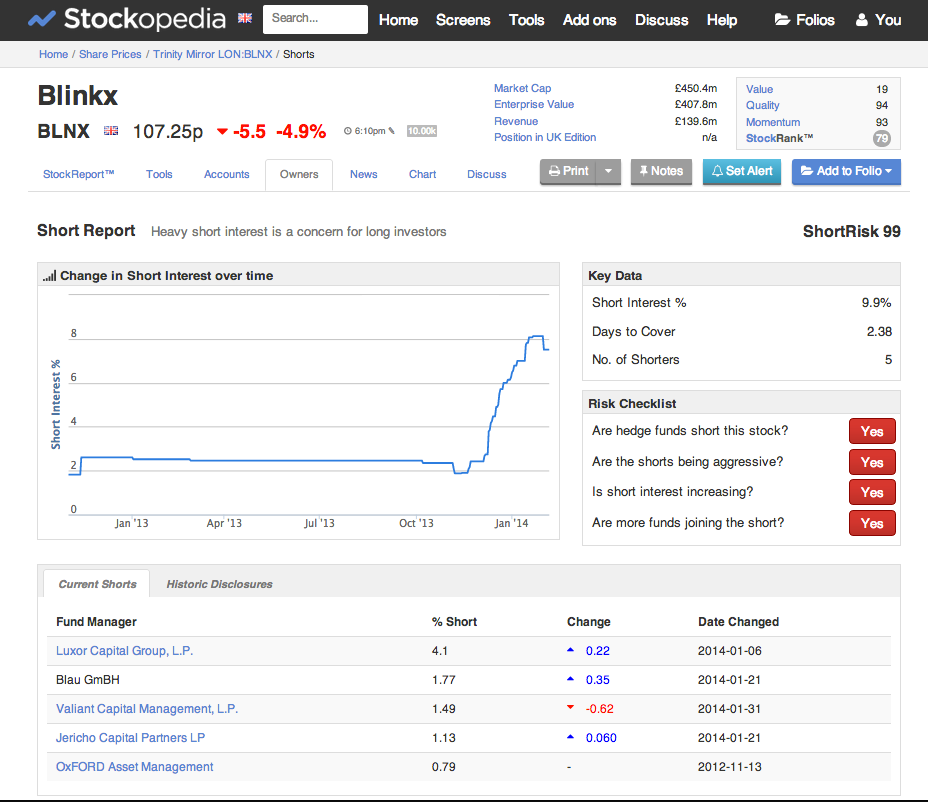

Equity analysts and short sellers are two of the smartest and most informed players in stock market investing yet there’s evidence that they often reach completely different conclusions from the information available to them. Despite broker research being highly sought after by some investors, their buy and sell ratings have been found to be regularly incorrect in shares where short sellers have taken strong opposing views. For regular investors, this can be an opportunity to compare the experts and piggyback the ideas of short sellers to make a profit from trading long or short.

In much of our recent coverage of short selling (here, here and here) we’ve examined how the the level of short interest in a stock marries with other factors such as institutional ownership to influence future price performance. Much of this has shown that short selling can indeed be profitable for the participants and predictive for onlookers. But it’s also fraught with potentially high costs, risks and restrictions that need careful management. By contrast there are far fewer of these pitfalls involved in listening to analyst guidance and going long in stocks, which is one reason why there are vastly more long-only investors than there are short sellers.

Bulls and Bears

Comparing analysts and short sellers is a little like pitching bulls against bears. Research has shown that analysts issue many more positive research notes than they do negative. This is perhaps down to the pressure of maintaining genial relationships with management teams and securing lucrative investment banking work. Meanwhile, short sellers, by their nature, are entirely bearish about the shares they think will fall and scrutinise fundamentals and valuations carefully before placing bets with client money.

Research in 2010 by a team led by US accountancy professor Michael Drake investigated whether the differing opinions of analysts and short sellers could ever predict which way a share price would move. Staggeringly, the results showed that when the two sides were at odds - when a heavily shorted stock was highly rated by analysts or when a share with low short interest received a sell note - the analysts had frequently made the wrong call. The team put this down to earlier findings that analysts often recommend positive momentum, high growth, high volume and relatively expensive “glamour” shares, which often underperform. By comparison, although details of their fundamental analyses…