Sucker Stocks: Why do we love to own the worst prospects in the market?

In the aftermath of England’s early exit from the 2015 Rugby World Cup came an intriguing but sadly familiar tale of misadventure in the stock market. During the tournament preparations it was alleged that the team’s kit manager shared a tip about the ‘exciting prospects’ of a micro-cap oil exploration company. This apparently lulled some players into parting with tens of thousands of pounds for the stock. Like the team’s on-field performance, there were high hopes for shares in LGO Energy, but the hype failed to live up to expectations.

This was a classic case of story over substance tempting investors into a stock where the statistical likelihood of a good result was low. The share wasn’t obviously cheap, it had low quality characteristics and its momentum was declining. But it did have vocal supporters who were prepared to talk-up its prospects to anyone that would listen. In the Stockopedia taxonomy of stock market winners, we classify these shares as Sucker Stocks.

The traits of a Sucker Stock

Sucker Stocks have very little exposure to the Quality, Value and Momentum factors that have historically generated the strongest returns in the stock market. Typically they have blue sky business models or operate in highly speculative sectors that may be experiencing cyclical downturns.

Occasionally, they will be broken firms that have lost the confidence of most of the market. But unlike Value Traps, the appeal of their story to some investors often means that these low quality, low momentum shares remain over-priced.

Moreover, these stocks are often small and attract scant coverage from analysts. That means their poor quality and stretched valuations may not be obvious to gullible investors. It makes them particularly vulnerable to the kind of rumour and conjecture that is rife on internet bulletin boards. All these factors can easily suck in the unwary.

Robert Haugen’s “stupid stocks”

The profile of these shares is well known in academic finance. Some of the best analysis was done by Robert Haugen, the groundbreaking financial academic who sadly passed away recently. In his wonderful book, The Inefficient Stock Market[1], he referred to them as Stupid Stocks.

Haugen’s research into long term expected returns found that the best performing shares had the characteristics of what many would recognise as GARP stocks - or Growth at a Reasonable Price. These were low priced, low volatility shares with a strong growth profile.

By contrast, the shares that delivered the lowest returns were generally exposed to a heap of negative factors (although not all at the same time). Haugen defined the ultimate Stupid Stock as:

Relatively small, and illiquid, risky, financially shaky, negative momentum, unprofitable now and getting worse, yet selling at high prices relative to current sales, cash flow, and earnings

The strong link between poor returns and the sorts of negative factors Haugen highlighted has led some to use them for short selling strategies. James Montier, during his stint as Global Strategist at Societe Generale, wrote extensively about the tendency for expensive, deteriorating, poor quality stocks to systematically underperform.

To prove the point, he created an ‘Unholy Trinity’ strategy. It deliberately looks for stocks with a high price-to-sales ratio (ie. expensive), a low Piotroski F-Score to isolate deteriorating fundamental health, and high total asset growth as a signal of poor capital discipline. Between 1985 and 2007 a portfolio of such European shares rebalanced annually would have declined over 6% per year against a market that was rising 13% per year over the same period. Stockopedia’s tracking of the Unholy Trinity strategy has also seen very poor performance (as it should). You can see the performance here.

Red flags - expensive, poor and deteriorating

These negative characteristics echo the profile of stocks that score badly against Stockopedia’s ranking of Quality, Value and Momentum (QVM). Specifically, shares with low StockRanks will be afflicted by a combination of:

Expensive valuation: In the absence of earnings, valuations may have to rely on ratios like Price to Sales and Price to Book, which can quickly highlight shares on overstretched ratings.

Financial weakness & low earnings quality: As these shares tend to be blue-sky, or pre-revenue ventures they will likely have negative profitability (e.g. a negative Return on Capital Employed), poor or non-existent free cashflow and have a history of diluting shareholders through consistent secondary share issues. They may also flag for potential earnings or bankruptcy risk, as measured by the Beneish M-Score or Altman Z-Score.

