Good morning!

Vislink (LON:VLK)

Vislink is a group that I've written about a lot here in the last year, as it has always struck me as being very good value, and still does. My rationale for buying the shares at 30.5p was set out here on 25 Mar 2013, and that remains a good summary of the current investing case.

The shares re-rated to about 50p later last year, but have since slipped back to about 40p (for chartists note that is a 50% retrace, which apparently can be a good point to look at buying, once something has stopped falling anyway). The only reason I can find for the share price weakness is the company's decision to move from a full Listing to AIM. This strikes me as an entirely logical step for a £47m market cap (at 41p per share), acquisitive technology company to take - i.e. it was an anomaly having a full Listing in the first place. However, this move to AIM seemed to spook some private investors, who invented conspiracy theories about management's motives for the change, and will also have probably triggered some Institutions into becoming forced sellers (those whose remit means they are not allowed to hold AIM Listed shares). Some private investors also have an aversion to AIM, which is understandable, as it is arguably the unregulated Wild West of the investing world - plenty of very good companies are on AIM, but there's a lot of dross too - because wrong-doing is rarely punished, sadly, which attracts wrong 'uns.

Vislink has an ambitious Executive Chairman, John Hawkins, who has been following a strategy of rationalising the existing businesses to make them more profitable, then growth by acquisition (something he's done many times before). The longstanding strategy is to build Vislink into an £80m turnover group, making £8m profit by the end of 2014.

This strategy seemed to be counter-productive with investors, since people seemed to fret over whether the company could achieve this target on time, rather than being pleased with the progress being made to date.

Vislink has put its excess cash to work today, with the announcement of a takeover for £14.9m of Surrey-based Pebble Beach Systems, which is a "leading developer and supplier of automation, 'channel in a box' and content management solutions for TV broadcasters, cable and satellite operators". This looks a good fit with Vislink's existing business, which is mainly the supply of high-end specialist cameras for broadcasters (e.g. the cameras which show the driver's eye view of F1 races).

Pebble Beach itself has £5.9m cash, so that brings down the net consideration to £9m. This has been funded using Vislink's own cash, plus a new £3m term loan, and £7m overdraft. The vendors will also be locked in to Vislink for two years, with the issuance of £2m in new Vislink shares. That's very little dilution, for what is quite a decent-sized acquisition, so to my mind this looks a good deal for Vislink shareholders.

Most importantly, Pebble Beach is profitable, and reported £5.6m turnover, and £1.3m profit before tax for the year ended 30 Jun 2013. So that gives Vislink a material chunk of additional turnover & profit (at high margins).

In my view broker forecasts for Vislink look too low. I reckon the company is heading for 4-5p EPS this year, so put that on a PER of say 15, and the share price could be 60-75p, useful upside on the current price if my calculations turn out to be right. It all depends on execution of course - the company's business model lacks much recurring revenue, so you cannot be entirely sure that their pipeline will convert into sales in a reliable manner.

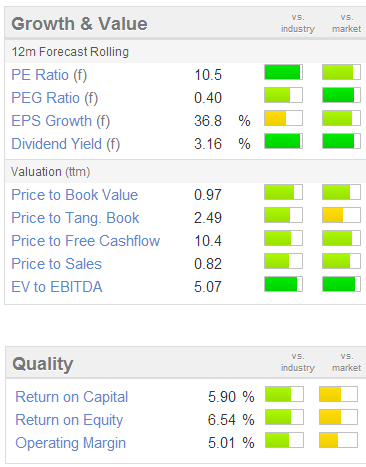

Note that on the existing broker forecasts for Vislink (2.85p EPS for 2013 [to be reported shortly, on 26 Mar 2014], and 3.9p for 2014) these shares are showing strong green (i.e. good!) on the Stockopedia growth and value graphics shown on the right.

Note also the healthy dividend yield.

The market shares my positive view of today's news, and I note that Vislink shares are currently up 7% to 44p at the time of writing (08:19).

