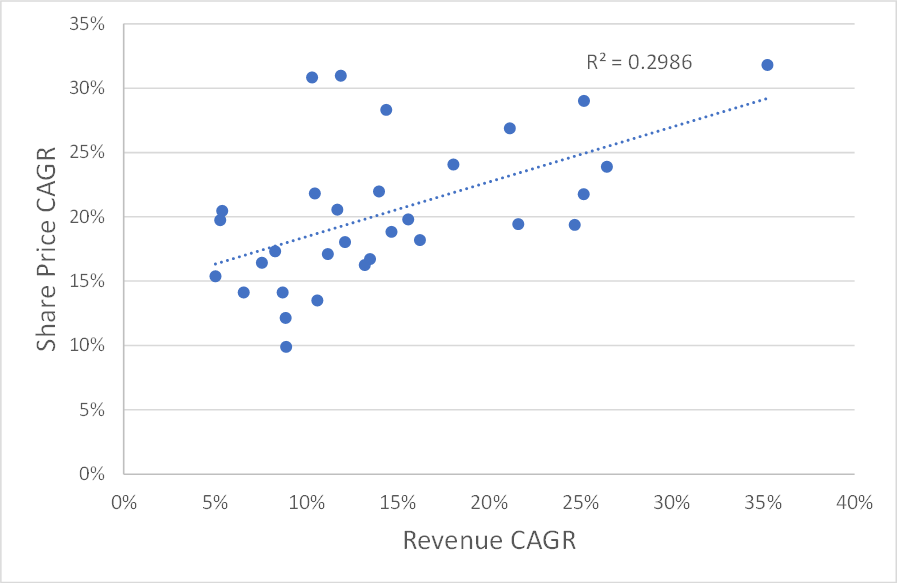

In last week's article, I looked at what investors could learn from the full list of multi-baggers from Ed's recent study. The evidence was clear: if investors had to pick one factor to look to find future multi-baggers, it would be the potential for rapid sales growth. Although operational leverage also aided strong returns, very few companies multi-bagged without seeing rapid sales growth. Here is the correlation I showed last week:

From this, it appears that investors seeking exceptional returns should simply screen for the fastest-growing companies in the market and invest in those. However, for this strategy to work, rapid historical growth rates would need to continue into the future. The big question is, how likely is this to happen?

Is revenue growth persistent?

The persistence of growth was analysed in a 2001 paper by Chan et al. called The Level and Persistence of Growth Rates. The authors concluded:

While some firms have grown at high rates historically, they are relatively rare instances. There is no persistence in long-term earnings growth beyond chance.

It doesn't look good, but the data used in the study ended in 1997, which was a long time ago. Many aspects of financial markets have seen significant shifts over the last two decades. Perhaps the rise of global tech and biotech firms means that rapid growth is more likely to continue in today’s markets?

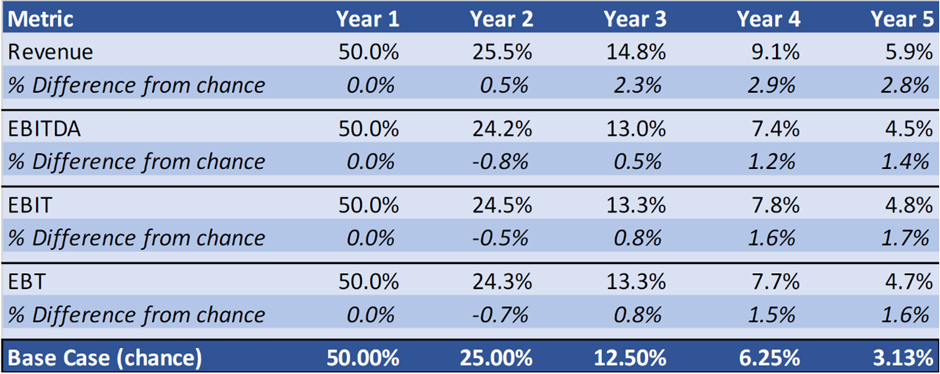

Thankfully, Hedge fund Verdad Capital has updated these findings using data from 1997-2021. Their methodology involved looking at which proportion of stocks with growth rates above the median remained above the median over subsequent periods. They compared the results to what you'd expect from pure chance, for example by flipping a coin, to see if growth would be higher or lower than the median. Here are the results for US stocks:

So, it seems that after one year, growth rates are effectively determined by chance. Over the long term, there appears to be some persistence of growth. For example, 5.9% of companies with sales growth rates above the median had sales growth rates above the median five years later. If this were purely determined by randomness, it would be expected that just 3.1% of them would. However, given that there appears to be no persistence above chance over…