Don’t be tempted by house builder valuations… yet

Three decades of bumper house price and population growth have made for a comfortable foundation for the UK’s housebuilders and construction companies. Their share price trajectory reflects that.

And in 2020, after the lowest decade of house market growth for 30 years, when everyone thought the fun was coming to an end, government stimulus alongside Covid-fuelled demand for properties with gardens, sent the market soaring again. According to data from Nationwide, the price of the average UK home has risen 26% since the start of the pandemic.

The housebuilders, unsurprisingly, got another boost. These were some of the worst sold-off companies during the March 2020 Covid-19 market crash, but some of the biggest risers in the following months.

But in 2022, their share prices haven’t fared so well. As housing market concerns have ramped up alongside government economic initiatives, their prices have been falling fast.

Safe as houses?

In the last two years the housing market has drifted into bubble territory, inflated by short-term interventions and unusual behaviour. In the final quarter of 2022, house price rises are forecast to rise by 5% year on year.

But that froth is expected to blow out of the market in 2023. In early October Knight Frank revised its forecasts for the next few years, saying that if prices rise 6% in 2022, they will fall by 5% in both 2023 and 2024, breaking the streak in growth which has lasted for 13 years.

This shouldn’t come as a surprise. The housing market has behaved irrationally in the last few years and some of the froth needs to come out of it. It’s the long term outlook that is more concerning.

Housing affordability and the proportion of a buyers’ salaries which are consumed by their mortgage is a key measure of housing market health. In recent years the challenges new buyers face has been in their deposits, rather than the affordability of mortgages. But that is changing. According to Rightmove’s most recent housing market report, average monthly mortgage payments have risen from about £750 in early 2020 to £1100 today, equivalent to 27% of disposable income in 2020 and roughly 32% today. A general rule of thumb is that if monthly mortgage payments are less than a third of disposable income, there is little cause for concern. But based on the mortgage rates being offered today that ratio could rise over 40%. Added to further inflationary pressures on buyers’ disposable income and we could see levels not reached since 2007.

Supply and demand concerns for the housebuilders

So where does that leave the housebuilders?

The sector has slumped to its lowest level in over a decade as increasingly gloomy house price news sends share prices lower. Barratt Developments is among a number of the larger builders to have reported a decline in buyers reserving new homes in the last few months. In a recent trading update, David Thomas, chief executive commented, “private reservations remain below the level seen in FY22 as customers react to the wider economic uncertainty.” Forward sales at the company have dipped in terms of both volume and value.

Greg Fitzgerald, chief executive at Vistry blames the irrational behaviour of the housing market in recent years for the current slump: “Up until April, I think we were operating in an unsustainable market, with house prices rising too fast. Now we’re back to a historical norm.” His company recently announced a cash and share merger with peer Countryside Partnerships in a deal which takes advantage of the recent share price weakness. This time last year Countryside was worth £2.38bn. The deal currently being considered by shareholders values the business at £1.5bn.

The demand shift is not the only concern for housebuilders which are also having to contend with supply constraints and inflationary pressures. In its annual financial results for the year to June 2022, Redrow - which specialises in high quality homes - reported a 10% increase in building costs, driven by inflation and demand for materials.

Should we expect a rebound?

Housebuilders’ inexorable link to the economic cycle tends to put pressure on share prices every time the markets collapse. In the last financial crisis the sector endured a more painful downturn than the wider market and took longer to recover.

But there is no denying that valuations look tempting. Taylor Wimpey shares are trading on a forward price to earnings multiple of less than 5, having been closer to 15 not much more than a year ago.

The trouble is that these P/E ratios currently look so attractive because forecasts haven’t yet priced in current market conditions. In their most recent announcements, most of the housebuilders are acknowledging tricky market conditions without making substantial cuts to their forecasts.

P/E ratios for these companies tend to rise in response to lower expectations, before share price recoveries.

And so it is worth waiting to see where the market settles after the froth has been blown away and expectations are reset before making the move back into the house builders.

