One of the joys of running my screen-based Stock in Focus fund over the last 3.5 years is that it’s (mostly) forced me to set aside my prejudices and macro views. I’ve repeatedly bought stocks which the discretionary investor in me wouldn’t have bought. Quite often, I’ve been rewarded with a profit.

This week is a good example. Having ditched the defensive safety of supermarket giant Tesco last week, I’m now preparing to consider the attractions of structural steel small cap Severfield (LON: SFR).

I’ve gained a positive impression of this company over the last few years, but from a cyclical viewpoint I don’t see it as an obvious choice at the moment.

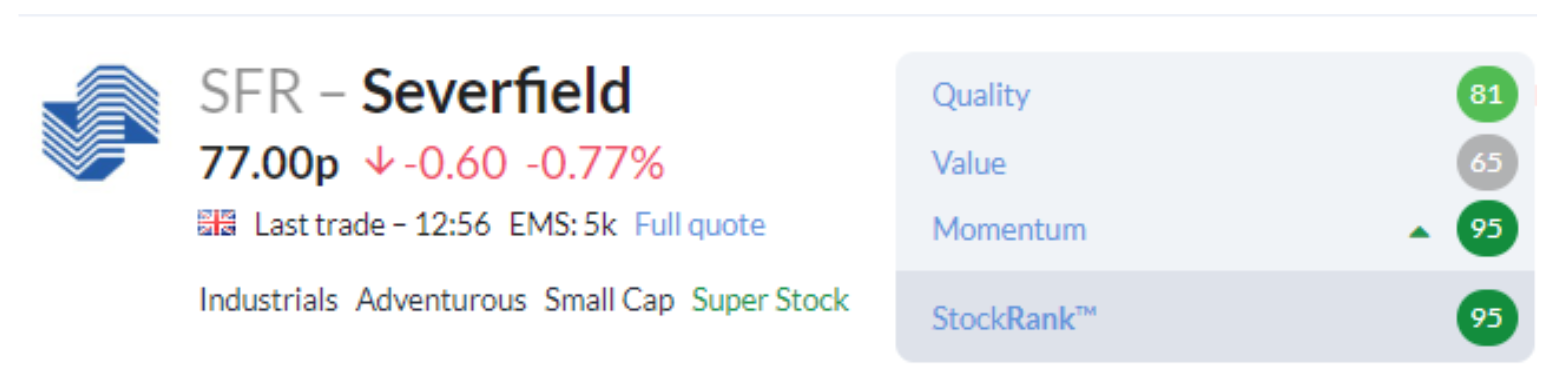

However, this popular stock qualifies for my screen and is potentially eligible for the SIF fund. This week I’m going to take a closer look at this company, which Stockopedia’s algorithms rate very highly:

As usual, I’ll look at Severfield’s quality, value and momentum scores. But first, I think it’s worth taking a look at the firm’s latest trading update. I also want to consider an acquisition which appears to have had a significant impact on broker forecasts.

Trading update warns of H2 weighting

In early September, Severfield issued an AGM trading update confirming that the outlook for the year ending 31 March 2020 remained unchanged. The order book stood at £301m, up slightly from £295m at the start of June.

Management commentary seemed bullish but the update contained one sentence which will strike fear into the hearts of many small cap investors:

“Results for the 2020 financial year are expected to be significantly more second half weighted”

As Paul and Graham often comment, guidance for a second-half weighting is often an early sign that a profit warning is likely.

Checking back to June’s full-year results, I see that the company reported softer UK orders, project delays and difficulties closing sales last year:

The results didn’t mention a second-half weighting, even though September’s trading update claims that this was “as anticipated”.

In the interests of balance, I should point out that there is a plausible explanation for this year’s expected H2 weighting. A recent (paid) broker note on Research Tree notes that an H2 bias to profits is a logical consequence of…

.JPG)