Tharisa was pitched to the Stockopedia Investment Club (SIC) on 7th January 2021.

The Metals & Mining industry has been one of the strongest performers over the past year, rebounding strongly from the March 2020 lows. One particular subset of the mining sector, which has performed exceptionally well is the Platinum Group Metal (PGM) producers. Buoyed by surging demand from the automotive industry, PGM prices have soared.

As a PGM & Chrome producer, Tharisa, has seen plenty of catalysts for a re-rating of its share price as well as its StockRank. Despite the pandemic, the shares are up by over 50% over the last year. This strong momentum, combined with its high quality metrics and attractive valuation now classes Tharisa as an adventurous, small cap, super stock.

Given the strong share price run recent weeks, has the easy money been made or is this the start of a more meaningful commodities rerating?

Summary

Bull Points - Rapidly growing revenues & profits, great exposure to PGMs & Chrome, Rhodium prices currently at $19,000, near-term production expansion, plans for asset & geographical diversification.

Bear Points - Cyclical nature of the industry, Electric Vehicles currently using other metals, South African volatility (currency, politics, Covid restrictions).

Profile

Tharisa (LON:THS), which trades on both the London (AIM) and South African (JSE) exchanges, operates within the Basic Materials sector. The company is a producer of Platinum Group Metal (PGMs) and Chrome concentrates from its mining operations in South Africa.

Tharisa currently trades at a price of 128p per share, giving the company a market capitalisation of £331 million. As a Small Cap, Adventurous, Super Stock, the shares have seen a fair amount of volatility over the past year, despite the impressive performance. An Exchange Market Size of 2,000 means that liquidity may be an issue for larger transactions.

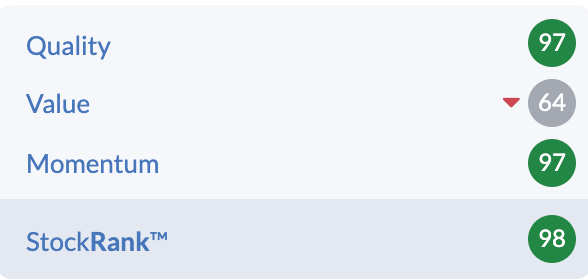

A StockRank of 98 is a testament to the strong all round fundamental characteristics of the company. The Quality and Momentum Ranks both currently stand at 97, whilst the Value Rank has now dropped to 64.

The 12m forecast P/E ranks as one of the lowest in the industry at 5.6 and the forward dividend yield is 3.14%.

Tharisa’s quantitative attributes means that it currently qualifies for 6…