About Megan Boxall

Disclaimer - This is not financial advice. Our content is intended to be used and must be used for information and education purposes only. Please read our disclaimer and terms and conditions to understand our obligations.

another important dimension that needs to added in is that a developers net cash flows can substantially rise in a downturn as it is spending less on multi year land banks and construction cost. Add in the substantial net cash position on many developers balance sheets and sustainable high dividends and you get some interesting value opportunities whilst being paid to wait for a return to capital appreciation.

Basically, don't you think GloucesterBob, the lower the share price goes the higher the dividend rises. That is, until something breaks. I hold Barratt Developments (LON:BDEV) , Taylor Wimpey (LON:TW.) and Persimmon (LON:PSN) and have not been topping up while their share prices are in free-fall but am bearing in mind what the boll-weevil song says.

Looking beyond the near future (next year), the foundations for the housebuilders are solid. The desire to own a property is very strong and the imbalance between demand and supply still exists. In the example of Taylor Wimpey, the PE can double to 10 with lower forecasts and it is still a good value. There is no risk of bankruptcy in any housebuilder, they have loads of cash. They can control the market by building less for now and they can sell at higher prices because other vendors refuse to accept the lower prices. There will be a collapse in transactions and the only active market is the new build.

There is no doubt the house prices will drop. it is a reality check which is necessary for a healthy market. Many young buyers love to see lower prices and socially speaking it is a good thing that prices are dropping. I believe, the collapse in housebuilder share prices has factored this in to good extend. Can they drop further? yes but that is you trying timing the market which is difficult.

When I see value I tend to buy , it may drop more and I buy more!

I think price to book, rather than price to earnings, is a better way to value housebuilders. On this measure they look exceptionally cheap, although clearly likely to be very volatile in short term. Trouble is, if you wait till things are all settled down then you risk missing the rebound.

Is the PE ratio even valid for assessing the attractiveness of housebuilders for investment? I was led to believe price to tangible value, or net tangible, was a better measure. Anything over 2 was suggested as poor value and under 1.3 likely to be better value, depending on margins the particular builder was able to achieve.

Some of the smaller builders don't have the scale to achieve the same margins as the likes of Persimmon, others have greater exposure to the unfolding cladding issue, etc. So no hard and fast rules just guides.

Have been tempted by the apparent value in this sector but waiting for an uptick. Not happy to hold much at the moment while the trend is still negative. Next 12 months could be very difficult, so good luck to the brave buyers.

There was a subscriber on this forum a few years ago,whose name I forget, and who suggested that house builders became possible buys once price to tangible book was below 0.8. That now applies to most of them except Persimmon and Berkeley. However in this bear market they may still have further to fall. Who knows! Personally I will wait for the charts to bottom out and the 50 day MA to at least level off before looking to buy even if it means missing a bit of the upside.

