Good morning!

Just in case you missed it, here is the link for yesterday's report, as I added another section on Victoria (LON:VCP) (in which I hold a long position) after the 1pm email was sent out.

There were also some fascinating comments from readers, about the chronology of how the Chairman managed to take over a sleepy company, and generate enormous wealth for himself - and it has to be said, other shareholders too.

So this is a tricky situation - where an outlandishly lucrative incentive scheme for management (which I would normally oppose vehemently) seems to have actually worked for the benefit of everyone - just look at the share price chart over the last few years! Food for thought anyway.

Staffline (LON:STAF)

Share price: 888p (up 3.2% today)

No. shares: 27.7m

Market cap: £246.0m

(at the time of writing, I hold a long position in this share)

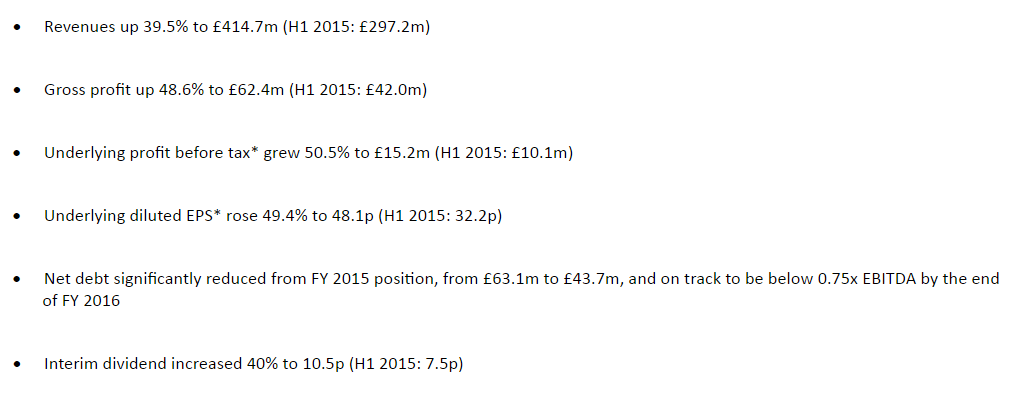

Interim results - the financial highlights in today's interim results (6m to 30 Jun 2016) look very impressive. Note the prompt reporting schedule too - only 27 days to produce published interim results - to me that demonstrates good financial controls are in place.

Note that most of the growth has come from acquisitions. However, organic growth was still very good, at 14%.

Going through these numbers, I really cannot see any justification for the Brexit-related plunge in share price. It doesn't seem to make sense, so this is looking like a good buying opportunity to me.

Current trading & outlook comments all sound positive;

The second half of 2016 has started well. Our sales pipeline, which remains significant, will support continued growth. As a result, we remain on track to deliver current expectations for FY 2016.

Furthermore, Staffline continues to work towards its longer term growth ambitions. We remain responsive and focused on adapting to new regulations and government change. Whether this is the NLW or the potential changes which the UK's exit from the EU may bring over time, our scale and capabilities mean that organisations increasingly look to Staffline to ensure their access to a flexible and efficient workforce.

Our Employability division, PeoplePlus, is making good progress and we expect the enlarged business to continue to have a significant impact financially and operationally in 2016 and beyond.

In addition to driving organic growth, we continue to identify further bolt-on acquisition opportunities, in particular within our Staffing business. We remain in discussions with a number of companies where we see the potential to develop our reach and offering further.

As an expression of our confidence in the Group's prospects, the Directors therefore propose to increase the interim dividend by 40%, from 7.5p per share declared H1 2015, to 10.5p per share. This dividend will be payable on 15 November 2016 to shareholders on the register at 14 October 2016. The ex-dividend date is 13 October 2016.

Broker forecasts - the average of 2 broker forecasts I've seen this morning is 114.4p EPS for 2016. So at 888p, I make that a PER of only 7.8 (I've checked my maths today!)

Brokers are being quite cautious for 2017, and the average EPS is 120.7p, so the PER drops to 7.4. I wonder if brokers are being too conservative in their 2017 & 2018 forecasts? Given how well managed this group seems, and the excellent track record, I don't see why such caution is justified. So personally I see upside potential on existing forecasts, which if I'm right, would mean the PER is even lower than the figures above.