I think the Chairman deserves credit for taking time to seek out a good acquisition. His comments below also indicate that there are some recurring revenues from the acquisition, which could help re-rate the shares if the quality of earnings is improved (i.e. more recurring revenues, and less reliance on one-off sales);

Pebble Beach Systems is a perfect fit given our focus on product leadership and it will enable us to offer our global broadcasting clients a complete scene-to-screen solution. Additionally, the acquisition fits perfectly into our long term strategy of acquiring software and services capability that we hope to drive recurring revenues for the Group.

I'm not concerned by the level of gearing being used on this deal, which looks modest, and I'd much rather the company put its surplus cash to use, rather than continuing to sit on a surplus cash pile, earning zilch in interest from the bank.

So overall, this deal gets a thumbs up from me, and I shall report on the company's results in more detail next week. Hopefully we should also get some revised broker forecasts for 2014 and 2015 then too.

EDIT: I see that house broker, N+1 Singer, has upgraded their forecasts for 2014 from 3.6p to 3.9p EPS (fully diluted), and for 2015 from 3.9p to 4.4p EPS, so the shares are looking cheap on a PER basis on broker forecast, and there could be upside on those earnings figures in my view.

2nd EDIT: Equity Development are doing a results presentation Webinar for Vislink next Weds at 1pm, here is the registration link. I was very impressed with their webinar last week with Fairpoint management - it's basically just like a results presentation in real life, and you can submit questions in a text box. So much more efficient than a 6-hour roundtrip into London for me.

PPHE Hotel (LON:PPH)

This is a hotels group which at 322p per share has a market cap of around £134m. This is a European hotel group that was established in 1989, and has since growth to 38 hotels, including the Park Plaza brand (of which there are six in London).

Preliminary results for calendar 2013 are published today. There has been a 16.7% increase in total dividends for the year, to 14p per share, which gives a useful yield of 4.3%. However, I am always wary of highly indebted companies which pay big dividends, and for me the deal-breaker here is the amount of debt.

The Balance Sheet shows net assets of E290.6m, of which E35.4m are intangibles, so E255.2m net tangible assets. Working capital looks OK, with current assets of E70m almost exactly matched with current liabilities of E70.4m. That's fine for a business like a hotel, which has very little requirement for stock (which is only E1.3m in this case, just food & drink I assume).

However, it's the long term liabilities that worry me here. These total up to E763.3m, including just over E500m of bank debt, and E191.6m in advance payments from "apart-hotel unit holders". This looks like some kind of deferred income, but is not matched with equivalent cash balances, so it looks to me as if up-front payments from customers are providing a substantial part of the financing for the whole group. I don't like that model, which is quite common in the travel sector.

EBIT was E60.2m (up from E57.5m in 2012), but almost half of that was absorbed with financial costs of E30.2. There's also a further financing charge of E10.8m related to the apart-hotel unit holders, partly offset by some finance income.

Therefore the key risk here is a rise in interest rates, to the extent that has not been hedged, and the risk of withdrawal of bank facilities, say in the event of a Covenant breach, or if we have another international banking crisis from the expected financial meltdown from China's credit bubble.

On the other hand, you could argue that this is probably the stage in the economic & credit cycle where we should be seeking out highly geared companies, as providing they survive then all the upside from improving economic conditions flows through to equity, which could give multi-bagger potential possibly?

Overall, my feeling is that the Balance Sheet is currently too scary, and I'm not prepared to take the risk. Today's results recap on the Dec 2013 refinancing, its largest to date, with a LTV of 65% on hotels valued at E545m. Overall I could cope with 50% LTV, but 65% seems a bit too aggressive, particularly as there is additional quasi-debt from the apart-hotel unit holders. This type of highly geared, expanding group, tend to be constantly refinancing, which is fine as long as Banks are happy to keep lending. One of the first Receiverships I worked on in 1990 was a rapidly expanding, highly geared leisure group - when Recession hits, the risk is that the Banks just call in the loans. Everyone seems to assume that interest rates will remain low forever. They might not. What happens if the Bank of England loses control of interest rates - i.e. if there is a run on sterling, and they are forced to raise interest rates to say 5-10% to defend the currency? It may sound fanciful, but it's happening right now in emerging market countries. So a highly indebted country like the UK is not necessarily immune from these risks. Maybe I'm too cautious, but I just have an aversion to highly geared Balance Sheets.