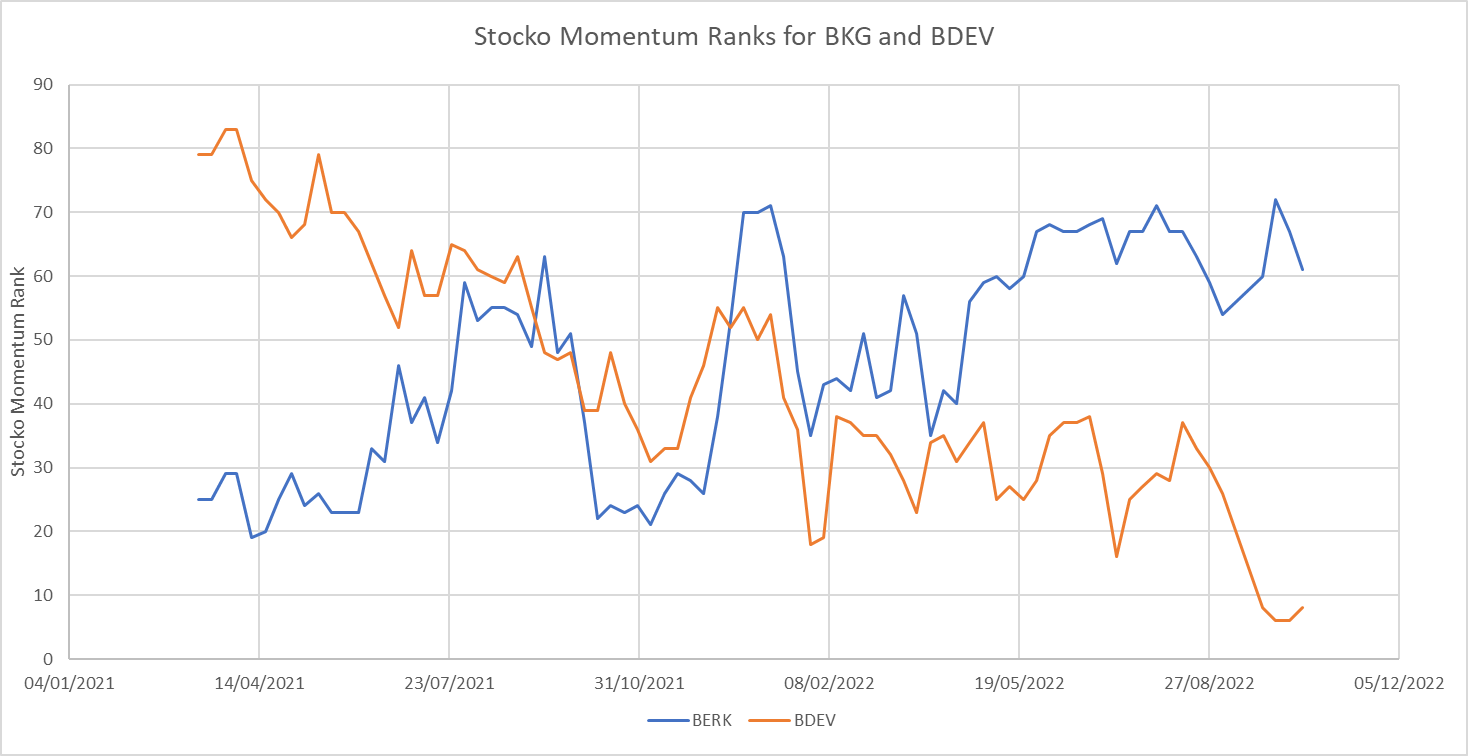

Interesting article. The chart below shows the Stocko Momentum Ranks of Barratt Developments (LON:BDEV) and Berkeley group (BKG) since March last year. There is a striking difference between the two companies but I don't really understand the reason.

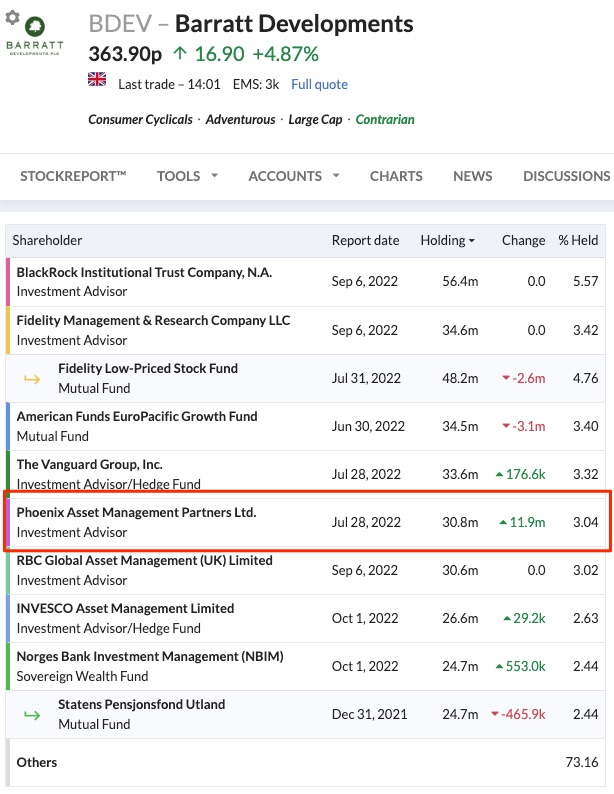

Interestingly Gary Channon at Phoenix Asset Management has recently massively upped his stake in Barratt Developments (LON:BDEV) again. An additional 11.9 million shares bought as of July 28th report date... upping his stake by 63%. The valuation has fallen by an additional 27% since that report.

