VEEM (ASX:VEE) are a Perth based engineering firm specialising in marine propulsion and stabilisation systems for the global luxury motor yacht, fast ferry, commercial work boat, and defence industries.

Although the company is managed as a single business segment, VEE comprises the following sales categories Propulsion and Stabilisation, Defence, and Engineering. In my view and of VEE, their competitive advantage is their continued in-house R&D, allowing them to release and specialise in new and efficient technologies.

With their world class gyrostabilisers (gyros) and propeller products receiving ever increasing demand both at home and internationally, this is testament to their R&D abilities (more on this below). VEE are not an engineering services firm, but use their engineering prowess to design and manufacture world-class marine parts, products, and systems which they then market and sell.

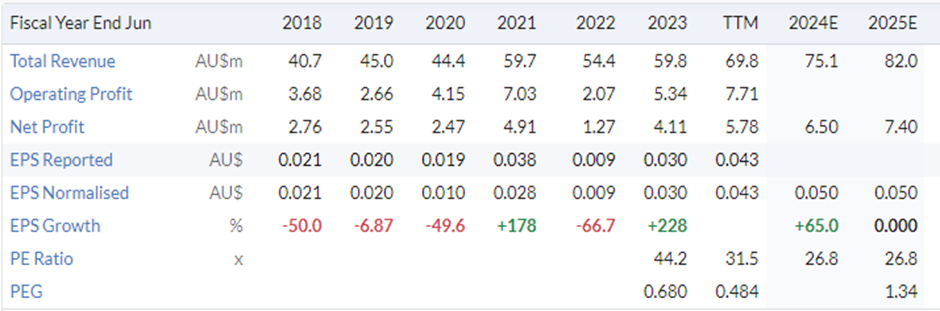

The last time I personally looked at VEE was in September 2023, where they had righted the ship after COVID impacted their ability to do business and profits had increased from a COVID induced low of $1.2m in FY22 to $4.1m in FY23. It is also a stock that Chris Batchelor had also discussed frequently.

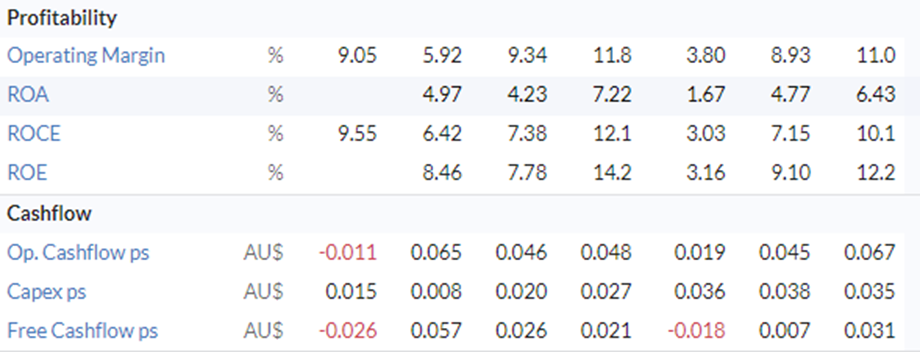

As you would hope and expect with a near tripling of profits, VEE’s profitability and cash flow ratios improved substantially from FY22 to FY23 and have returned to pre-COVID levels. At this time VEE’s share price was 64c per share but on the back of signing an exclusive worldwide agreement to design, manufacture and sell Sharrow propellers in October 2023 (which according to VEE have a global addressable market of US$2.6bn, with the annual new build market of US$338m) and Strategic Marine bringing forward their order of 12 gyros (resulting in VEE expecting gyro revenue to double in FY24 to $10.0m) VEE’s share price shot up over the dollar mark and is currently around $1.50, at the time of writing.

VEE have released their HY24 report, and it looks like the Momentum from FY23 is continuing. With revenue coming in at $37.5m up 37% for the half. Following suite, EBITDA and NPAT were up 65% and 92% to $6.9m and $3.5m for the half respectively. But for me, most importantly cashflow from operations…