A number of friends hold this share, and know more about it then I do, so hopefully people will add their comments in the comments below, please always feel free to do so, where you can add useful points to my initial review comments.

Essenden (LON:ESS)

This company operates ten pin bowling leisure facilities in the UK. It's been an excellent turnaround situation, and the market has given their results today a big thumbs up, with the shares rising 33% to 100p.

I did look at this one a few months ago, but unfortunately rejected it because of the weak Balance Sheet. So it just shows that in a bull market, taking a prudent view on Balance Sheet risk can mean losing out on some spectacular gains. So maybe I should be a bit more flexible on that front?

Essenden reports today on the 52 weeks results to 29 Dec 2013. The headline profit before tax of £3.6m seems to have been flattered by some one-offs, including a £1.4m profit from reversing an impairment provision, and £1.6m release of an onerous lease provision. So I wonder if the market has taken into account these one-offs, or has just roared up on the inflated headline profit numbers?

The company says that adjusted profit before tax rose from £1.5m to £1.9m from 2012 to 2013, so that is the figure that should be used in valuing the company, in my opinion - since one should always be mostly focussed on the underlying, i.e. repeatable profit, not figures that are distorted up or down by one-offs.

I don't like the way this company reports its net debt. They ignore the £18m debt on the Balance Sheet in long term creditors, and report net cash of £2.1m. That is highly misleading in my opinion. The true position is substantial net debt of £15.9m, which is material to the valuation, since the market cap is now £21.5m at 100p per share.

The company provides a reconcilation of net debt in note 10 of today's results, which shows the large, £15.8m debt owed to shareholders through loan notes. So it is essential in valuing the company to understand the terms of these loan notes. It's debt, so should be included in net debt.

On checking the most recent (2012) Annual Report, in note 19 the terms of the shareholder loan notes is explained. It's a very unusual situation, and kicks the can down the road in terms of repayment, which is due in 2020, as follows;

The bank loans and overdrafts are secured by fixed and floating charges on all of the group’s properties and assets. The Essenden loan notes are £1 principal amount, zero coupon, perpetual notes which are freely transferable and are listed on ISDX. They are fully repayable at par on the occurrence of certain specified events, including a change of control of Essenden, an insolvency event or a change in operating activity. They were recognised on the balance sheet at their initial fair value less amortisation of the initial discount within financial liabilities due after more than one year, as there is no fixed redemption date and no current obligation to make any redemption within one year. They are subsequently measured at their fair value accounting for any change in their redemption date. As at the year end these loan notes was reviewed and no change to the redemption period was made which remains as October 2020 when it is anticipated there is likely to be sufficient cash surpluses to redeem the loan notes. Their fair value at 30th December 2012 was £7.7m (1st January 2012: £5.4m) based on their price on ISDX.

So that seems to me as if the company will need to build up its cash reserves over the next few years, in order to repay the loan notes in 2020. That is likely to restrict what dividends it can pay in the meantime. There is no dividend at the moment.

I really don't like the way this company tries to gloss over the existence of these loan notes. It is material to the valuation, and should be far more prominent in their results narrative.

Having said that, they have clearly pulled off a strong turnaround, and I note that the new year has started very well indeed, with LFL sales up 13.5% for the 11 weeks to 16 Mar 2014. With a fixed cost base, that should produce a geared return to the bottom line.

