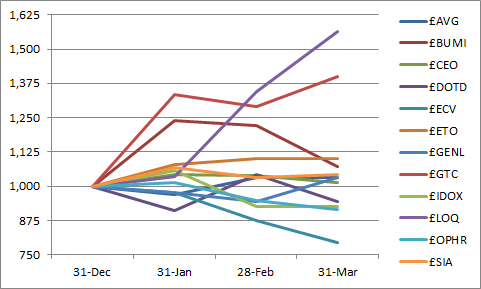

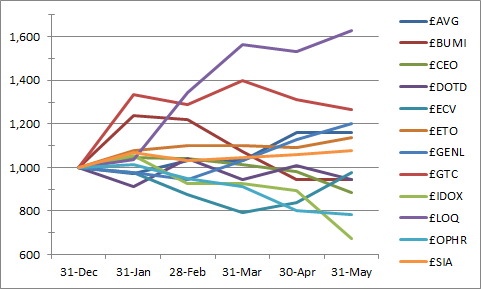

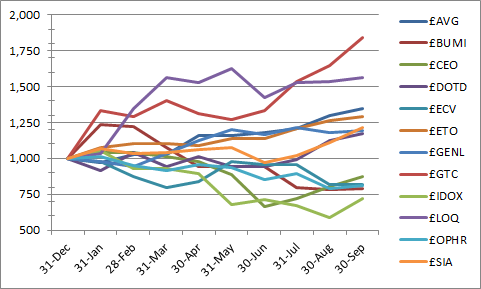

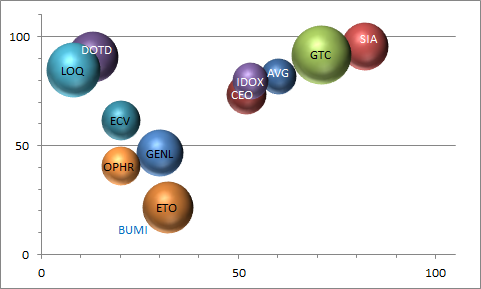

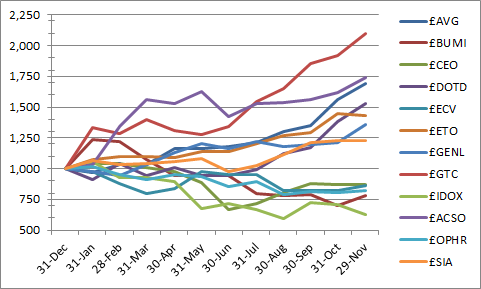

In a similar vein to the '12 for 2012' portfolio experiment I ran through 2012, I've chosen the following 12 stocks to track throughout the year (amongst others):

| 31-Dec | 31-Mar | 30-Jun | 30-Sep | 31-Dec | % change | Dividends | |

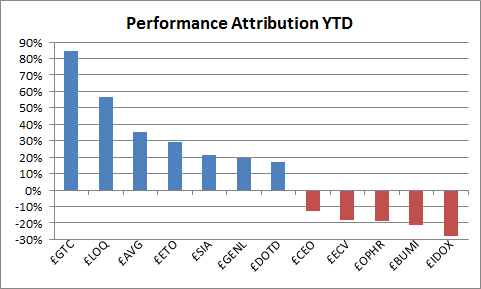

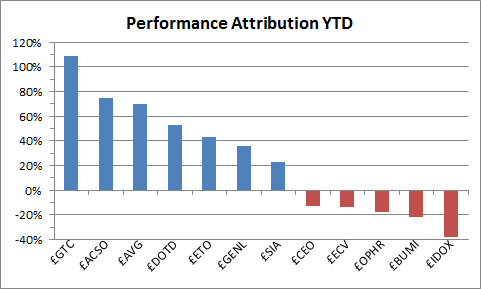

| Avingtrans (LON:AVG) | 1,000 | 1,030 | 1,179 | 1,365 | 1,689 | 68.9% | 22 |

| Asia Resource Minerals (LON:ARMS) | 1,000 | 1,073 | 943 | 789 | 836 | -16.4% | |

| Coastal Energy Co (LON:CEO) | 1,000 | 1,012 | 665 | 875 | 862 | -13.8% | |

| dotDigital (LON:DOTD) | 1,000 | 945 | 945 | 1,173 | 1,694 | 69.4% | |

| Eco City Vehicles (LON:ECV) | 1,000 | 795 | 955 | 818 | 750 | -25.0% | |

| Entertainment One (LON:ETO) | 1,000 | 1,101 | 1,136 | 1,293 | 1,527 | 52.7% | |

| Genel Energy (LON:GENL) | 1,000 | 1,032 | 1,164 | 1,193 | 1,368 | 36.8% | |

| Getech (LON:GTC) | 1,000 | 1,400 | 1,342 | 1,853 | 2,009 | 100.9% | 9 |

| Idox (LON:IDOX) | 1,000 | 926 | 713 | 728 | 608 | -39.2% | 6 |

| accesso Technology (LON:ACSO) | 1,000 | 1,564 | 1,423 | 1,564 | 1,992 | 99.2% | |

| Ophir Energy (LON:OPHR) | 1,000 | 914 | 855 | 810 | 800 | -20.0% | 150 |

| SOCO International (LON:SIA) | 1,000 | 1,044 | 973 | 1,213 | 1,219 | 21.9% | 112 |

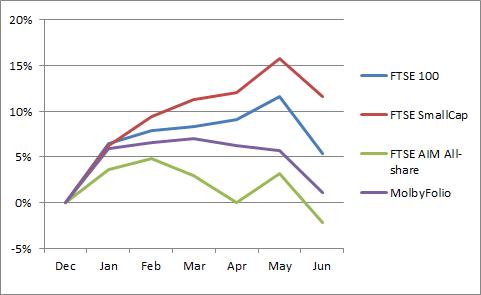

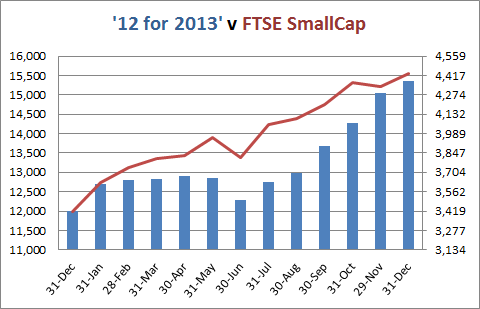

| Portfolio value (£) | 12,000 | 12,836 | …