Poor price momentum and broker downgrades: Share prices of Sucker Stocks will likely have been weak against the market. Brokers may have revised down their forecasts, or the firm may have missed earnings expectations.

Why people love sucker stocks

What normally happens when we publish lists of ‘sucker stocks’ is that defensive shareholders come out in waves to unleash a torrent of reasons why their favoured stock shouldn’t be in the list. Some of the usual suspect reasons are:

Valuing the company on historic measures is not relevant as the reality is all about the future.

The technology once fully commercialised will ‘revolutionise’ an industry or the world.

There is some upcoming ‘transformative’ event that must be taken into account (like a drilling result or an FDA report).

Our numbers are just plain wrong.

Nearly every sucker stock always has a strong story behind it that will (apparently) lead it to redemption. But we humans are blinded by the allure of a good story. The facts are plain. Just as with lottery tickets, some sucker stocks may do well but, if past trends persist, the majority are likely to underperform. We can almost guarantee that every investor holding one of the above stocks will believe that their stock is ‘the one’ which will outperform. But everyone can’t be right.

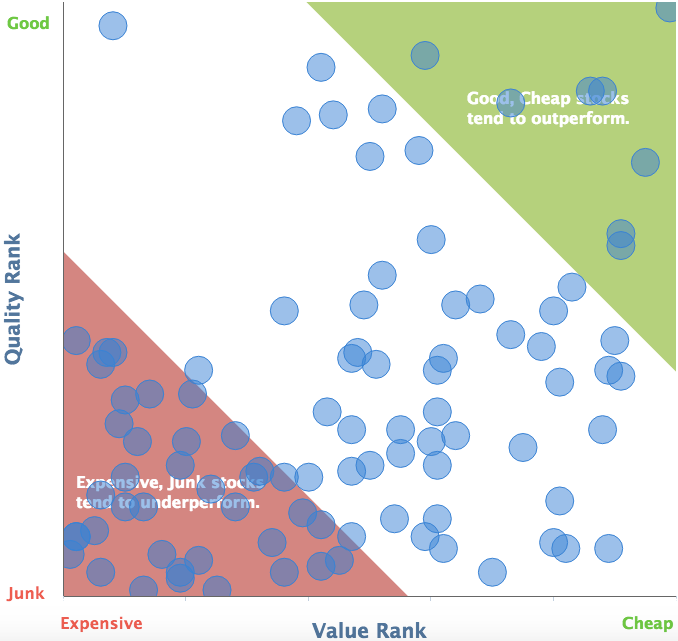

The really sad truth is that individual investors just love loading up on these losing plays. If we look at the most discussed shares on UK bulletin boards and put them into the Stockopedia Bubble Charts it’s obvious that there are far more sucker stocks (bottom left) heavily discussed than super stocks (upper right). Perhaps we should learn from Odysseus and block our ears with wax so we don’t succumb to the siren song of story stocks.

Lessons from Sucker Stocks

The major lesson here is that shares which rank badly for their Quality, Value and Momentum should immediately raise red flags in the minds of investors and require very detailed research.

Warren Buffett once remarked in a letter to shareholders of Berkshire Hathaway:

If you aren't certain that you understand and can value your business far better than Mr. Market, you don't belong in the game. As they say in poker, ‘If you've been in the game 30 minutes and you don't know who the patsy is, you're the patsy’.

To varying degrees, portfolios are dragged down by exposure to shares that are overvalued, poor quality and on a deteriorating trend. Yet, for various psychological reasons, this class of share still holds great appeal. And while there may be individual cases of remarkable recovery, evidence suggests that the odds are stacked against it. So when constructing a portfolio it’s best to keep to an absolute minimum the number of sucker stocks held.

For investors and rugby players alike… it’s worth treating tips and bulletin board hype with great caution. The prospect of quick riches from speculative story stocks is likely to end in tears… or at least an early bath.