Value investors generally have to be a tenacious bunch. While everyone knows that value will out in the long run, in the short run it seems to have a torrid time. Within these long periods of underperformance lies the risk that value investors lose their careers in the process - a grim prospect for many. Warren Buffett himself underperformed the market during the dot com bubble by something like 70%. Luckily for him he had the record and authority not lose his job. Others like Tony Dye at the time had no such luck. The risks that value investors deal with in pursuing their strategy are very real. But what if there were a way to mitigate these risks?

In 2008, Cliff Asness, Goldman Sachs alumni and founder of the big quantitative hedge fund AQR Capital, published a research paper titled "Value and Momentum Everywhere" that holds some hope for those value investors willing to broaden their remit. Most investors who've been around markets know that over the long run both value investing and momentum investing work, but something extraordinary appears to happen when they are baked together.

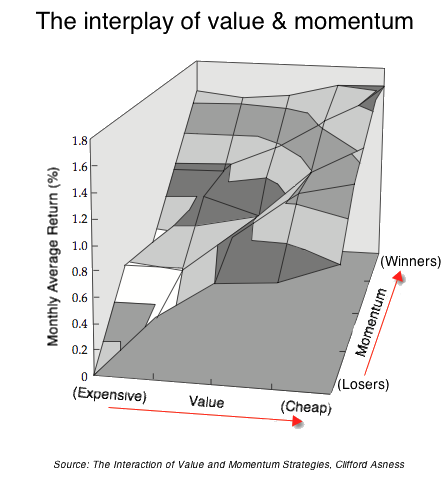

Building the combined value & momentum portfolio

Asness et al decided to study a combined portfolio weighted 50% towards a value strategy, and 50% towards a momentum strategy across a range of asset classes and geographies. Most previous studies had only investigated either value or momentum on their own, usually in an isolated asset class or geography. By investigating 'Value and Momentum Everywhere' the authors were able to highlight a completely global phenomenon - that value and momentum, when brought together create quite remarkably strong returns with remarkably low volatility.

Across the US, UK, Europe and Japan they looked at portfolio returns in not only traditional stock portfolios but also index stock portfolios, currencies, commodities and bonds. Each portfolio was constructed to be market neutral - for the stock picking strategies this meant being long cheap stocks and short expensive stocks (by price to book) and long recent momentum winners and short losers (by 12 month price return). Microcaps, closed end funds, financials and REITs were excluded.

Asness et al found that momentum and value strategies not only provide strong returns, but that they are negatively correlated. What this means in plain english, is that when one strategy works well, the other…