Gary famously put almost 30% of his fund into BDEV in the GFC... and did tremendously well. I have spent some time with Gary in the past - he's one of the best deep value investors in the UK - he's been a great Stockopedia supporter too so I always track his movements.

I would be wary of the supposed coverage of the dividend for many housebuilders. There is often a big difference between the P/E ratio and the P/FCF which makes wonder if there is the cash being generated to pay the dividend. Redrow seems to be the exception to this.

Thanks for the write-up Megan

I am a holder of both MJ GLEESON (LON:GLE) and Persimmon (LON:PSN) and remain reasonably content to continue holding both.

---

The former - MJ GLEESON (LON:GLE) - offer the cheapest properties of all the listed housebuilders so I think (or rather hope) that they will be relatively well insulated from the short to medium term turmoil.

---

The latter - Persimmon (LON:PSN) - I hold for several reasons.

For 2006-2021 I've compiled a table below showing the company's:

- Gross Profit %;

- ASP (Average Selling Price);

- Volumes Sold,

which I will use to support my rationale for holding.

---

Gross Margins are much stronger today (c30%) vs 15 years ago (c14%)

Additionally, debt was much higher back in the noughties with a huge £76m finance charge paid in 2008 and £55m paid in 2009. The company today has no debt.

That's 2 huge problems the company doesn't have today.

---

Now if history repeats itself in the next 2 years for both volume and ASP i.e. drops of 44% and 15% respectively, then revenue in 2024 should still hit c.£1.6b.

I see this as quite an extreme (and hopefully prudent) scenario.

Apply a very poor PBT% of 20% (the last time it was lower than this was in 2014 - 18.1%) and we are still discussing a company with an operating profit of £327m and free cash generation, using historic assumptions and a 25% corporation tax rate, of c£230m.

---

There is of course a lot of land and cash on the balance sheet too:

a) The current market cap is £4b.

b) I'm personally assuming land on the balance sheet is overvalued by 30% (£2.1b ---> £1.5b), and is worth £1b net of £0.5b of Land Payables.

c) Cash on the balance sheet is currently £780m.

a) + b) + c) gives me an EV of £2.2b.

----

So this is a company that has an EV of £2.2b and in its worst upcoming year will still generate £230m of free cash (a c10% yield) and doesn't appear to have any liquidity issues.

That doesn't sound that bad.

Do I think the share price will fall further? Probably, especially once the current dividend is cut. But in this rapidly changing world, I think I'd rather hold when the valuation seems so cheap and there doesn't appear to be any obvious danger of things falling to zero, or not recovering in good time.

---

On a slightly unrelated note I was amazed to see that ASP CAGR from 2006-2021 was 2.8%, and 3.3% from 2009-2021.

I always think of house prices increasing 5-10% every year for the last 15 years. A 2.8%-3.3% per annum increase in ASP doesn't seem that bad.

Another thing that surprised me was that 16,701 homes were sold in 2006 and this was, and still is, the highest number of sales in a calendar year in the last 15 years.

A lot of housebuilders have been complaining about slow planning approvals. I thought they were simply getting their excuses ready for the inevitable profit warnings, but maybe they have a point?

