AdvancedAdvT Limited - Financial Results for year ended 28 February 2026

AdvancedAdvT Limited

Financial Results for year ended 28 February 2026

AdvancedAdvT Limited (LSE: ADVT, "AdvT", the "Group"), the international software solutions provider for the business solutions, compliance, and human capital management sectors, announces its audited results for the twelve months to 28 February 2026.

Financial Highlights

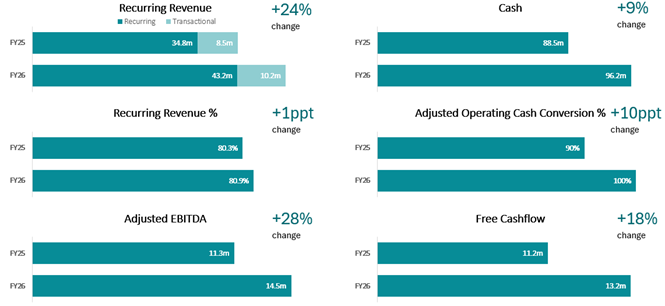

· Revenue increased 23% to £53.4m (2025: £43.3m).

· Recurring revenue grew 24% to £43.2m representing 81% of total revenues (2025: £34.8m and 80%).

· Adjusted EBITDA1 was up 28% to £14.5m, (2025: £11.3m).

· Pre-tax profit before fair value movements on financial assets of £13.4m up 21% (2025: £11.1m).

· Reported basic EPS (impacted by fair value movements): 3.4p (2025: 8.2p). Basic EPS on adjusted operating profit2: 10.5p (2025: 8.5p).

· Cash of £96.2m at 28 February 2026 (29 February 2025: £88.5m).

Operational Highlights

· Acquired HFX Limited ("HFX"): a cloud based workforce management SaaS product, broadening coverage across enterprise and SME customers and supporting migration pathways to cloud adoption in May 2025 for £5.0m net of cash acquired.

· Acquired GOSS Technology Group Limited ("GOSS"): a scalable, low code digital platform enabling public sector organisations to deliver digital transformation and improved citizen engagement platform in May 2025 for £7.4m net of cash acquired.

· Acquired MatchingCore intellectual property for professional services, a leading AI driven resource optimisation capability in December 2025 for £0.5m. This acquisition is intended to accelerate the delivery of advanced AI functionality within the Group's workforce and resource management platforms and to expand addressable market opportunities in professional services use cases.

· Launched a share buyback programme (March 2026), with 4,869,000 Ordinary Shares repurchased and held in treasury as at 24 June 2026.

· Operational improvements: Continued execution of efficiency and performance initiatives across acquired businesses.

· Business Solutions: Deepened engagement in regulated, mission-critical environments, with strong renewals, measured platform modernisation, and improving professional services delivery readiness.

· Human Capital Management: Accelerating SaaS migration and new business, supported by investment in product roadmaps, customer success, and refined go-to-market strategies and operations.

· Market demand / positioning: Digital transformation demand remains structurally positive, especially where customers need trusted systems of record with governance, auditability and control under productivity pressure.

· AI & automation approach: Embedding AI/automation into core workflows to remove friction, automate repetitive tasks, and improve insight while preserving data integrity and regulatory assurance.

· Cloud momentum & product differentiation: Cloud adoption remains in demand (new and existing clients), with recent releases strengthening capability in skills, matching, and multi-department resource planning, reinforcing the need for ongoing innovation and clear roadmaps as expectations evolve (including AI-enabled workflows).

Vin Murria, AdvancedAdvT's Executive Chairperson, said

"The Group has delivered strong progress during the year, with revenue from operations increasing to £53.4m and Adjusted EBITDA rising to £14.5m, ahead of management expectations. This performance reflects continued operational focus, high renewal activity, the expansion of recurring and multi-year revenues, and growing customer demand for dependable software that supports digital transformation in complex and regulated environments. Many of the workflows we support are deterministic, mission-critical systems where accuracy, resilience and control are essential, and where successful modernisation requires deep domain skills, long operating experience and practical understanding of customers' processes. We are investing in AI and automation in a practical and commercially grounded way, embedding capability into trusted systems of record to help customers remove friction, improve productivity, strengthen insight and maintain governance and auditability. We see a significant opportunity ahead as customers continue to modernise critical workflows through SaaS, cloud, AI and automation-enabled solutions. Following the acquisitions of HFX, GOSS and the MatchingCore intellectual property, and with cash of £96.2m at the year end, the Group remains well positioned to pursue disciplined organic investment and selective acquisitions that support long-term growth."

1 Adjusted EBITDA is EBITDA before acquisition expenses and exceptional gains or costs, as defined in Alternative Performance Measures (note 3).

2 Basic EPS on adjusted operating profit is adjusted EBITDA less depreciation, divided by the weighted average number of ordinary shares.

The full final results will be published on the Company's website shortly.

Enquiries:

AdvancedAdvT Limited

Vin Murria, Chairperson

Gavin Hugill, Chief Financial Officer

Singer Capital Markets (Nominated Adviser and Broker) Tel: 020 7496 3000

James Moat / James Fischer

KK Advisory (Investor Relations) Tel: 020 7039 1901

Kam Bansil

Note to Editors

AdvancedAdvT Limited (AdvT) provides software solutions and platforms across two business transformational areas: business solutions & healthcare compliance, and human capital management.

AdvT is an agent for change. The Group enables the delivery of Artificial Intelligence ("AI"), data analytics and business intelligence, all of which are key future drivers for growth in these sectors where long term digitisation trends are set to transform the workplace for professionals.

AdvT is developing both organically and through acquisitions, by expanding its presence across adjacent markets, geographical boundaries and digital sectors.

