Source: Vodafone FY25 presentation

Welcome back to our Stock Pitch series. We’ve covered several small caps recently; today I’m zooming out to take a look at a FTSE 100 heavyweight that’s comfortably outperformed the wider market over the last year.

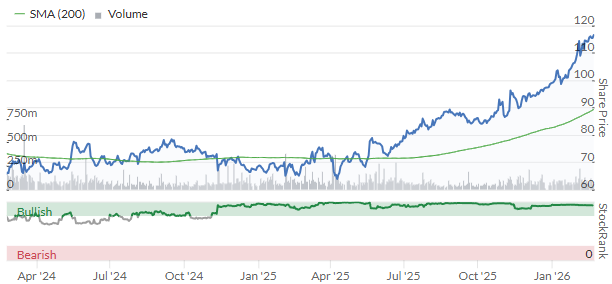

Shares in telecoms giant Vodafone (LON:VOD) have now risen by nearly 70% since the start of 2025. This rally appears to have gathered pace so far in 2026:

The Pitch

Vodafone has been steadily shedding its reputation as a value trap since CEO Margherita Della Valle became CEO in early 2023.

Revenue has returned to growth, debt has fallen and last year saw the first dividend increase in seven years. Earnings forecasts suggest double-digit EPS growth over the next year.

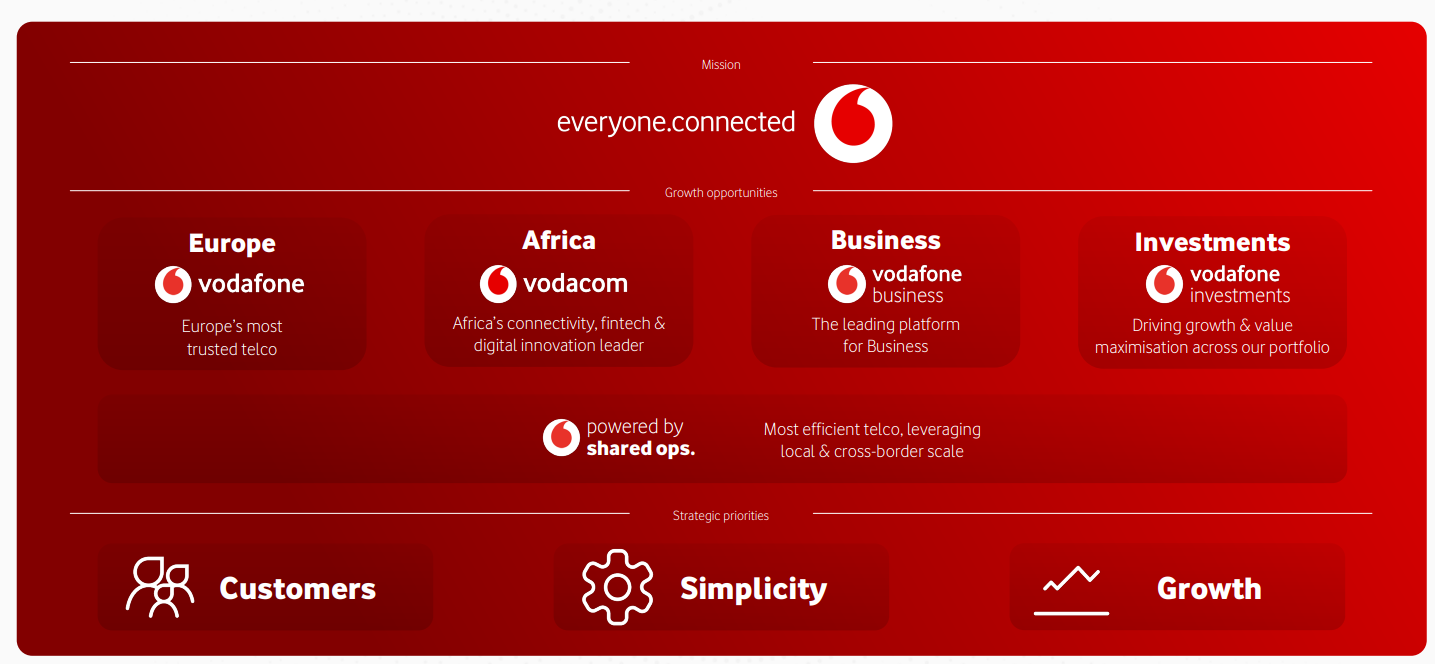

Ms Della Valle has achieved a long-held sector goal by reducing the number of network operators in the UK from four to three through the merger of Vodafone UK with Three. Elsewhere, a number of divisions have been sold, raising cash and creating a more coherent and manageable portfolio with plausible growth prospects.

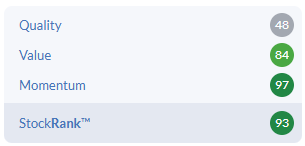

The StockRanks view this as a Turnaround, with strong value and momentum scores:

The focus is now on delivering long-needed improvements in quality metrics. Success could justify a sustainble higher rating and support a return to progressive dividend growth.

The Big Picture

Vodafone’s attractions as an investment fall into three main categories:

Europe: it’s one of the largest telcos in Europe, with 112m mobile customers, 19m fixed line customers and 14m TV subscribers. Vodafone is well positioned to become a major broadband supplier in the UK and expects to return to growth in Germany – its largest market – this year.

Africa: organic service revenue rose by 11.3% in FY25, a growth rate European operators can only dream of. Vodafone has 227m mobile customers and 92m financial service customers in Africa, but smartphone penetration is still only 64% and demand is growing fast.

Dividend & buybacks: the dividend returned to growth last year following a cut in 2024. Vodafone is also returning cash through buybacks and has repurchased €3.5bn of stock since May 2024, reducing the share count by 15% and supporting EPS and dividend growth. Shareholder returns are now…