FTSE 100 commodity giant Glencore (LON:GLEN) has been one of the biggest beneficiaries of the war in Ukraine. The Swiss-based group has opted to continue owning thermal coal mines (used to generate electricity), rather than selling them. This has enabled it to play a big role in filling the supply gaps created by the shortfall in Russian coal exports.

Coal generated half Glencore’s profits during the first half of this year – more than the entire group made during the same period in 2021.

Shareholders are set to benefit from this windfall. Dividends and buybacks are expected to total $8.5bn in 2022. That’s nearly 10% of the company’s market cap.

However, while Glencore shares have outperformed the FTSE 100 and coal-less rival Rio Tinto, the company’s share price action since the start of the conflict has looked fairly muted to me:

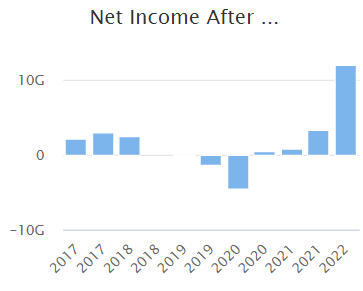

Especially when we compare this to the threefold increase in Glencore’s profits over the last year:

One possible explanation is that the smart money saw the energy supply crunch coming, even before the war brought the situation to a head. Glencore’s share price has risen by 190% over the last two years:

Another explanation might be that this is just another cyclical peak, and that profits will soon slump. After all, Glencore shares are – remarkably – still no higher than when the company floated at the peak of the last big commodity bull market, in 2011:

Glencore is positioning itself as an energy transition firm that’s running down its coal assets responsibly, while investing in energy transition commodities such as zinc, copper and cobalt. I think CEO Gary Nagle may be painting a somewhat rose-tinted view, but I can see this story.

To some extent, I also share Glencore’s view that responsible ownership may be a better alternative to divestment.

While mining profits will always be linked to commodity prices, Glencore’s trading division has historically been able to deliver reliable profits, even during mining downturns. Can the company avoid a slump and deliver sustainable growth?

I’ve been taking a fresh look at Glencore’s financial metrics to find out more.

Value: cyclical risk

A ValueRank of 76 suggests that Glencore shares could offer fairly good value. Some of…