Chairperson's statement

I am pleased to share that in the year ended 28 February 2026, the Group made excellent progress in executing on its strategy which is centred around backing sectors characterised by long term AI, automation, digital transformation and data analytics and business intelligence trends. Across both operating divisions, management teams remained focused on execution quality, product progression, customer delivery, service reliability and disciplined pipeline conversion, whilst always open to the impact of outside market developments.

In the current market context, investors are rightly focused on the potential impact of AI on software value. No organisation can be immune to disruption risk, however our businesses typically win and retain customers because they embed decades of domain expertise, workflow depth, regulatory understanding and integration into mission‑critical processes. These characteristics create high switching costs and a defensible "system of record" position for many customers, where data governance, trust and auditability are mandatory and where buyers prefer predictable, supportable and compliant solutions.

Importantly, AI is a potential multiplier for solutions like ours. As AI copilots and agents are plugged into trusted systems of record, they can help users complete tasks faster; automate previously uneconomic activities and improve compliance outcomes, without compromising governance or control. In the public sector in particular, adoption is often cautious and policy‑driven, which naturally favours established suppliers with proven resilience, support models and long operating histories in regulated environments.

Across our markets, demand for digital transformation remains structurally underpinned by the need to modernise complex, regulated workflows while maintaining governance, auditability and operational resilience. Our focus is to support through the active use of technology those customers who continue to face sustained productivity pressure, workforce constraints and heightened regulatory scrutiny. We do this by reinforcing the importance of trusted systems of record rather than point solutions.

During the year, we saw this translate into continued engagement across both operating divisions, with strong renewal activity, contract expansions and increasing interest in cloud and automation‑enabled capability. The underlying need to simplify and automate mission‑critical processes has not diminished. In this context, customers are prioritising vendors with demonstrable domain expertise, long operating histories in regulated environments and clear product roadmaps that balance innovation with risk management.

The Board remains confident that these dynamics align well with the Group's portfolio and long‑term strategy, providing a supportive backdrop for disciplined organic development alongside selective, value‑enhancing acquisitions.

Since 2023, the Group has carried out a number of acquisitions, including the original carve-out of 5 entities from Capita plc, which has greatly expanded both our platform and our capabilities.

Upon acquiring each business, we unlock value by focusing on standardising and simplifying processes to adopt best practices and improve go-to-market strategies and operations.

The Group's strategy is centred on the disciplined development of software businesses that operate at the heart of customers' critical processes. Our focus is on retaining and deepening long‑standing customer relationships, supporting measured modernisation through cloud and automation, and selectively extending capability through acquisition where this accelerates delivery or broadens addressable markets.

Organic progress is driven through a combination of high renewal rates, targeted platform enhancements and careful expansion of use cases within existing customer estates, particularly where modernisation and automation can deliver clear operational benefits. This is complemented by a selective M&A approach, targeting businesses with strong recurring revenue characteristics, embedded customer relationships and technologies that can be integrated pragmatically into the Group's operating model.

This balance between organic development and acquisition reflects a long‑term approach to compounding value, prioritising quality of execution, resilience and sustainability over short‑term optimisation.

The management team's experience in software and services, along with their track record in mergers and acquisitions, provides a strong foundation for future expansion.

The Group's performance is measured through a set of core financial metrics, including recurring revenue, adjusted EBITDA, and free cash flow. These indicators serve as benchmarks in gauging our progress, ensuring alignment with our overarching strategic objectives and commitment to delivering sustainable value to our stakeholders.

The Group continues to hold a 9.8% stake in M&C Saatchi plc.

Current trading and outlook

Entering the new financial year, the Group is encouraged by the level and quality of customer engagement across the portfolio. Activity to date reflects ongoing demand for dependable, mission‑critical software that supports automation, insight and governance in complex operating environments.

While macroeconomic and policy uncertainty continues to influence the pace of decision‑making for some customers, particularly in the public sector, management remains focused on execution quality, delivery readiness and disciplined pipeline conversion. Integration of recent acquisitions is progressing as expected, and ongoing investment in product, technology and operational capability is being managed within the Group's established capital allocation framework.

Taking these factors together, the Board remains confident in the Group's ability to deliver sustainable progress, supported by strong cash generation, improving revenue visibility and a balanced approach to organic development and selective acquisition.

Overall, the Group is trading in line with the management's expectations.

Financial highlights

The Group reported revenues from operations of £53.4m in the year under review (2025: £43.3m), with recurring revenue of £43.2m representing 81% of total revenue (2025: £34.8m and 80%). Adjusted EBITDA from continuing operations was £14.5m (2025: £11.3m), which was ahead of management expectations. The Group ended the period with cash of £96.2m (2025: £88.5m).

The Group's operational performance has strengthened materially since admission, underpinned by high renewal rates, targeted platform enhancements, contract expansions and the adoption of best practices that continue to drive operational improvement across the portfolio. Since the platform acquisitions in 2023, this has resulted in revenue increasing from £34.9m to £53.4m for the 12 months to February 2026, alongside an expansion in adjusted EBITDA margin from 16% to 27%, and an increase in recurring revenue as a proportion of total revenue from 75% to 81%, this has resulted in a basic EPS on adjusted operating profit of 10.5p for the 12 months to February 2026 (2025: 8.5p) (see table 1 and note 5).

The Group has continued to implement operational improvements throughout its businesses, boosting performance and long-term potential. The Group has updated its go-to-market strategies to leverage the investments in SaaS and software solutions.

M&A

There was significant M&A activity during the year, including due diligence, successful completion and integration of three acquisitions (two businesses and one intellectual property). Other potential acquisitions advanced but discussions ended due to issues with strategic fit, timing, or value. We continue to evaluate opportunities based on mission-critical software, recurring revenue, strong customer relationships, and clear value creation potential.