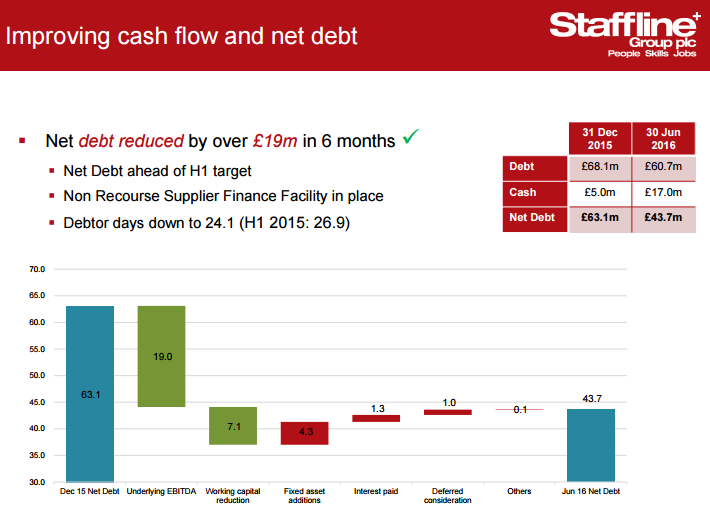

Net debt - so if the PER is this low, is the group laden with debt then? There is some, but it's come down a lot in the last 6 months, and is forecast to be fully paid off by the end of next year;

Net debt significantly reduced from FY 2015 position, from £63.1m to £43.7m, and on track to be below 0.75x EBITDA by the end of FY 2016

As you can see, the EBITDA multiple is modest.

Private investor lunch

There are still some spaces left for a private investor lunch with Staffline, on Monday which the company has laid on through its advisers, Buchanan. This is a terrific initiative, and I'm very supportive of companies which reach out to private investors. After all, it's the private investors who create the liquidity, and set the share price. So ignoring this huge part of the market is pretty bonkers. Here are the details;

A presentation for private and retail investors will be held at 1.30pm on Monday 1 August 2016 at the offices of Buchanan, 107 Cheapside, London, EC2V 6DN. Admittance is strictly limited to those who register their attendance for the event by 5pm Friday 29 July 2016 with Buchanan.

Here are the contact details for Buchanan, to book a place;

020 7466 5000 or staffline@buchanan.uk.com

Balance sheet - I'm not keen on this. When you write off the intangibles, NTAV becomes negative, at -£36.1m. This is the typical problem for acquisitive groups - intangibles pile up at the top, and debt builds at the bottom.

However, in this case, the working capital position looks OK, and debt levels are fairly moderate, so I can live with the balance sheet, whilst flagging that it could do with strengthening - that should happen over time, as debt is being repaid quite rapidly.

Here is a useful "bridge" showing how cashflows have affected net debt in the last 6 months. This demonstrates the cash generative nature of the business, and its ability to pay down debt fairly quickly;

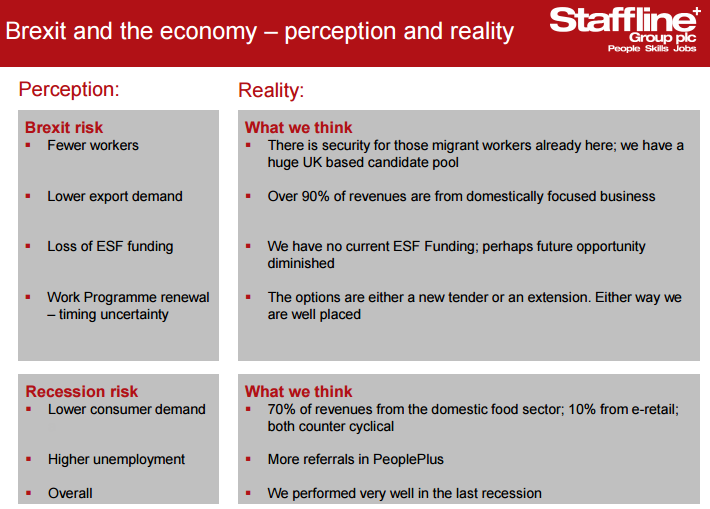

I also liked another slide from management today, explaining their view on how Brexit will affect them (basically, not very much);

Q&A with the CEO

(this is from memory, so I hope is broadly accurate, but it's not verbatim)

Q1. Impact of Brexit? e.g. are E.Europeans returning home, due to feeling unwelcome, or the value of sterling wages falling? What proportion of your workers are E.European?