How to value it? I think with the complication of the loan notes, being a large, deferred liability, and the one off boosts to 2013 results, the share price is probably up with, or maybe ahead of events at 100p. It could go higher though, as I think many people buying the shares may be unaware of the loan notes, and are just ignoring them in valuing the company. They don't seem to provide an adjusted EPS figure either. So taking the £1.9m adjusted profit before tax, taking off say 20% notional tax, gets to just over £1.5m earnings. Divide that by 21.4m shares in issue, and I arrive at a normalised EPS figure of about 7p per share for 2013.

So my estimate of underlying EPS compares very unfavourably with the 16.7p EPS quoted in today's results, which working backwards equates to £3.6m earnings, which of course is the figure that is heavily flattered by a zero tax charge, but also the big one-off boosts to profits mentioned above from releasing provisions. So 16.7p should absolutely not be the figure that you value the company on, as it's not a sustainable earnings figure. I suspect bulls are probably saying, oh it's only on a PER of 6, and has no debt. Both those statements are badly wrong!

Given all the debt, which you could apply a discount to because it's deferred until 2020, I think a valuation of say 12 times my sustainable EPS figure of 7p makes sense - that also allows for 2014 earnings rising a decent amount on the back of improved current trading. Therefore I'm coming to a valuation of about 84p per share which looks sensible to me. So at 100p currently, my conclusion is that these shares have probably got ahead of themselves, on people possibly getting carried away with the headline numbers today, and not working them through to what is sustainable, and adjusting for the real level of debt.

Still, it's been a spectacular 4-bagger for those who spotted the opportunity a few months ago, and a good example of how seeing the glass half-full, rather than agonising over the Balance Sheet, can pay off very nicely in a bull market! Also bear in mind that a lot of buyers in a bull market are really not crunching the numbers properly, which is great on the way up, but not so good as that type of buyer tends to lose interest quickly once the shares stop going up.

I'm not negative on the company at all, but hope the figures above demonstrate that perhaps the valuation is now up with events, after a spectacular recent rise? It's important not to get too greedy with these things.

EDIT: Many thanks to Martin who has pointed me in the direction of yesterday's RNS from Essenden, which sets out proposed terms for conversion of the loan notes into shares. I think it also vindicates my view that the loan notes were highly material to the company's valuation, and should not have been ignored by investors.

The proposal is to more than double the shares in issue, by converting all the shareholder loans into equity. This will result in 49.9m shares in issue, but with the debt extinguished. So that's a double-edged issue for shareholders - the Balance Sheet is fixed, but they are seeing heavy dilution.

So trying to work out a proforma valuation, I would take the £1.9m adjusted profit, and adjust it backwards to eliminate interest cost, since the group will now genuinely be debt-free. That would take you up to about £3.3m profit, and with current trading strong, this might mean about £4m profit for 2014. Take off say 20% notional tax (although they might have b/f tax losses, but I would still like to value it on a full tax charge going forwards) and that gives earnings of £3.2m. With the enlarged issued share capital of 49.9m, that gives my estimate of 2014 EPS at 6.4p. What PER to put that on? I would say maybe 12-14, so that means a share price of 77-90p. Therefore the current share price of 100p looks in the right ballpark, maybe a little on the high side?

Also bear in mind that unless there are lock-in provisions, then this is likely to lead to a big overhang in shares, so the comany's broker would probably need to organise a secondary Placing of these newly issued shares.

As an investment, the company is now looking much more attractive, with that debt cleared. However, holders are seeing heavy dilution in order to clear the debt. So make of that what you will. But it very much reinforces my view that proper Balance Sheet analysis is vital - you cannot just ignore debt, as this situation proves.

That's it for today. Do please feel free to comment below, especially if you have more detail on companies concerned - always bear in mind that most of my comments are just a quick view, as I try to cover about 500 companies, so it's really not possible for me to know all the ins & outs of each company.

Regards, Paul.

(of the companies mentioned today, Paul has a long position in VLK, and no short positions)

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.