In May 2025, the Group completed the acquisitions of GOSS and HFX.

GOSS expands the Group's Business Solutions capability with a scalable, low‑code digital platform enabling public sector organisations to deliver digital transformation and improved citizen engagement and also strengthens integration potential across the Group's enterprise software footprint. Consideration for GOSS comprised approximately £8.5m in cash from existing resources and approximately £5.0m in Ordinary Shares. After accounting for £6.1m of cash acquired, the net consideration was approximately £7.4m.

HFX complements the Group's Human Capital Management offering with a cloud‑based workforce management SaaS product, broadening coverage across enterprise and SME customers and supporting migration pathways to cloud adoption. Total consideration was £5.0m net of cash acquired of £0.6m, of which £2.3m is deferred over two years.

In December 2025, the Group also acquired the MatchingCore intellectual property for professional services, a leading AI‑driven resource optimisation capability. This acquisition is intended to accelerate the delivery of advanced AI functionality within the Group's workforce and resource management platforms and to expand addressable market opportunity in professional services use cases. MatchingCore applies holistic optimisation to workforce scheduling and scenario planning, helping customers improve utilisation, increase productivity and support more informed, data‑driven decision‑making at scale.

With substantial cash reserves (£96.2m as at 28 February 2026), and our investment in M&C Saatchi plc (valued at £15.4m as at 28 February 2026), we remain well-positioned, with significant available capital, to pursue disciplined M&A while retaining flexibility over capital allocation.

Our capital allocation approach continues to balance investment in product, technology and talent with selective acquisitions that extend capability, strengthen integration across the portfolio and enhance the Group's long‑term compounding potential. In addition, we remain focused on delivering value to our shareholders through disciplined capital management, including actions targeting investor returns.

In March 2026, the Board announced the launch of a share buyback programme to purchase up to £10.0m of the Company's Ordinary Shares over a 12‑month period. The Board believes that, at prevailing market prices, a buyback represents an attractive and responsible use of capital alongside continued investment in the portfolio. The programme is being executed by Singer Capital Markets on the Company's behalf, with trading decisions taken independently of the Company. Any shares acquired may be held in treasury (for example, to satisfy future obligations under employee share schemes or as consideration for acquisitions) or may be cancelled. In addition to the Buyback Programme, the Board is considering a further substantial return of capital to Shareholders, potentially by way of a tender offer, but will continue to assess all available capital allocation options, including a tender offer, alongside, or as an alternative to, on‑market buybacks.

As at 24 June 2026, the Company had repurchased 4,869,000 Ordinary Shares under the programme, which are held in treasury, representing an aggregate consideration of approximately £7.8m. The Company's issued share capital remains 137,125,806 Ordinary Shares, with 132,256,806 Ordinary Shares carrying voting rights (being the issued share capital less treasury shares). The programme contains customary price and volume parameters, including that the maximum price paid will not exceed 105% of the average middle market quotation for the five business days preceding a purchase.

M&A continues to be central to the Group's strategy, focusing on businesses that align closely with our management team's vision and demonstrate key characteristics necessary to generate long-term value.

The Board will continue to evaluate each potential target against its acquisition criteria, seeking businesses with:

• high recurring revenue streams and good forward visibility.

• sticky customer retention.

• mission critical products and services.

• opportunities for both organic and inorganic growth.

• strong cash generation.

• sectors with high barriers to entry.

• highly fragmented industries with opportunities for consolidation.

Operational review

Our Business Solutions division continued to deepen customer engagement in regulated and mission‑critical environments, with progress characterised by strong renewal performance, measured platform modernisation and improving delivery execution. In parallel, Human Capital Management continued to balance stability in on-premise customer estates, displaying deep workflow and configuration characteristics, with accelerating SaaS and new technology adoption, supported by investment in product roadmaps, customer success and targeted go‑to‑market refinement.

In Business Solutions, demand for digital transformation remains structurally positive, particularly where customers face sustained productivity pressures and require "trusted" systems of record that support governance, auditability and control. This is especially evident in the public sector, where pockets of momentum are emerging in areas with strong demand for digital services. Nevertheless, progress across the sector is uneven, with delays in decision-making due to ongoing uncertainty around budgets and strategic priorities slowing adoption in other areas. These conditions present both opportunities and challenges, requiring a flexible and responsive approach to engagement and delivery. The Group's approach is to embed AI and automation into core workflows to remove friction, automate repetitive tasks and improve access to insight, while maintaining data integrity and regulatory assurance.

Within Human Capital Management, the Group continued to expand its customer base on cloud platforms, reflecting sustained market demand for modern workforce and resource management solutions. Alongside this migration, we maintained disciplined investment in new functionality and platform capability; focused on scalability, automation, reporting and AI‑enabled planning, while carefully managing investment risk and execution complexity.

Cloud adoption trends within Human Capital Management continue to grow, with both new and existing international clients adopting SaaS platforms to simplify processes and support standardised delivery. Investment in new capabilities and product enhancements have strengthened differentiated capability in areas such as skills, matching and multi‑department resource planning, creating scope for improved customer outcomes and more scalable deployment. The pace of technological change and evolving client expectations, including around AI‑enabled workflows, reinforces the need for ongoing innovation and clear product roadmaps.

The Group considers AI and automation opportunities by weighing potential benefits such as efficiency gains, ease of adoption and value against the scale of change and potential disruption involved, with the aim of delivering practical low risk and measurable outcomes for both the business and its customers. In Business Solutions, AI capability and natural language querying is being embedded directly into core finance workflows and automation libraries to accelerate processing and improve access to insight while preserving governance and auditability. In Human Capital Management, AI‑enabled capabilities are being applied to enhance resource allocation, skills and matching, and advanced planning, supporting improved utilisation and decision‑making for customers. We are also applying AI internally to improve build, test and release processes, supporting higher quality and cadence across product teams.

