Good morning and welcome to Wednesday's report - the Agenda is now complete. It's an awfully long list to digest but the good news is that there are hardly any profit warnings!

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

GSK (LON:GSK) (£58.9bn) | Sales +2%. Op profit +50% to £2.2bn helped by accounting methods. Guidance unchanged. | ||

Barclays (LON:BARC) (£42.6bn) | Ahead of expectations, PBT £2.7bn vs. £2.5bn forecast (Reuters). | ||

HALEON (LON:HLN) (£34.0bn) | Reiterates FY 2025 guidance. Organic revenue growth 4-6%, organic op profit ahead of this. | ||

Glencore (LON:GLEN) (£31.8bn) | Production guidance unchanged except for 5% reduction to energy coal’s range. | ||

Prudential (LON:PRU) (£21.0bn) | Q1 new business profit +12% to $608m, consistent with guidance for FY growth of more than 10%. | ||

Coca Cola HBC AG (LON:CCH) (£13.6bn) | Organic volume +1.8%, organic revenue +8.7%. Reiterating financial guidance for the year. | ||

Smith & Nephew (LON:SN.) (£8.7bn) | Underlying revenue growth 3.1%. Full year guidance unchanged. Includes $15-20m tariff impact. | ||

Melrose Industries (LON:MRO) (£5.5bn) | Q1 in line with expectations. Guidance unchanged but excludes any tariff impact. | ||

Taylor Wimpey (LON:TW.) (£4.2bn) | Full year guidance reiterated: operating profit of £444m. Small reduction in final dividend. Order book at 27 Apr was £2,335m, versus £2,093m last year. H1 25 margin expected to be lower than H1 24 due to the return of build cost inflation. | AMBER (Roland) [no section below] | |

Aberdeen (LON:ABDN) (£2.7bn) | Q1 net outflows £5.2bn. Inflows at interactive investor. Still on track to meet FY 2026 growth targets. | GREEN (Graham) I am AMBER/GREEN on some fund managers now but Aberdeen strikes me as a likely winner in the sector due to its scale, wide-ranging capabilities and also its ownership of a high-quality platform business in the form of interactive investor. | |

Glanbia (LON:GLB) (£2.2bn) | Q1 in line with expectations. Reiterating full year guidance of adjusted EPS of $1.24 - $1.30. | ||

Spectris (LON:SXS) (£1.99bn) | Continue to expect strong growth in adj. profit, in line with exps, while mindful of uncertain macro. | ||

Osb (LON:OSB) (£1.7bn) | Q1 in line, on track for full year guidance of low single digit net loan book growth, NIM c. 225bps. | ||

| Genus (LON:GNS) (£1.1bn) | PRRS Resistant Pig - FDA Approval | SP +24% to 1,970p. US FDA has approved Genus’s PRP gene edit for use in the US food supply chain. This gene edit could mean a substantial reduction in PRRS (a pig disease) and a significant reduction in antibiotic usage | AMBER (Roland) [no section below] This US approval is said to be a major commercial milestone. Genus believes it now needs to secure approvals in key US export markets (Mexico, Canada, Japan) to support successful US commercialisation. Broker Panmure Liberum believes PRP is worth 1,100p per share based on a 2026 launch, but warns it won’t benefit profits until FY27 and leaves current forecasts unchanged. I’m going to leave our neutral view unchanged too, given Genus’s poor historic profitability and P/E of 20+. However, this situation could potentially justify more in-depth research. |

Oakley Capital Investments (LON:OCI) (£799m) | Q1 NAV return per share 2%. NAV per share 707p as of 31st March (before the broad market sell-off). With a current share price of 457p, OCI trades at a discount of 33% to the end-March valuation. A further £30m is now added to OCI’s buyback, on top of a £20m annually recurring buyback that is replacing the dividend. | GREEN (Graham) [no section below] This was mentioned by readers in response to my recent coverage of Pantheon International (LON:PIN) (in which I have a long position). I calculated that PIN was trading at a 44% discount to NAV. OCI is not so cheap in NAV terms but its buyback this year is more impressive as a percentage of its market cap (6%). OCI’s portfolio is valued at c. 16.4x EBITDA, vs. PIN valued at 16.9x, so there is little to choose between them on that metric, and both portfolios have enjoyed strong annual EBITDA growth of 15-20% in recent years. OCI is however much more concentrated with the top ten holdings accounting for 61% of NAV. I’m still happy to give OCI a GREEN on the basis of a long and successful track record. | |

