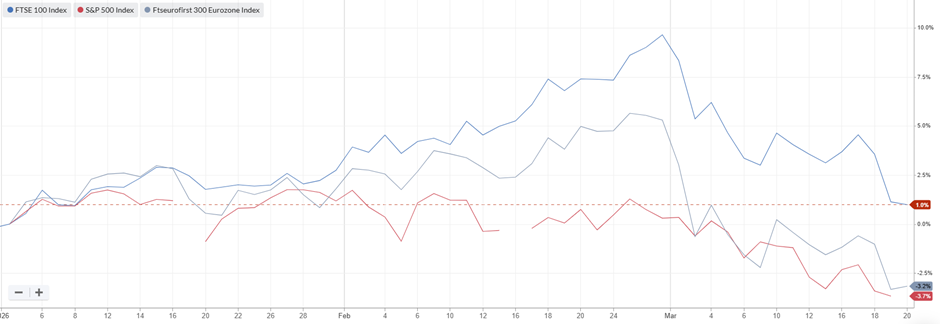

It's been a pretty crazy week for global markets, as equities sold off in response to global events and worries that higher energy prices will feed through to higher inflation and rates. The S&P 500 and Eurozone index are firmly in the red YTD, and the FTSE 100 only just clings on to a small gain due to its oil and mining constituents:

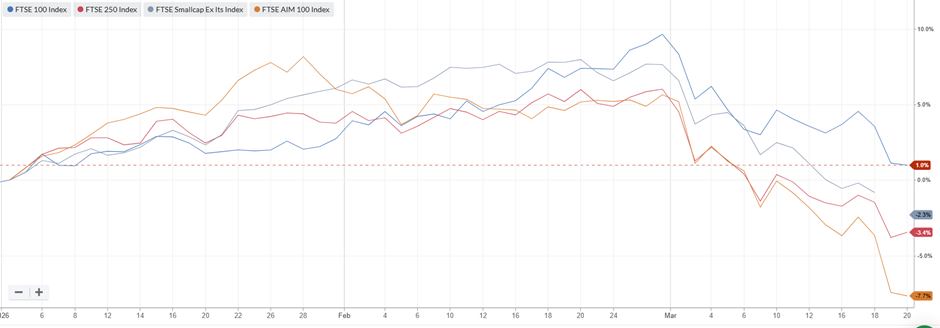

Things get worse as we go down the market cap level in the UK, with the FTSE 250 going negative YTD. AIM in particular has taken a battering (although the AIM 100 is a slightly strange index dominated by a smaller number of large companies that have chosen to remain on AIM):

Perhaps the biggest surprise, given global uncertainty, is the drop in the gold price over the past week:

It seems that Gold’s status as a safe haven has been overwhelmed by Gulf countries' need for cash after losing short-term oil and gas revenue, plus potentially margin calls on commodity traders caught short oil into the crisis.

In the case of oil itself, the market initially priced this as a short-term issue. Whereas this week, prices have moved upwards across the forward curve. Oil futures are above $70/bbl out to September 2028:

This means producers should be able to hedge strong prices into the future, making hay for several years, not just while the sun shines for them in the short term.

Here's what we can look forward to next week:

Economic Calendar

Monday 23 Mar |

||

15:00 |

Euro Area |

Consumer Confidence |

23:30 |

Japan |

Inflation Rate |

Tuesday 24 Mar |

||

09:30 |

UK |

Manufacturing PMI Services PMI |

12:30 |

United States |

Retail Sales |

20:30 |

United States |

API Crude Stocks |

23:30 |

Japan |

BoJ MPC Meeting Minutes |

Wednesday 25 Mar |

||

07:00 |

UK |

Inflation Rate |

09:00 |

Germany |

Business Climate |

12:30 |

United States |

Current Account |

14:30 |

United States |

EIA Gasoline Stocks EIA Crude Oil Stocks |

Thursday 26 Mar |

… |