Market commentators love to separate stocks into value and growth buckets. Even academics like to use this language. When Eugene Fama and Ken French wrote their seminal paper on their three-factor model, they called the high price-to-book stocks “growth stocks”. However, their methodology didn’t actually measure the growth in earnings of such stocks. They inferr that they are fast-growing from the fact that they are expensive. If investors are paying up to own these types of stocks, surely they must be expecting them to grow rapidly in the future.

It is true that stocks with a high price-to-book do grow more rapidly than market averages in the short term, but the effect is relatively short-lived. The reality is that the average “value” stock will grow earnings in line with market averages over time, as will the average “growth” stock. The only difference is how much an investor pays to own these stocks and the difference in returns they get while waiting for that mean reversion. Growth stocks should be priced more highly than value stocks to reflect better near-term Growth. The problem is that investors often expect them to grow at the same rate for an extended period and overpay for such businesses. It would perhaps have been better for all concerned if Fama and French had referred to these as “cheap” and “expensive” stocks rather than “value” and “growth”.

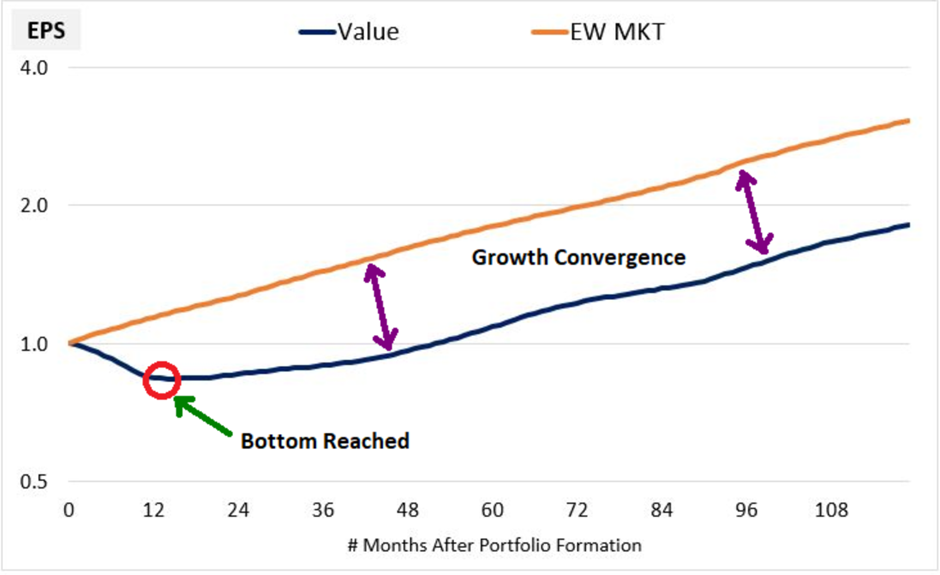

Far from being unimportant to investing in value stocks, growth is a fundamental part of the returns that the strategy generates. As one of my favourite charts from Factors From Scratch demonstrates:

Likewise, valuation is an important part of being a successful growth investor. Understanding these principles has led to the rise of GARP investing - Growth at a Reasonable Price. The cornerstone of this approach is the Price-Earnings-Growth ratio:

Price-Earnings-Growth (PEG) = Price-Earnings Ratio / Growth Rate of Earnings

Which can be found on the Stockopedia StockReport here:

It was initially developed by Mario Farina and featured in his 1969 Book, A Beginner’s Guide To Successful Investing In The Stock Market, but the legendary Peter Lynch popularised it. For this ratio, smaller is better, as it implies earnings are growing more rapidly than the P/E ratio. There are a few different versions of the ratio, and Stockopedia provides the ability to screen for…