A1. There have been isolated incidents of racism in the workplace, very regrettable, and hopefully won't recur. Min wage in Poland is very low - approximately £1 to £1.40-ish, so even with the weaker pound, UK wages are still very attractive. So we're not seeing E.Europeans returning home as a trend, at all. Of our 45k workers, 75% are E.European - employers like them, as they have a good work ethic. Even if incoming workers are restricted, the 3m already in the UK are likely to be allowed to stay.

No impact on trading from Brexit, because 70% of our workers are in the food industry, and 10% in ecommerce. These sectors should be fine, even in a recession. We performed very well in the last recession.

Q2. One broker has slashed growth forecast to only 5% in 2017 & 2018. Is there upside on this?

A2. There are quite wide variances in the 3 main brokers covering us, who see the macro picture differently. We just get on with running the business. Our plan remains to reach £1bn turnover, and £50m profit, although £45m is probably more realistic. We'll do our damnedest to achieve that target.

Q3. Seasonality - I see that, whilst profits are up in H1 2016 vs H1 2015, profit is actually down sequentially - i.e. when compared with H2 of 2016. Is this a downturn, or seasonality?

A3. It's seasonality - profit is split roughly 40:60 between H1 & H2. This is because of operational gearing - fixed costs, but clients require more staff in H2.

Q4. Are you concerned about the balance sheet weakness, once intangibles written off?

A4. No, because working capital position is fine. Also, debt is modest relative to EBITDA, which is the key consideration for us.

Q5. Is there a risk of the welfare to work contracts ending?

A5. The CEO explained how the contracts work, and that they are indeed nearing the end. However, they are extended, or replaced with something very similar. Welfare to work programmes are very successful - saving £4 in benefits for every £1 in cost. So there is zero chance of Governments cancelling these type of contracts. Also, a tighter labour market would make it easier to place benefit claimants in work.

Q6. The cashflow bridge looks good, but is the working capital improvement a one-off, and will it reverse in future?

A6. Actually the working capital was unusually adverse at 31 Dec 2015, so has righted itself now. Therefore the position at 30 Jun 2016 is normal.

My opinion - obviously I like this share, and hold some personally (bought on the recent dip below 800p, so quite nicely timed for once!).

In my view the company deserves a higher rating - I think a PER of say 10-12 would be appropriate. That implies a share price of c. 1200-1440p, if we work on the basis of 120p EPS for this year/next year. That's usefully higher than the current price of about 888p.

It seems to me that Staffline has recession-proof characteristics, so it's difficult to understand why the shares have sold off so much - perhaps on fears that its 75% E.European workforce may gradually disappear?

I suppose there's a regulatory risk as well - if the Govt decides to push employers into taking on staff on permanent contracts, rather than more flexible, and some say exploitative, agency workers?

Overall though, I like it a lot - the current price just seems too low to me. Obviously DYOR as usual - and if you spot something I've missed, then please post in the comments below, as I'm itching to buy more of this one at the moment!

I've asked the company if the CEO would like to do an audio interview with me, so hopefully that might happen in due course.

Norcros (LON:NXR)

Share price: 160p (up 6.8% today)

No. shares: 61.0m

Market cap: £97.6m

(at the time of writing, I hold a long position in this share)

AGM trading statement - covering the 13 weeks to 3 July 2016.

Here's my report from 20 Jun 2016, when I met with management just before the Brexit vote. They sounded relaxed about the risk of Brexit, so I wonder how they're feeling now, just over a month later?

Q1 has gone according to plan;

The Group's overall trading for the first quarter was in line with the Board's expectations.

Norcros is an interesting buy & build group, where management seem to be executing well - having made several good, and reasonably-priced acquisitions.

Group revenue for the 13 week period was 18.5% higher on a constant currency basis compared to the same period last year and 13.0% higher in Sterling terms reflecting a weaker South African Rand. On a constant currency like for like basis (excluding acquisitions*) Group revenue was 2.6% higher than the same period last year.

Once again, it's the South African business which is powering forward, taking up the slack from a lacklustre UK performance.

Brexit comments are non-specific;

Although it is too early to judge the effect the EU referendum result may have on activity levels in our businesses the Board is monitoring the position and will effect mitigating actions in response to any change in demand.