Aston Martin Lagonda Global Holdings (LON:AML) (£655m) | Q1 in line, 2025 guidance unchanged. Positive adj. EBIT (full year) and positive FCF (H2). | ||

PPHE Hotel (LON:PPH) (£556m) | Q1 traditionally quiet. Stable LfL occupancy. Confident full year within range of expectations. | ||

Young & Co's Brewery (LON:YNGA) (£533m) | Full year: LfL sales +5.7%. Total managed revenue +25.4%. Vague “confidence in performance”. | ||

Puretech Health (LON:PRTC) (£302m) | Cash, cash equivalents & short term investments $339m. Operational runway to 2027. | ||

Anglo-Eastern Plantations (LON:AEP) (£301m) | Shares will be suspended due to audit delay. 2024 profit after tax +20% to $67.6m. | ||

LBG Media (LON:LBG) (£188m) | Confident of delivering full-year revenue +10%, as previously indicated. Net cash £32.9m. | ||

SIG (LON:SHI) (£170m) | LFL sales +2%, LFL volumes +3%. UK & DE stronger. FY25 outlook unchanged. | ||

Sylvania Platinum (LON:SLP) (£122m) | Rev +2%, EBITDA -4% to $6.5m. FY25 prod guidance now 78-80koz (prev 75-78koz). | ||

Camellia (LON:CAM) (£117m) | Rev +3%, net loss £4.9m. Net cash £124.7m. 260p dividend. Strategy update May 2025. | ||

Serabi Gold (LON:SRB) (£108m) | Gold production +13% to 37.5koz. Revenue +48%, profit after tax +321% to $35.9m. Net cash of $16.2m. All-in sustaining cost $1,700/oz (2023: $1,635/oz). FY25 production guidance: 44-47koz. New shareholder return policy for 20%-30% of free cash flow. | AMBER/GREEN (Roland) [no section below] | |

| Strix (LON:KETL) (£98m) | Full Year Results | Rev -1.4%, adj PBT -16% to £18.7m, slightly ahead. FY25 exps unch, but flags macro risk. | |

Solid State (LON:SOLI) (£95m) | Trading Update | FY25 rev >£124m and adj PBT £4.25m, ahead of mkt exps. Order book +17%. FY26 exp unch. | |

Trifast (LON:TRI) (£87m) | FY25 rev £223m, adj EBIT in line at £14.8m. Net debt/EBITDA 1.0x. Intend to pass through tariff costs. | ||

Videndum (LON:VID) (£64m) | Rev -8%, adj LBT £(25)m. £8m placing at 85p. Uncertainty re. refinancing. FY25 revenue flat. | ||

Palace Capital (LON:PCA) (£64m) | £35m of sales in FY25. £10m sale in April. £30.9m cash. Reviewing options for final six assets. | ||

IG Design (LON:IGR) (£49m) | FY25 in line with Jan 25 expectations. Rev -9%, adj PBT c.$1m. May exit US market. Outlook unclear. | AMBER/RED (Roland) [no section below] Problems at IG’s US division (FY25 sales -12%) are worsening as customers refuse to accept tariff costs and scale back orders. Mgt are now considering a full exit from the US and warn of “a very material write-down” of this value-destroying 2020 acquisition. The possible saving grace here is that IG ended last year with a net cash position of $84m. Forward guidance has been withdrawn but IG may provide an update on its US plans before its results are published in June. Until then, I see this as a speculative situation, albeit with possible upside if the business can return to its successful pre-US format. | |

Skillcast (LON:SKL) (£34m) | Rev +17%, ARR +25%. Return to profit, EBITDA £0.5m. Net cash £9.1m. YTD trading in line. | ||

Sanderson Design (LON:SDG) (£31m) | Rev -7.6%, adj PBT -64% to £4.4m. Dividend -57%. Net cash £5m. YTD mixed, FY exps unch. | AMBER/GREEN (Roland) Today’s results highlight a sharp fall in sales of the company’s branded goods, plus excess inventories. But the balance sheet remains strong and the stock is trading well below its tangible net asset value. While uncertainty remains over near-term demand and manufacturing profitability, I think the group’s valuable intellectual property is likely to underwrite an eventual recovery. | |

