Markets

What a week! Everything has been overshadowed by geopolitical events. There is an old market adage that says, “in a crisis, the only thing that goes up is correlation!” and so it seems over this past week. Days seem to have been marked out as either risk on or risk off, with major indices moving in step with commodities such as gold and silver. Only energy has broken the trend, with oil up on the closure of the Straits of Hormuz, and natural gas on the news that Qatar was ceasing LNG shipments.

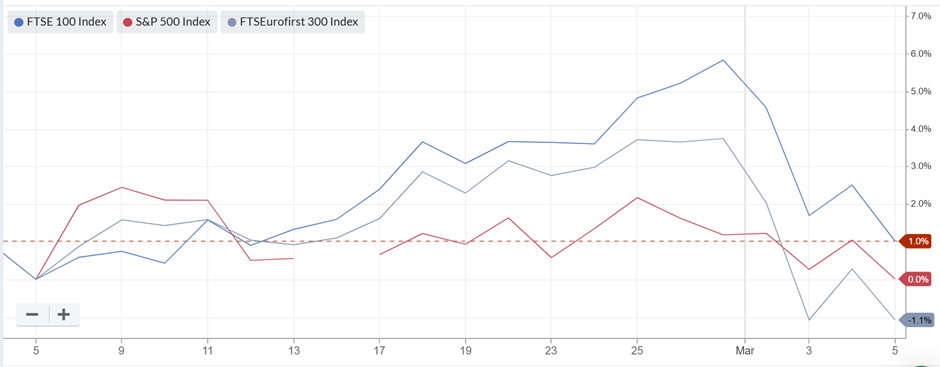

While this may seem another victory for the FTSE100 over the last month, this is a largely phiric one, as a flight to safety saw the US dollar strengthened against the pound, making the moves in dollar terms broadly similar.

Iran cannot win a war against the US and Israel. However, they don’t have to win to cause chaos, and we have already seen an Iranian missile hit Bahrain’s main oil refinery and a number of oil tankers hit in the Persian Gulf. US administration estimates of how long this war will last have already gone up from 2 weeks to 100 days. The US stated goal of regime change is very hard to achieve through airpower alone. This may go on for some time…

Here's what we can look forward to next week:

Economic Calendar

Monday 9 Mar |

||

01:30 |

China |

Inflation Rate |

23:50 |

Japan |

GDP Growth |

Tuesday 10 Mar |

||

03:00 |

China |

Balance of Trade |

14:00 |

United States |

Existing Home Sales |

20:30 |

United States |

API Crude Stocks |

Wednesday 11 Mar |

||

12:30 |

United States |

Inflation Rate |

14:30 |

United States |

EIA Crude Oil Stocks |

Thursday 12 Mar |

||

07:00 |

UK |

RICS House Price Balance |

12:30 |

United States |

Housing Starts Building permits |

Friday 13 Mar |

||

07:00 |

UK |

GDP Balance of Trade Industrial Production |

Interest Rates

It is far too soon to see the impact of recent geopolitical events on economic data. However, this doesn’t mean there hasn’t been any change to outlook. Treasury yields have risen as…