Across the portfolio, this reinforces the importance of continuing to invest in workflow depth, integration capability and the operational disciplines that underpin customer trust (service reliability, security, data governance and supportability). These are the factors that make replacement risk structurally lower than in less regulated, less embedded software categories, and they also provide a strong foundation on which AI‑enabled automation and premium capability can be adopted over time.

The Group has continued to build its Indian offshore development centre which is now established as an integral part of our product engineering capability. One year on from its original setup, the centre's headcount has grown to 37 colleagues and delivering high-quality enhancements and new capabilities that add incremental value to our existing products, with an original focus across the Human Capital Management portfolio and expanded to the whole portfolio during the year. Importantly, this capability represents a key element of the Group's investment in AI, enabling us to develop and deploy practical, customer-led AI and automation features that improve productivity and outcomes within trusted systems of record.

Importantly, our progress is underpinned by audited outcomes rather than aspiration. The Group has delivered continued EBITDA discipline, strong cash generation and a demonstrable shift in revenue quality toward higher‑visibility recurring income. These themes are reflected consistently through the Consolidated Financial Statements, including the composition of revenue, margin delivery and cash conversion, providing confidence that operational momentum is translating into durable financial performance.

CFO's Report

For the year ended 28 February 2026, the Group generated revenues of £53.4m, compared to £43.3m for the year to 28 February 2025.

Recurring revenues as a proportion of total revenue increased to 81%, up from 80% for the year to 28 February 2025. This performance reflects continued progress in shifting the mix toward higher‑visibility subscription and support income across both operating businesses, supported by disciplined renewal execution, targeted pricing and packaging improvements, and strong conversion of quality pipeline into multi‑year contracts. Notably, GOSS and HFX, both acquired during the year, had previously reported recurring revenues of 71% and 73% respectively, underscoring that the overall improvement in the Group's recurring revenue mix is more significant than the headline figure alone suggests.

The continued shift toward higher‑visibility recurring revenue remains a core feature of the Group's financial performance and is a key focus for management. This reflects disciplined renewal execution, ongoing migration toward subscription and cloud‑based arrangements, and a selective approach to pricing and packaging that aligns value delivered with long‑term customer outcomes.

Beyond reported results, management monitors a range of operational indicators to assess momentum and visibility, including renewal strength, pipeline quality and customer adoption patterns across new and existing platforms. These indicators provide confidence that activity seen during the year is not solely period‑driven but reflects broader engagement with customers as they progress modernisation and automation initiatives within constrained operating environments. While the timing of individual contracts can vary, particularly in regulated sectors, the overall profile of customer demand continues to support sustained progress in revenue quality and cash generation.

This Group's performance is reflected in the composition and quality of the revenues as reported in the notes to the consolidated financial statements. Within Business Solutions, renewed customer confidence translated into both net new wins and deeper engagement from existing customers through extensions, upgrades and adoption of practical AI and automation capabilities. Within Human Capital Management, growth continued to be driven by SaaS adoption and the progressive migration of customers from on‑premise arrangements to cloud subscription models, while maintaining near‑term cash generation and funding product investment.

Alternative performance measures

The Group's approach to AI and automation remains pragmatic and commercially grounded. This year, the Group invested £9.5m in research and development (2025: £6.5m), including capitalised R&D and acquired intellectual property, which represents 17.7% of revenue (2025: 15.1%), underscoring its commitment to advancing embedded technology within core workflows. Investment is directed towards integrating capability directly into established processes where trust, data integrity and regulatory assurance are paramount. This strategy minimises adoption risk, delivers measurable results and aligns closely with customer expectations when introducing AI and automation into mission‑critical environments.

Over time, we expect this to support both improved utilisation of existing platforms and the introduction of premium capability, while preserving the characteristics that underpin customer retention and long contract lifecycles. Importantly, these investments are assessed against clear execution and return thresholds, ensuring that product progression remains closely aligned with operational delivery and financial discipline.

Our cloud strategy continues to gain strong traction across both public and private sector markets. Within Business Solutions, momentum improved over the year as customers renewed, upgraded and adopted new AI-enabled capabilities embedded directly within core systems of record, improving workflow efficiency and access to trustworthy insight while preserving governance, auditability and data integrity. Within Human Capital Management, cloud adoption continued to scale as customers migrated from on-premise to SaaS, supported by ongoing investment in platform performance, automation, reporting and AI-enabled planning and matching capabilities.

From a financial perspective, the Group's exposure to AI‑driven replacement risk is mitigated by the nature of the markets we serve. Many customer deployments sit at the heart of mission‑critical workflows and operate under strict governance requirements, where data integrity, audit trails and predictable support models are non‑negotiable and change programmes are high cost and multi‑year. Over time, we expect AI to expand opportunity rather than compress it, through automation of previously uneconomic tasks, enhanced compliance tooling, premium AI‑enabled features and higher utilisation of existing software footprints as capacity constraints are reduced.

Adjusted EBITDA increased to £14.5m, 27% of revenues, up from £11.3m (26%) in 2025 and £4.4m (21%) in 2024. This improvement has been led by continued enhancements in go-to-market strategies and operations, driving both higher revenue and margins.

Growth in recurring revenue reflects updated pricing models and good customer retention, supported by a continued shift in emphasis towards subscription-based offerings. This approach is enhancing revenue visibility and fostering longer-term customer relationships, consistent with the Group's strategic direction.

During the period, we experienced some customer churn within our mature product lines. However, this was balanced by continued growth in customer acquisition across our SaaS platforms, reflecting the ongoing success of our strategic focus.

Our cloud strategy continued to gain traction. In the public sector, 74% of organisations have adopted our Centros Integra solution. In the private sector, Resource management SaaS platform has delivered 74% year-on-year revenue growth for the 12 months ending 28 February 2026.

