Background and Preamble

Works Co Uk (LON:WRKS) is "one of the UK’s leading multi-channel specialist retailers of value gifts, arts, crafts, toys, books and stationery", but best known for its 500+ high street stores which generate the vast majority of reported revenue. They came to the market in Summer 2018 with management / private equity realising £36.7m and £28.5m being used to repay debt - their prospectus can be found here. Card Factory founder Dean Hoyle retains a significant shareholding and continues as Chairman. Performance has been disappointing - in January the FY 2021 EPS forecasts had fallen from 15p a year before to 6p and the share price had fallen 85% from its highs. All their shops are currently closed but online sales continue with extended delivery times.

With so many serious investors now subscribing to Stockopedia, a company's StockReport™ can be considered a form of "outside view". Therefore, however well I think I know a company, I still regularly check it on Stockopedia both as a sanity check and to see how it is likely to be perceived by other investors. This article explores what is behind The Works' StockReport, with a focus on quantitative rather than qualitative aspects, and considers how its StockReport is likely to evolve in future. It is aimed at readers with a moderate level of experience of Stockopedia.

At the time of writing I have no position in The Works.

Analysis

Balance Sheet

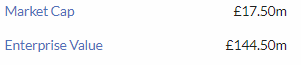

On first glance the balance sheet appears to be very stretched. Valuation implies high likelihood of failure and this is supported by the Bankruptcy Risk:

The vast majority of the £127m total debt figure implied by the Market Cap and EV figures above (and repeated in the Stockopedia balance sheet) relates to IFRS 16 lease liabilities. Including this within the EV makes most bricks and mortar retailers look more highly financially geared than before. It has been argued that it makes no sense to recognise the lease liability without any recognition of right-of-use assets since no circumstances could be conceived whereby the right-of-use becomes worthless (but then, some have criticised share prospectuses for diluting the usefulness of the "Risk Factors" with extremely unlikely ones such as "an outbreak of a pandemic disease"). About 5% of their stores are garden centre concessions where rent may not be due…