World Chess (LON:CHSS) (£25m) | Rev +4% to €2.4m, pre-tax loss €(3.8m). Net debt €2.4m. Material uncertainty re. refinancing. | ||

Carclo (LON:CAR) (£22m) | FY25 “trading performance” ahead of exps. Improved margins. Net debt £19.3m. Outlook positive. | ||

Zinc Media (LON:ZIN) (£15m) | Rev -4.3%, adj PBT £0.3m (2023: £(0.4m)). Current trading ahead of FY24, FY25 exps unchanged. | ||

Fadel Partners (LON:FADL) (£14m) | Rev -10%, ARR +10% to $9.9m. Adj EBITDA loss reduced to $1.7m. Outlook: cont’d progress. | ||

Huddled (LON:HUD) (£13m) | Rev +110% to £4.4m, 62.7k new customers (+64% YoY). On track for “operational profitability”. | ||

Titon Holdings (LON:TON) (£8m) | Rev -2.3%, op loss reduced to £(162k). Sales performance improving, FY exps unchanged. |

Graham's Section

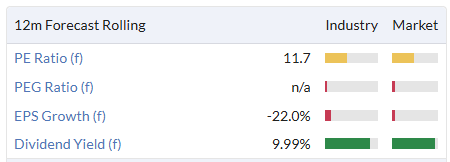

Aberdeen (LON:ABDN)

Up 1% to 148.2p (£2.7bn) - Q1 2025 AUMU and flows update - Graham - GREEN

Let’s briefly check in on this major fund manager, to get a reading on investor sentiment:

Aberdeen Group plc ("Aberdeen" or the "Group") is today providing an update on its Q1 assets under management and administration (AUMA) and net flows.

The headline: AUMA fell by 2% in Q1, or £11bn, to £500bn.

Half of the decline was due to net outflows, with the rest coming from the weakness in financial markets in Q1.

The bright spot, as per usual, is interactive investor which saw net inflows of £1.6bn. Its customer numbers are up 9% year-on-year, with SIPP customers up 29%.

But the story is not so bad at the Investments division, either.

As I noted recently, this division saw net outflows of only around 1% of AUM in 2024.

And while it saw more net outflows in Q1, it is now positive year-to-date thanks to a £6bn mandate win in April, for their quantitative strategies.

So again I wonder if Aberdeen is giving us some clues that investor sentiment is not so bad after all?

CEO comment excerpt:

"Our strategy is to become the UK's leading wealth business and to reposition our Investments business to areas of strength and market growth. So far this year, we have made good progress against these objectives, despite the current heightened levels of market uncertainty.

"interactive investor has seen significant growth in new customers, and in trading volumes, which have risen to record levels during the recent period of market volatility.

Outlook: targeting adj. operating profit of over £300m in 2026. On course to meet target of £150m of annualised cost savings by the end of this year..

Graham’s view

I have moderated my view on most fund managers to AMBER/GREEN, as most of them are suffering very poor momentum in terms of flows, and the competitive environment is extremely difficult. So despite their cheapness, I’m no longer taking an outright bullish stance in every case.

Aberdeen is a case where I think I can stay fully positive, for a few reasons.

Firstly, its scale sets it apart. It’s 10-20x the size of the other fund managers I cover. In plain English, it’s in a different league to the others.

Secondly, the inclusion of interactive investor means that it owns a high-quality platform business in addition to the advisor/investments businesses. These platforms typically trade at higher multiples than fund managers.

Thirdly, the flows at Aberdeen have not been all that bad. It’s almost standing still - which is pretty good.

Finally, the valuation doesn’t put me off:

Stockpoedia categorises it a a “Turnaround” stock (high value and high momentum), which is considered to be a winning style. I think Aberdeen is a winner in the asset management sector - and I’m glad I can call it by that name now, instead of using a strange assortment of letters without enough vowels!