The table below reconciles EBITDA to operating profit including one off adjustments and the fair value (loss)/gains.

Table 1:

Audited Period ending

(year ending)

Revenue

53,403

43,274

EBITDA

14,958

10,510

Acquisition expenses, and exceptional (gains)/costs

(477)

838

Loss on disposal

68

-

Adjusted EBITDA

14,549

11,348

Depreciation

(299)

(65)

Adjusted operating profit

14,250

11,283

Amortisation of intangible assets

(4,538)

(3,189)

Loss on disposal

(68)

-

Acquisition expenses, and exceptional (gains)/costs

477

(838)

Operating profit before FVTPL

10,121

7,256

Fair value (loss)/gain on financial assets

(5,640)

180

Operating profit

4,481

7,436

Margin expansion has been supported by operational efficiencies, a balanced revenue mix, and continued investment in technology and process optimisation. The Group has simplified its hosting strategy by transitioning from a mixed private hosting environment to cloud hosting on Microsoft Azure. The investment in this shift enhances security, interoperability and data integration, delivering benefits to both customers and internal operations. These improvements are contributing to more predictable margins and supporting scalable growth.

The Group leverages its existing business software platforms to speed up integration of new acquisitions and ensure consistent operations. Recent updates like a shift to Microsoft Azure tenancy, investment in Azure DevOps, and security protocol standardisation are streamlining processes and improving data governance. These changes and use of group core back-office systems aim to enhance scalability and allow the Group to focus quickly on business development and value creation post-acquisition.

Our continued focus on operational improvements has remained central to progress. By systematically identifying and removing inefficiencies, we have further streamlined operations, delivering ongoing cost savings and supporting improved margins. The rollout and adoption of fit‑for‑purpose systems, frameworks and processes has reinforced these efforts, ensuring that operations remain efficient, scalable and increasingly consistent across the Group.

Table 2:

Free cashflow from continuing activities

Operating profit from continuing activities

4,481

7,436

Fair value on financial assets

5,640

(180)

Amortisation and impairment of intangible assets

4,538

3,189

Depreciation

299

65

Loss on disposal

68

-

Acquisition expenses, exceptional (gains)/costs

(477)

838

Adjusted EBITDA

14,549

11,348

Provision utilisation

(60)

(370)

Decrease/(increase) in working capital

102

(712)

Adjusted operating cashflow

14,591

10,266

Cash Conversion

100%

90%

Capital expenditure

(2,932)

(1,358)

Provision remeasures

(796)

-

Lease payments

(108)

-

Acquisition expenses, exceptional gains/(costs)

477

(838)

Unrealised exchange gains/(losses)

69

(127)

Interest, dividend and warrant proceeds

4,165

3,614

Tax paid

(2,232)

(365)

Free Cashflow

13,234

11,192

Through management of cash reserves, the Group had a net income from financing activities of £4.2m (2025: £3.6m) and profit before tax from continuing operations of £7.7m (2025: £11.3m).

The Group's 9.8% stake in M&C Saatchi plc was valued at £15.4m at 28 February 2026 (28 February 2025: £21.0m), a decrease of £5.6m.

The Group has recognised a deferred tax asset of £0.3m (2025: £1.3m) predominantly in respect of losses expected to be utilised in future periods. The Group has a deferred tax liability of £5.1m (2025: £4.0m) relating to intangible assets recognised on acquisition.

Basic and diluted EPS were 3.4p and 3.4p respectively, reflecting the impact from fair value movements on financial assets (2025: 8.2p and 8.1p). However, Basic EPS on adjusted operating profit was 10.5p (2025: 8.5p - see note 5). The Board is not recommending a dividend at this time. Consistent with our disciplined and responsible approach to capital management, the Board initiated a share buyback programme in March 2026, authorising the purchase of up to £10.0m of Ordinary Shares over a twelve-month period. This mechanism for shareholder returns was selected to ensure efficient allocation of resources while continuing investments in the portfolio, including M&A as well as organic product development. The share buyback reflects the Board's assessment that the current market price does not adequately capture the intrinsic value of the Group's software operations.

Shares repurchased under the programme are held in treasury and therefore reduce the number of shares carrying voting rights, while providing the Company with flexibility to meet future share scheme requirements or, where appropriate, to support transaction consideration. As at 24 June 2026, 4,869,000 Ordinary Shares had been repurchased and held in treasury, representing an aggregate consideration of approximately £7.8m, and resulting in total voting rights of 132,256,806 Ordinary Shares.

The Group's cash position as at 28 February 2026 was £96.2m (29 February 2025: £88.5m), before the net cash outflow of £5.5m related to acquisitions of HFX and GOSS.

Adjusted operating cashflow was £14.6m, representing 100% cash conversion of adjusted EBITDA (28 February 2025: £10.3m and 90%). The Group also capitalised £2.0m of R&D cost (2025: £1.3m).

Free cash flow from continuing activities was £13.2m (28 February 2025: £11.2m). This was impacted by the acquisition of HFX and GOSS in May 2025 with a cash outflow of £5.5m net of cash acquired of £6.7m and the MatchingCore intellectual property acquisition in December 2025 for a further £0.5m.

The Group's cash generation and balance sheet strength remain a key enabler for further organic and inorganic growth. As set out in the consolidated statement of cash flows and supporting notes, profitability continues to convert into cash, supporting ongoing investment, disciplined capital allocation and resilience through the transition to higher proportions of subscription‑based revenue. This strong cash position enabled the Group to invest in new product development, such as the recent acquisition of the MatchingCore intellectual property to accelerate advanced scheduling and scenario planning capabilities within our workforce and resource management platforms. In addition, the Group has pursued targeted acquisitions in key markets, including HFX Limited and GOSS Technology Group Limited, which have expanded our capabilities in Human Capital Management and Business Solutions. Recent investments also include the enhancement of our digital platform capabilities and the strengthening of customer support infrastructure, underscoring our commitment to sustainable growth and service excellence.

