Market Musings 25/09/21:

The UK: Contrarian trade of the decade?

Recent podcasts you may care to listen to:

Every Dog has its Day - Eventually

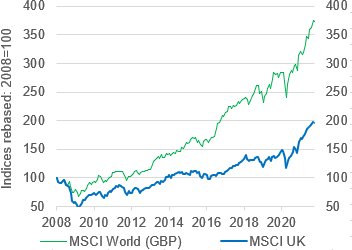

UK stocks have lagged global stock markets since 2008

Source: MSCI, Bloomberg

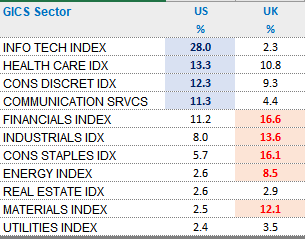

Latterly, the relatively poor performance of UK large-cap stocks in the form of the FTSE 100 index has been put down to a lack of growth stocks in the UK stock market, for instance in the technology sector. This is objectively difficult to argue with, given the massive difference in sector weightings between the two markets.

US stock market heavy in Tech/Communications, Consumer, while UK weighted to Financials, Industrials, Staples, Energy, Materials

Source: Bloomberg

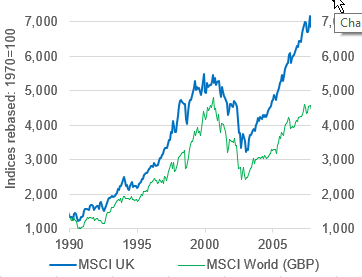

Bear in mind though, that this UK stock market underperformance has not always been the case. It has certainly been the case since 2008, but look at the period between 1990 and 2008! Coming out of the early 1990s recession, UK stocks had two strong runs. - firstly between 1991 and 2000, and then again from 2003 post the TMT bubble and burst up to late 2007.

UK stocks led the World from 1990 to the GFC

Source: MSCI, Bloomberg

Lower commodity prices and interest rates a headwind for the UK

But that does not mean that there is no growth for the stock market investor in the UK. Rather, the nature of this potential growth is simply far more cyclical in nature, depending typically on two key drivers - interest rates and commodity & energy prices.

Financials (Banks and Insurance companies) are sensitive in particular to interest rates and economic growth - the higher economic growth and long-term bond yields are, generally the better for them.

Energy and Materials sectors are evidently sensitive to metals and oil & gas prices, as those prices determine their selling prices and thus their profitability.

Both of these drivers have been trending lower the years since the Great Financial Crisis, as can be seen in the chart below.

Both…