Correction: This article previously missed a disclosure statement. Roland Head owns shares in Shell.

Anyone who bought big oil stocks in the depths of the 2020 crash has done very well. Shell (LON:SHEL) shares have more than doubled since October 2020. The dividend is also now 50% above the reduced payout announced in 2020.

Shell’s share price recently topped its pre-pandemic level, before slumping as the market started to price in weaker demand for oil.

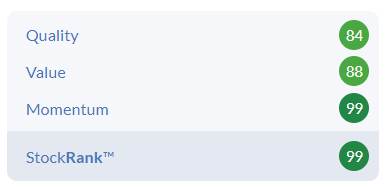

However, Stockopedia’s algorithms are taking a more bullish view. They’ve digested the group’s half-year results and still rate Shell as a Super Stock, with a StockRank of 99.

Shell’s dividend looks rock solid to me and I do not expect another cut. But with profits expected to peak this year, I’m unsure of the case for growth or a further re-rating of the shares.

To find out more, I’ve decided to dig into the story (and the numbers) a little further this week.

Known knowns, unknown unknowns

Early on in my investing career, a much more experienced investor told me to remember that the oil market always overshoots.

We saw this in the early months of the pandemic, when the price of some oil contracts briefly went negative. There was a new groundswell of pressure on fossil fuel producers to clean up their acts. Very little attention was given to the inevitable rebound in energy demand when the pandemic eased.

I wonder if we’re now seeing energy markets overshoot to the upside. Brent Crude recently came close to $140 per barrel, before settling back around the $100 mark.

Source: IG Group

For Shell and its rivals, high oil prices have been a boon. But oil prices are still well above pre-pandemic levels. This seems to assume that demand will be higher than in 2019, or that supply will be more restricted. I’m not sure how strong either argument is.

For example, this recent FT article (paywall) suggests to me that the UK, EU and US may be inclined to continue allowing Russian oil shipments, as long as they are going elsewhere.

Shell’s own Brent crude price assumptions are for $80 for 2023, and $70 for 2024. These numbers would leave oil trading broadly in line with…