Looking ahead, we remain committed to these strategic initiatives, which we believe will continue to drive profitability and support sustainable growth. Our ongoing investments in technology and process optimisation are expected to yield further improvements in operational efficiency and readiness for growth.

Consolidated Statement of Comprehensive Income

28-Feb-2026

28-Feb-2025

£000s

£000s

Revenue

53,403

43,274

Cost of sales

(17,370)

(15,580)

Gross profit

36,033

27,694

Administrative expenses

(21,075)

(17,184)

Depreciation

(299)

(65)

Amortisation

(4,538)

(3,189)

Fair value on financial assets

(5,640)

180

Operating profit

4,481

7,436

Dividend received

234

192

Net finance income

3,131

3,740

Share-based payment expense

(109)

(109)

Profit before tax for continuing operations

7,737

11,259

Taxation

(3,123)

(382)

Profit for the period from continuing operations

4,614

10,877

Total comprehensive profit for the period attributable to owners of the parent

4,614

10,877

Other comprehensive income

Items that may subsequently be reclassified to profit and loss

Translation

69

(127)

Total comprehensive income for the period attributable to owners of the parent

4,683

10,750

Profit per ordinary share (£)

Basic

0.03

0.08

Diluted

0.03

0.08

The Group's activities derive from continuing operations.

Consolidated Statement of Financial Position

£000s

£000s

Non-current assets

Intangible assets

23,829

19,405

Goodwill

36,160

24,715

Property, plant and equipment

939

53

Contract fulfilment assets

110

308

Deferred tax asset

319

1,263

Financial asset at fair value through profit or loss

15,360

21,000

76,717

66,744

Current assets

Inventories

155

108

Trade and other receivables

12,626

12,602

Cash and cash equivalents

96,238

88,510

Total current assets

109,019

101,220

Total assets

185,736

167,964

Equity and liabilities

Sponsor shares

-

-

Ordinary shares

136,866

131,166

Share Premium

98

-

Warrant reserve

-

98

Warrant cancellation reserve

-

350

Share-based payment reserve

691

582

Translation reserve

(53)

(122)

Retained Earnings

14,015

9,051

Total equity

151,617

141,125

Liabilities

Current liabilities

Trade and other payables

7,850

6,130

Corporation taxation

738

727

Contract liabilities

16,713

13,872

Total current liabilities

25,301

20,729

Non-current liabilities

Deferred tax liability

5,086

3,963

Contract liabilities

414

475

Lease liabilities > 1y

161

-

Deferred consideration

1,921

-

Provisions

1,236

1,672

Total non-current liabilities

8,818

6,110

Total equity and liabilities

185,736

167,964

Consolidated Statement of Changes in Equity

Sponsor share

Ordinary shares

Share premium

Warrant reserves

Warrant cancellation reserve

Share based payment reserve

Translation reserve

Accumulated losses/ retained earnings

Total equity

£000s

£000s

£000s

£000s

£000s

£000s

£000s

£000s

£000s

Balance as at

29 February 2024

-

131,166

-

98

350

473

5

(1,826)

130,266

Total comprehensive profit for the period

-

-

-

-

-

-

-

10,877

10,877

Share-based payment expense

-

-

-

-

-

109

-

-

109

Translation

-

-

-

-

-

-

(127)

-

(127)

Balance as at

28 February 2025

-

131,166

-

98

350

582

(122)

9,051

141,125

Total comprehensive profit for the period

-

-

-

-

-

-

-

4,614

4,614

Issuance of Ordinary shares for acquisition

-

5,000

-

-

-

-

-

-

5,000

Issuance of Ordinary shares for warrants

700

98

(98)

-

-

-

-

700

Share-based payment expense

-

-

-

-

-

109

-

-

109

Translation

-

-

-

-

-

-

69

-

69

Reclassification of warrant cancellation reserve to retained earnings

-

-

-

-

(350)

-

-

350

-

Balance as at

28 February 2026

-

136,866

98

-

-

691

(53)

14,015

151,617

Consolidated Statement of Cash Flow

Year ended

Year ended

28-Feb-2026

28-Feb-2025

£000s

£000s

Cashflow from operating activities

Profit before taxation for the period

7,737

11,259

Adjustments for:

Depreciation

299

65

Amortisation

4,538

3,189

Loss on disposal

68

-

Net interest received

(3,131)

(3,740)

Fair value (gains)/losses on financial assets

5,640

(180)

Add back share-based payment expense

109

109

Provision release

(856)

(370)

Dividend income

(234)

(192)

Working capital adjustments:

(Increase)/decrease in trade and other receivables and prepayments

1,218

(4,336)

Decrease in contractual fulfilment assets

198

467

Increase/(decrease) in trade and other payables

(575)

675

Increase/(decrease) in contractual liabilities

(739)

2,482

Tax paid

(2,232)

(365)

Net cash flow from operating activities

12,040

9,063

Cash flow used in investing activities

Purchase of property, plant and equipment

(451)

(38)

Development of intangible assets

(1,981)

(1,320)

Purchase of intangible assets

(500)

-

Acquisition of subsidiaries, net of cash acquired

(5,506)

(4,793)

Lease payments

(108)

-

Net cash flow used in investing activities

(8,546)

(6,151)

Financing activities

Dividend income

234

192

Warrant exercise

700

-

Net Interest received

3,231

3,422

Net cash flows from financing activities

4,165

3,614

Net increase in cash and cash equivalents

7,659

6,526

Net foreign exchange differences

69

(127)

Cash and cash equivalents at the beginning of the period

88,510

82,111

Cash and cash equivalents at the end of the period

96,238

88,510

Notes to the Consolidated Financial Statements

1. GENERAL INFORMATION

AdvancedAdvT Limited ("Company") was incorporated on 31 July 2020 in the British Virgin Islands ("BVI") as a BVI business company (registered number 2040954) under the BVI Business Company Act, 2004 and has its registered address at Commerce House, Wickhams Cay 1, Road Town, Tortola, British Virgin Islands VG1110 and UK establishment at 11 Buckingham Street, London WC2N 6DF. The Company has one direct subsidiary, MAC I (BVI) Limited and a number of indirectly held subsidiaries (together with the Company the "Group").