Roland's Section

Sanderson Design (LON:SDG)

Down 6% to 40p (£29m) - Full Year Results - Roland - AMBER/GREEN

Sanderson Design Group PLC (AIM: SDG), the luxury interior furnishings group, announces its audited financial results for the year ended 31 January 2025.

(For the backstory on Sanderson’s rise and fall, check out this recent review by Mark.)

Today’s results are not exactly sparkling, but the question for investors will be whether the value investment case remains intact.

Let’s start with a look at the numbers to understand what happened last year.

FY25 results summary: sales fell sharply last year, driven primarily by a drop in the company’s own branded sales:

Revenue -7.6% to £100.4m

Adjusted pre-tax profit -63.9% to £4.4m

Reported pre-tax loss of £(13.9)m

Dividend -57% to 1.5p per share

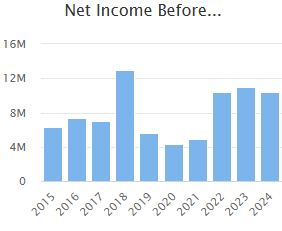

Net cash £5.8m (FY24: £16.3m)

The reported loss is due to the £16.3m goodwill impairment on Clarke & Clarke (acquired 2016):

The valuation of brands across the interior furnishings industry has declined since 2016 and this non-cash impairment of Clarke & Clarke aligns the brand to the current industry environment. The Board remains confident in the future performance of the Clarke & Clarke brand, in its licensing potential and its overall importance to the Group's brand portfolio.

Without this non-cash impairment, the group would have reported a pre-tax profit of £2.4m last year, arguably supporting a view that earnings could be close to a cyclical low:

Trading commentary: while demand slowed for the group’s own brands and manufactured goods, licensing revenue set a new record, helped by deals with Next and J Sainsbury. Licensing carries a near-100% margin and thus this performance effectively protected the business from what would otherwise have been a much deeper loss last year.

Across its business, Sanderson says it’s now focused on a greater shift to digital printing, modernising its factories (with reduced headcount) and capturing the growth opportunity offered by US markets. While tariffs are not expected to have a major direct impact, they are seen as a broader macro risk that could affect demand.

Balance sheet: I calculate NAV of £66.4m or a tangible net asset value of £53.5m. Both are significantly higher than the current £29m market cap.

Happily, Sanderson continues to benefit from a net cash position, albeit reduced significantly last year to £5.8m (FY24: £16.3m).

This £10.5m cash outflow was made worse by adverse working capital movements and a one-off c.£2m pension contribution. However, ultimately this free cash outflow was driven by the loss of profitability caused by lower volumes through Sanderson’s Brand/Manufacturing division (the company’s factories manufacture for its own brands and third parties).

Brands were a particular area of weakness:

With cost cutting and headcount reductions now in force, I’d hope that profitability and cash generation will improve this year.

A reduction in the group’s £27m inventory balance could also release some working capital – management admits that inventories rose last year due to higher volumes and are now “above their optimum level”.

Given that cost of sales were £32m last year, this implies that as much as 10 months’ of stock is being carried. Even after deducting an allowance for raw materials and work in progress, this does look too high to me.

Outlook: the company says that sales have started strongly in the USA this year, with “core brand sales showing double-digit revenue growth” compared to the same period last year.

Sales in the UK and Europe are said to have been in line with expectations during the same period.

However, the announcement of tariffs at the beginning of April has “impacted order intake in all regions”.

My reading of this is that there’s a risk of a further downgrade to expectations at some point.

However, given the uncertainty over the tariff endpoint and impact, I think it’s reasonable for management to have left expectations unchanged at this point:

At this early stage in the current financial year, the Board continues to anticipate that the full year outturn will be in line with its expectations.

Roland’s view:

While there’s clearly some uncertainty about near-term demand, I think that Sanderson’s combination of balance sheet strength and valuable intellectual property assets makes the shares a tempting value play at current levels.

I estimate a tangible net asset value of 77p per share from today’s results. With the stock trading at 39p as I write, I think there should be a reasonable margin of safety from current levels, with decent upside if demand for the company’s own goods does recover.

The main risk I can see is that the manufacturing business will remain a drag on profitability and – potentially – be loss making.

However, on balance Stockopedia’s Contrarian rating seems appropriate to me.

I’m happy to take a moderately positive view, based on today’s results.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.