. The consensus view in the market after this week’s decision seems to be that another rate cut may be likely in August.

Source: Bank of England

Looking ahead, next week’s NATO Summit in The Hague is expected to be relatively brief, with the agenda focused on discussing a new target for members' defence spending.

The proposal on the table is for members to increase their spending to 5% of GDP over the next 10 years. That could be bullish for UK and European defence stocks and perhaps some infrastructure construction groups.

However, an increase in NATO defence spending has been expected for a while, given pressure from President Trump and wider events in Europe and the Middle East. I think we might argue that a certain amount of growth is already priced into companies such as BAE Systems (LON:BA.) , which is currently trading on 25x forecast earnings.

Elsewhere, next week is expected to bring a fresh batch of economic data to help investors gauge the health of the US, UK and European economies. Results from US heavyweights Nike and FedEx may also provide insights into consumer spending, tariff impacts and broader conditions in the US economy.

In company news, it’s looking like another relatively quiet week for UK big cap news, but there are a few interesting small and mid-caps scheduled to report. We’ll be covering all the top stories in the Daily Stock Market Report, as always.

Economic Calendar

Date | Time (BST) | Country | Event |

23 June | 08:30 | Germany | Manufacturing PMI |

23 June | 09:30 | UK | Manufacturing & Services PMIs |

23 June | 15:00 | US | Existing Home Sales |

24 June | 09:00 | Germany | Ifo Business Climate |

24 June | 11:00 | UK | CBI Industrial Trends Orders |

24 June | 14:00 | US | Case-Shiller Home Price Index |

24 June | 21:30 | US | API Crude Oil Inventories |

25 June | 05:00 | EU | New Car Registrations |

25 June | 15:00 | US | Federal Reserve Chair speaks |

25… |