The Group provides software solutions and platforms across two business transformational areas: business solutions & healthcare compliance, and human capital management. The Group's operations are Integra (financial management software), CHKS (AI based healthcare intelligence compliance and accreditation software), inSTREAM (intelligent process automation software), GOSS (low code digital platform), Retain (global resource planning and talent management software). WFM (workforce management software provider) and HFX (cloud-based workforce management SaaS product). The Company is an agent for change, enabling the delivery of Artificial Intelligence ("AI"), data analytics and business intelligence, all of which are key future drivers for growth in these sectors where long term digitisation trends are set to transform the workplace for professionals.

The Group is developing both organically and through acquisitions, by expanding its presence across adjacent markets, geographical boundaries, and digital sectors.

The Company was listed on the Main Market of the London Stock Exchange from 4 December 2020, the Acquisitions constituted a reverse takeover, and shares were therefore suspended from 8 June 2023, the Company was subsequently admitted to AIM from 10 January 2024.

Certain items in the Consolidated Statement of Comprehensive income have been reclassified for presentational purposes, the effect of which is immaterial.

2. CRITICAL ACCOUNTING JUDGEMENTS AND ESTIMATES

The preparation of the Consolidated Financial Statements under IFRS requires the Directors to make estimates and assumptions that affect the reported amounts of assets and liabilities and the disclosure of contingent assets and liabilities including those that would result in a material adjustment to carrying amounts within the next financial year. Estimates and judgements are continually evaluated and are based on historical experience and other factors including expectations of future events that are believed to be reasonable under the circumstances. Actual results may differ from these estimates.

Key sources of estimation uncertainty

Identifiable assets acquired and liabilities assumed

As required by IFRS 3, we have measured the assets acquired and liabilities assumed on the acquisitions in the period at their fair value on acquisition. The fair values of contract liabilities at acquisition dates were estimated to obtain a price that would be paid to transfer the liability in an orderly transaction between market participants. The approach used was based on a market participant's estimate of the costs that will be incurred to fulfil the obligation plus a normal profit margin, based on the overall cost profile over the life of the contract.

The determination of the fair value of assets and liabilities including goodwill arising on the acquisition of businesses, the acquisition of branding, customer relationships and intellectual property, whether arising from separate purchases or from the acquisition as part of business combinations, and development expenditure, which is expected to generate future economic benefits, are based, to a considerable extent, on management's estimations. Independent specialists were engaged to review the assessment.

The fair value of these assets is determined by discounting estimated future net cash flows the asset is expected to generate where no active market for the assets exists. The use of different assumptions for the expectations of future cash flows and the discount rate would change the valuation of the intangible assets

Goodwill impairment

Goodwill is not considered impaired based on cash flow projections.

Critical accounting judgements

Revenue Recognition

There are a number of areas where judgement has been applied in respect of revenue recognition. In applying IFRS 15, Revenue from Contracts with Customers, significant judgement which may affect the determination of the amount and timing of revenue from contracts with customer includes: assessment of the costs the Group incurs to deliver the contractual commitments and whether such costs should be expensed as incurred or capitalised.

Recovery of deferred tax assets

Deferred tax assets are recognised for deductible temporary differences only if the consolidated entity considers it is probable that future taxable amounts will be available to utilise those temporary differences and losses.

Provisions

Onerous contract provisions are recognised where the unavoidable costs under a contract reflect the least net cost of exiting from the contract, which is the lower of the cost of fulfilling it and any compensation or penalties arising from failure to fulfil it.

For the year to 28 February 2026, the Directors do not consider that they have made any other significant estimates, judgements or assumptions which would materially affect the balances and results reported in these Consolidated Financial Statements or in the next period.

3. ALTERNATIVE PERFORMANCE MEASURES

In reporting financial information, the Group presents alternative performance measures ("APMs") which are not defined or specified under the requirements of IFRS. The Group believes that these APMs, which are not considered to be a substitute for IFRS measures, provide stakeholders with additional useful information on the underlying trends, performance and position of the Group and are consistent with how business performance is measured internally. The alternative performance measures are not defined by IFRS and therefore may not be directly comparable with other companies' alternative performance measures. The key APMs that the Group uses are outlined below.

Closest equivalent IFRS measure

Reconciling items to IFRS measure

Definition and purpose

Income Statement Measures

Adjusted EBITDA or Profit before tax (PBT)

Operating profit or Profit before tax

Adjusting items

Adjusted operating profit/profit before tax excludes adjusting items.

Adjusting items

None

Refer to definition

Items which are not considered part of the normal operating costs of the business, are separately disclosed because of their size, nature or incidence are treated as adjusting. The Group believes the separate disclosure of these items provides additional useful information to users of the Consolidated Financial Statements to enable a better understanding of the Group's underlying financial performance. These may include the financial effect of adjusting items such as, inter alia, restructuring costs, impairment charges, amortisation of intangibles, costs relating to business combinations, one-off foreign exchange gains or losses, integration costs, acquisition-related expenses, share-based payment charges, contingent consideration and earn-outs, cloud computing configuration and customisation costs, and right-of-use asset disposal gains or losses.