Bear in mind that a lot of their products are manufactured in the Far East, and would therefore be invoiced in US dollars. So I imagine that there's likely to be some adverse forex impact, if current £:$ levels are maintained. Probably offset, or rather deferred by hedging arrangements.

Outlook - the CEO sounds happy with full year prospects (which is for y/e 31 Mar 2017).

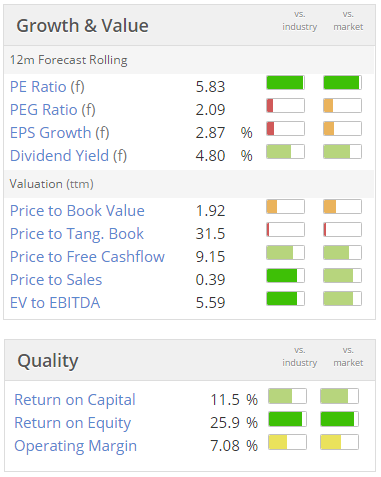

Valuation - it looks dirt cheap on conventional valuation measures;

Although as I've mentioned many times before here, you do have to factor in the large pension fund. Bond yields being low, is tending to worsen pension deficits. Although in this case, the company announced comfortably manageable overpayments in its last results statement, as follows;

I am pleased to report that we reached agreement with the pension scheme Trustee on the 2015 actuarial valuation and recovery plan. The actuarial deficit at £73.5m (2012: £61.9m) reflects the impact of historically low gilt yields and the recovery plan of £2.5m per annum plus CPI for the next ten years represents a satisfactory outcome in the light of that valuation and the previous plan of £2.1m plus CPI per annum.

When I discussed the pension deficit with management, they said they're mindful of it, but it's a manageable issue. The scheme is mature, and is shrinking quite rapidly now, due to the average age being in the late 70's.

Dividends - note the divi yield is attractive, at 4.8%, with a good progression in divis in recent years, rising by almost 13% p.a.

My opinion - so far, so good. I think the valuation is attractive. Sure, the pension deficit is a headache, but it's more than factored into the price, in my view. Actuarial deficits are arguably over-stating the downside at the moment, due to extremely low gilt yields. So the actual cash cost to Norcros is likely to be a good deal less than the £73.5m actuarial deficit, and of course spread over many years.

If they can keep bolting on good quality, reasonably-priced, complementary businesses, then over time the pension deficit should become less of an issue.

Of course, if we go into a proper recession, then earnings are likely to fall sharply. However, the group is in very much better shape than it was last time recession hit. Personally, I don't think a prolonged or deep recession is likely, but others may differ on that point.

Flybe (LON:FLYB)

Share price: 39.3p (down 6.5% today)

No. shares: 216.7m

Market cap: £85.2m

(I no longer hold a long position in this share - have sold)

Q1 2016/17 trading statement - there's lots of data in this announcement, and nothing is specifically said about performance versus market expectations. The section below seems to be sending mixed messages, making it difficult to interpret;

Flybe reports a solid start to the year, with sustained passenger and revenue growth, in a challenging revenue environment with significant yield pressure across the sector driven by a slow-down in demand growth, accelerating industry wide capacity growth and repeated industrial unrest in France which accounts for c12% of Flybe's seat capacity.

Taking a simplistic approach, these particular stats don't look good to me;

9.1% decrease in revenue per seat6 to £47.95 (Q1 2015/16: £52.73)

3.2% reduction in UK cost per seat (including fuel) from £53.24 to £51.52

So revenue per seat is falling considerably faster than cost per seat. Also note that there's a £3.57 loss per seat implied from these numbers. Hmmmm.

In the current trading section, it is stated that revenue per seat on current bookings is down 11% on last year, so a worsening trend.

My opinion - I've seen one broker note today, who has slashed forecasts heavily. So forecast EPS for this year has been cut from 10.2p to just 3.0p. Although the share price was already telling us that nobody thought the old figures would be hit.

It's yet another disappointment, from this very disappointing company. It's a turnaround that never quite seems to happen, but again that's now in the price already.

There could be value from a takeover approach - it's a lot of company for a market cap of now only £85m.

However, for me this is one disappointment too many, and I'm currently in the process of ditching my position in the company today. The load factor dropping to 70% is worrying me, and I think it's possible that this company may never move back into proper profitability.

Sod's Law being what it is, no doubt there'll be a takeover approach tomorrow morning!

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.