Yesterday's announcement that the $5bn Jarden Corporation was making a bid for ICAP Securities Exchange tiddler Sprue Aegis wouldn't have threatened many headlines, but hidden within this story and the share price breakout are plenty of pearls that investors can learn from.

Sprue Aegis is the kind of company that the City neglects to its regret but that private investors are so able to take advantage of. On average only £15,000 of Sprue's shares have traded each day over the last few months. Clearly institutional fund managers can't trade companies like this without the share price soaring so they tend to completely ignore them unless they can pick up a big line of stock in a placing. It's for this reason that one can so often find hidden gems amongst the smallest companies on the market.

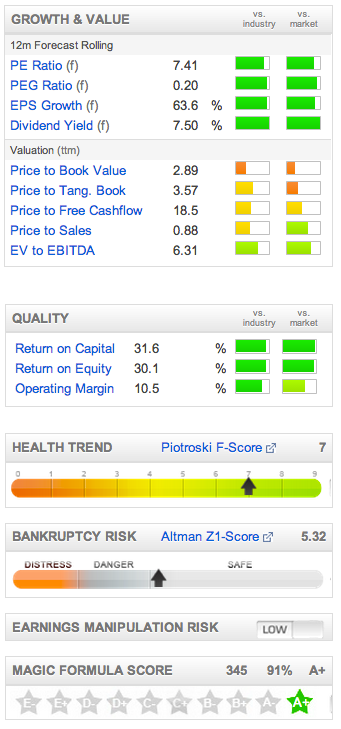

Sprue has certainly been a hidden gem in recent years but what the Jarden Corporation knows that the City doesn't is that Sprue has built up an impressive track record of innovation, execution and excellence in its tiny niche - clearly they think it worth bidding up for.

What's in the silly name?

Sprue Aegis is a fairly young company with a fascinating story beginning in 1998. The founders had decided on their business model before they even decided what products to make. They wished to build plastic electronics devices in a global market without strong brands where the user experience was poor. But it was only when they spotted a broken fire alarm hanging from a ceiling that the proverbial lightbulb switched on.

15 years later and Sprue is the UK market leader in home safety products (smoke and carbon monoxide alarms), with exclusive supplier status to Tesco and B&Q and exclusive rights to distribute many of minority shareholder Jarden Corporations products too. Meanwhile increasing domestic safety legislation across Europe provides a growing market for the company to sell into.

I'm not going to go into the details of the story here as there are some excellent write ups about Sprue Aegis already on the web. Glasshalfull has promoted the investment case extensively on the Motley Fool and on ADVFN, while all credit should go to David Stredder for bringing the company to many private investor's awareness at his Mello meetings.