Recurring revenue

Revenue

See note 4

Recurring revenues are income occurring continuously and repeatedly.

Transactional revenue

Revenue

See note 4

Transactional revenue is recognised at the point of transfer (delivery) to a customer.

Balance Sheet Measures

Net cash or debt

None

Net cash debt is defined as cash and cash equivalents and short-term deposits, less bank overdrafts and other current and non-current borrowings.

Cash Flow Measures

Cash conversion

None

Refer to definition

Adjusted operating cash flow as a percentage of adjusted EBITDA.

Free cash flow

None

Refer to definition

Cash flow in the period after accounting for operating activities, investing activities, lease payments, interest and tax.

4. SEGMENT INFORMATION

Revenue from continuing operations

Year ended

Year ended

28-Feb-2026

28-Feb-2025

£000s

£000s

Recurring revenues

43,195

34,768

Transactional revenues

10,208

8,506

53,403

43,274

Revenue is recognised for each category as follows:

• Recurring revenues: income occurring continuously and repeatedly; and

• Transactional revenues: recognised at the point of transfer (delivery) to a customer.

Operating segments

IFRS 8 requires operating segments to be identified on the basis of internal reports about components of the Group that are regularly reviewed by the chief operating decision makers to allocate resources to the segments and to assess their performance.

The chief operating decision makers have been identified as the Executive Directors. The Group revenue is derived from the sale and subscription of recurring and transactional revenue engagements with its customers. Consequently, the Executive Directors review the two revenue streams, but as the costs are not recorded in the same way, the information on costs is presented as one segment and as such the information included below is presented in line with management information.

Year ended

Year ended

28-Feb-2026

28-Feb-2025

£000s

£000s

Revenue

53,403

43,274

EBITDA

14,958

10,510

Acquisition expenses, stamp duties and relisting expenses

(477)

838

Loss on disposal

68

-

Adjusted EBITDA

14,549

11,348

Depreciation

(299)

(65)

Adjusted operating profit

14,250

11,283

Amortisation of intangible assets

(4,538)

(3,189)

Loss on disposal

(68)

-

Acquisition costs and exceptional gain on provision release

477

(838)

Operating profit before FVTPL

10,121

7,256

Fair value (loss)/gain on financial assets

(5,640)

180

Operating profit

4,481

7,436

5. EARNINGS PER ORDINARY SHARE

Basic EPS is calculated by dividing the profit/(loss) attributable to equity holders of a company by the weighted average number of ordinary shares in issue during the year. Diluted EPS is calculated by adjusting the weighted average number of ordinary shares outstanding to assume conversion of all potentially dilutive instruments into ordinary shares.

On 4 December 2020, the Company issued 700,000 ordinary shares and 700,000 matching warrants. All 700,000 warrants were exercised for cash at £1 per share, resulting in the issue of 700,000 new ordinary shares becoming effective on 9 December 2025 and are included in the calculation of earnings per share (EPS). Following this exercise, there are no warrants outstanding at the reporting date.

3,225,806 new ordinary shares were issued during the year in connection with the acquisition of GOSS. These shares became effective on 2 June 2025 and are included in the calculation of earnings per share (EPS).

As more fully detailed in the Audited Financial Statements incentive shares in MAC I (BVI) Limited have been issued. On exercise, the value of these shares is expected to be delivered by the Company issuing new ordinary shares, and hence the Incentive Shares could have a dilutive effect, although the Company has the right at all times to settle such value in cash. Although the Preferred Return is currently being met, the Incentive Shares remain outside the exercising period and therefore cannot be redeemed. As a result, they have not been included in the calculation of diluted EPS.

The Company has issued two sponsor shares, the sponsor shares have no right to receive distributions and so have been ignored for the purposes of IAS 33.

Year ended

Year ended

28-Feb-2026

28-Feb-2025

Basic

Profit attributable to owners of the parent (£000s)

4,614

10,877

Weighted average number of ordinary shares in issue

135,761,149

133,200,000

Basic profit per ordinary share (pence)

3.40

8.17

Diluted

Profit attributable to owners of the parent (£000s)

4,614

10,877

Weighted average shares in issue

135,761,149

133,200,000

Adjustment to number of shares for warrants

-

700,000

Adjusted weighted average shares in issue

135,761,149

133,900,000

Diluted profit per ordinary share (pence)

3.40

8.12

Basic EPS on adjusted operating profit

Adjusted operating profit

14,250

11,283

Weighted average number of ordinary shares in issue

135,761,149

133,200,000

Basic EPS on adjusted operating profit per ordinary share (pence)

10.50

8.47

This information is provided by RNS, the news service of the London Stock Exchange. RNS is approved by the Financial Conduct Authority to act as a Primary Information Provider in the United Kingdom. Terms and conditions relating to the use and distribution of this information may apply. For further information, please contact rns@lseg.com or visit www.rns.com.

RNS may use your IP address to confirm compliance with the terms and conditions, to analyse how you engage with the information contained in this communication, and to share such analysis on an anonymised basis with others as part of our commercial services. For further information about how RNS and the London Stock Exchange use the personal data you provide us, please see our Privacy Policy.ENDFR EAEKPALXKEAA

Recent news on AdvancedAdvT

See all newsBrief: AdvancedAdvT Posts FY2026 Pre-Tax Profit Before Fair Value Movements £13.4 Mln, Up 21%

AdvancedAdvT Limited - Financial Results for year ended 28 February 2026

AdvancedAdvT Limited - Holding(s) in Company

No intention to make an offer for M&C Saatchi plc

Brief: AdvancedAdvT Launches Share Buyback Programme To Purchase Up To £10 Million Ordinary Shares