---

Persimmon (LON:PSN) ONLY

| Gross Profit % | ASP (group average!) | YOY% | CAGR (since 2006) | CAGR (since 2009) | Volume Sold | YOY% | |||

| 2006 | 188,129 | 16,701 | |||||||

| 2007 | 189,558 | 0.8% | 0.76% | 15,905 | (4.8%) | ||||

| 2008 | (24.1%) | 172,994 | (8.7%) | (4.11%) | 10,202 | (35.9%) | |||

| 2009 | 14.0% | 160,513 | (7.2%) | (5.15%) | 8,976 | (12.0%) | |||

| 2010 | 17.5% | 169,339 | 5.5% | (2.60%) | 5.50% | 9,384 | 4.5% | ||

| 2011 | 15.4% | 166,142 | (1.9%) | (2.46%) | 1.74% | 9,360 | (0.3%) | ||

| 2012 | 17.7% | 175,640 | 5.7% | (1.14%) | 3.05% | 9,903 | 5.8% | ||

| 2013 | 20.9% | 180,941 | 3.0% | (0.55%) | 3.04% | 11,528 | 16.4% | ||

| 2014 | 22.2% | 190,533 | 5.3% | 0.16% | 3.49% | 13,509 | 17.2% | ||

| 2015 | 25.4% | 199,127 | 4.5% | 0.63% | 3.66% | 14,572 | 7.9% | ||

| 2016 | 27.8% | 206,765 | 3.8% | 0.95% | 3.68% | 15,171 | 4.1% | ||

| 2017 | 29.8% | 213,321 | 3.2% | 1.15% | 3.62% | 16,043 | 5.7% | ||

| 2018 | 31.6% | 215,563 | 1.1% | 1.14% | 3.33% | 16,449 | 2.5% | ||

| 2019 | 31.0% | 215,709 | 0.1% | 1.06% | 3.00% | 15,855 | (3.6%) | ||

| 2020 | 26.9% | 230,534 | 6.9% | 1.46% | 3.35% | 13,575 | (14.4%) | ||

| 2021 | 30.0% | 237,078 | 2.8% | 1.55% | 3.30% | 14,551 | 7.2% |

Every single response (so far) to this post is that Housebuilders now represent good value and indeed many state they are buyers at current prices. I actually find that quite bearish given the continued weakness in share prices, the economic backdrop and likelyhood that earnings estimates will fall much further as will the headline dividend payments. That appears to be a contrarian view that I share with the author. But in my experience deep value only tends to kick in at extremes.

I've been rather gleefully looking at the value case for these for some time. However, I've yet to purchase. There is a cold winter coming people, energy isn't something one can get more of within 12 months no matter what happens in the market. The UK government has proven itself utterly incompetent to an almost laughable point and it is unlikely that inflation will be solved anytime soon or that the UK Government can avoid raising interest rates. Even if they try to avoid it, it will likely only lead to being forced into raising them even more sharply down the line.

I am not English, but I visit you lot for holidays quite frequently and your AirBnB's are cold. Damn cold. Are any of your damn houses insulated? UK Heating bills are going to be unhinged and someone is going to have to pay market price, be it your government, the consumer or going Dutch.

Now I am absolutely convinced that these house builders are solid and that long term, even at these levels they represent value.

I am however also convinced that the UK is in for it until spring comes back around.

Unless anyone can point me to a company that gets most of its profit from doing insulation work, I'm not loving UK stocks for the moment. Especially home builders. I think we could see more panic before the calm.

Please do let me know if anyone knows of any small caps that work with insulation/heating work on already built property though, they're going to do a booming business among the upper middle class while the poor freeze to death this winter.

*Past performance is no indicator of future performance. Performance returns are based on hypothetical scenarios and do not represent an actual investment.

This site cannot substitute for professional investment advice or independent factual verification. To use Stockopedia, you must accept our Terms of Use, Privacy and Disclaimer & FSG. All services are provided by Stockopedia Ltd, United Kingdom (company number 06367267). For Australian users: Stockopedia Ltd, ABN 39 757 874 670 is a Corporate Authorised Representative of Daylight Financial Group Pty Ltd ABN 77 633 984 773, AFSL 521404.

Ive been tempted for the past year buying every month, and alas I am 30% down, now only buy when the share price drops 10% from my last buy, and there has been a few of those, however the huge divi keeps dragging me in, not mentioned in the article but how safe is that?