This North Sea oil and gas producer currently trades on a forward price-to-earnings ratio of three and boasts a 9% dividend yield. There’s a healthy cash pile as well.

We’ve covered this stock here before, but much has changed over the last 18 months, including the acquisition of Tailwind Energy.

Stockopedia’s algorithms rate Serica Energy (LON:SQZ) as a Super Stock. I think it’s a good time to take a fresh look at this business.

Summary

Pros:

Cash-rich group with low-cost production assets in the UK North Sea

Specialist in operating and improving the performance of ageing fields

Tailwind acquisition has improved asset diversity and resulted in more event split between oil and gas production

Seemingly modest valuation on three times earnings, with 9%+ dividend yield

Experienced management, supportive main shareholder

Cons:

Many of Serica’s assets have limited lifespans

Minimal hedging means a high level of exposure to commodity prices

There’s no guarantee continued reserve replacement will be possible at attractive costs

Risk of Serica ‘diworsifying’ into international operations and losing money

Decommissioning liabilities may be greater than expected

Net cash position may partly reflect the need to provide for future liabilities

Profile

About the stock

Serica Energy is an independent oil and gas producer operating in the North Sea. It operates in the Energy sector and is part of the Oil & Gas industry group.

Serica was founded in 2004 and floated on London’s AIM market in 2005. Today it has a market cap of £850m and a recent share price of 220p.

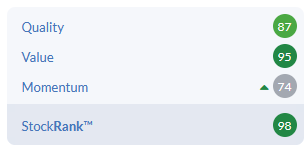

The StockRanks show high quality and value scores for Serica, with improving momentum. This suggests that the business might potentially be in a sweet spot of improving performance and attractive valuation.

About the opportunity

Earlier this year, Serica Energy completed the acquisition of privately owned North Sea firm Tailwind Energy . This resulted in a 75% increase in Serica’s reserves and a significant increase in oil production.

Serica’s production is now split 55%/45% between gas and oil respectively, whereas it was previously 90% gas. In the UK market at least, gas prices tend to be far more volatile…