Faced with choosing between a $10 bottle of wine and a $90 bottle of wine, which would you go for? In one experiment - with the prices of each wine clearly marked - nearly twice as many people preferred the taste of the most expensive bottle. But unknown to the volunteers, the two wines were exactly the same.

This test was carried out by American researchers investigating how pricing can influence the brain’s perception of how ‘pleasant’ something is. Told it’s expensive, we tend to like it all the more. It’s an example of what behavioral scientists say is a flaw in human emotions that causes us to be overly-influenced by a good story.

The read across for investors could hardly be more stark. Stories in the stock market are like a magnet. With herds of followers, these popular shares typically boast eye-catching price momentum. Yet a good proportion of them hide deteriorating fundamentals and stretched valuations that can be harder to spot (and, for some, easy to ignore). These are the market’s glamour stocks which may well be Momentum Traps - stocks where a sudden change in sentiment could see their momentum crash.

Of all the dangers that investors face, perhaps none is more seductive than the siren song of stories. Stories essentially govern the way we think. We will abandon evidence in favour of a good story - James Montier

Signs of a Momentum Trap

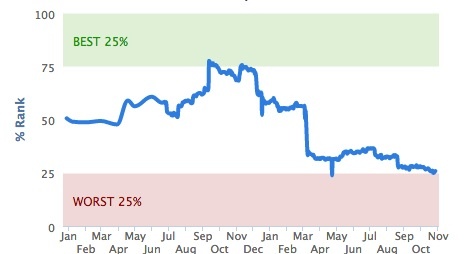

Small cap stocks soared through 2013, and by early the following year some valuations looked frothy. Swept up in a wave of bullish exuberance, popular ‘blue sky’ companies like Blur, Monitise and Cloudbuy were showing some of the classic signs of being momentum traps. As sentiment towards small caps drifted through the next 12 months, the price of each share was pummelled.

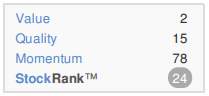

The common traits shared by these and other momentum traps was that their strong price momentum hadn’t been matched by improving fundamentals. Yet they looked expensive and their low QualityRanks pointed to firms that either weren’t profitable at all or were flagging as potentially distressed. Importantly, these were some of the most talked about small caps at the time, promoted by brokers and heavily traded by investors. They were the polar opposite of traditional ‘value’ shares but investors lapped them up all the same.

In The Little Book…