Good morning! I hope you had a restful weekend.

11.45am: we are all done for now! Cheers.

Spreadsheet accompanying this report (updated to 3/1/2025).

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Entain (LON:ENT) (£4.0bn) | Reiteration of FY24 guidance. | Group EBITDA at the top of the £1,040-1090m guidance range (previously: “towards the top”). | |

Plus500 (LON:PLUS) (£1.95bn) | Year End TU | Rev $768m, meaningfully ahead of market expectations. EBITDA $342m. Confident outlook. | GREEN (Graham) |

Oxford Nanopore Technologies (LON:ONT) (£1.27bn) | Full Year TU | In line. H1 revenue grows 1% (to $100m+), adj. EBITDA c. $30.3m. | |

Pagegroup (LON:PAGE) (£1.0bn) | Q4 2024 TU | 2024 operating profit towards lower end of range (£49-58.5m). Ongoing challenging conditions. | |

Craneware (LON:CRW) (£728m) | H1 FY25 TU | H1 revenue growth >10% to exceed $100m. Full year in line with exps, confident outlook. | |

Polar Capital Holdings (LON:POLR) (£488m) | AuM Update | Net inflows & positive market perf. AuM up 9% to £23.8bn at 31 Dec. | GREEN (Graham) |

Science (LON:SAG) (£203m) | FY24 TU & 2025 Buyback | 2024 record adj op profit “in line or slightly ahead” of exps. | |

Filtronic (LON:FTC) (£198m) | Trading ahead of expectations | Ahead of expectations. Order intake for the current year is higher than anticipated. | AMBER (Roland) |

| Macfarlane (LON:MACF) (£170m) | Acquisition of the Pitreavie Group | £18m price including £4m earn-out, all-cash. Funded by MACF’s existing bank facility. | GREEN (Graham) |

Eagle Eye Solutions (LON:EYE) (£139m) | H1 FY25 TU & Multi-Year Global OEM Agreement | Revenue warning. FY25 and FY26 revenue to be 15% and 18% below exps. Higher EBITDA margins mitigate impact. | AMBER (Roland) |

Quartix Technologies (LON:QTX) (£76m) | TU | FY24 rev £32.4m, PBT £6.0m. FY25 slightly ahead of expectations. | |

Hercules Site Services (LON:HERC) (£35m) | Final Results | “Ahead of expectations”, continuing rev +28%, adj PBT +43%. Positive outlook. | |

Sosandar (LON:SOS) (£16m) | TU & New Store Agreements | In line with expectations of £40.5m revenue and £1m PBT. Two new leases for its own stores. | AMBER/GREEN (Roland) |

Huddled (LON:HUD) (£10m) | TU | FY2024 loss in line with expectations. Revenue >£14m, “exceeding exps”. Cash £1.6m. |

Summaries

Polar Capital Holdings (LON:POLR) - unch. at 486p (£496m) - AuM Update - Graham - GREEN

This fund manager suffers a net outflow of £260m in Q3 (£360m if you include the planned closure of a fund). Assets under management rose anyway, thanks to the tailwind of positive market movements, and are up by 9% in the financial year to date. I continue to rate this highly as a pick within the fund manager space. Net flows are still positive overall for the current financial year.

Plus500 (LON:PLUS) - down 3% to £25.60 (£1.92bn) - Year End Trading Update - Graham - GREEN

Today’s full-year update requires some interpretation; the company has “meaningfully” beaten full-year revenue expectations, but this has not been converted into a meaningful increase in the EBITDA result. The company argues that its higher marketing spend will convert into medium- and long-term success but as I’ve argued before, the trading life of a PLUS customer is not typically all that long. Either way, I’m happy to stay positive on this as I’ve learned not to doubt the company’s ability to generate cash and with $900m of its own cash already on the balance sheet, I don’t view this stock as expensive at this level.

Eagle Eye Solutions (LON:EYE) - down 22% to 366p (£109m) - H1 FY25 TU & Multi-year global OEM agreement - Roland - AMBER

Today’s half-year update from this loyalty scheme software specialist reveals a double-digit cut to revenue guidance for FY25 and FY26, with a similar cut to broker earnings forecasts. Eagle Eye is operating in a growing market and benefits from net cash. However, slower sales cycles are a potential concern. I’d like more clarity before considering whether to catch this falling knife, so I’ve downgraded our view to neutral ahead of March’s interim results.

Macfarlane (LON:MACF) - down 1% to 106p (£169m) - Acquisition of the Pitreavie Group - Graham - GREEN

I’m giving the acquisition the thumbs up: the price is a little high but MACF can afford it and the rationale is sound. MACF is cheaply rated and worthy of further investigation in my view.

Short Sections

Filtronic (LON:FTC)

Up 7.5% to 97p (£214m) - Trading ahead of expectations - Roland - AMBER

The supplier of electronics to Space X (and others) has issued another upgrade to guidance, less than a month after its previous upgrade. Management says that “order intake for the current financial year is at a higher rate than anticipated”. Full year results are now expected to be ahead of recently-upgraded market expectations.

Helpfully there’s an update from broker Cavendish on Research Tree this morning. FY25 revenue forecasts have been increased by 11.5% to £48.4m, with adjusted EBITDA up by 22.3% to £13.7m. FY26 forecasts are unchanged. It’s worth pointing out that the company’s brief RNS this morning gives no idea of the substantial scale of today’s upgrade, leaving investors without access to broker notes at a disadvantage.

Filtronic clearly has strong momentum at the moment, but I can see a couple of potential concerns. One is customer concentration – how much of Filtronic’s business is now dependent on SpaceX? Secondly, in December, management said customer orders were being pulled forward (i.e. not additional orders). That comment has not been repeated today, but Cavendish’s decision to leave FY26 forecasts unchanged means that revenue is now expected to fall by 15% next year. Operating leverage means FY26 EBITDA is expected to fall by 31%.

Roland’s view: I remain broadly positive about Filtronic as a business. But the shares are now trading at 32 times FY26 forecast earnings, and there appears to be a risk that profits could fall sharply next year. I’d prefer to stay neutral, at least until the company’s interim results (six months to 30 Nov) are published in February. AMBER.

Sosandar (LON:SOS)

Up 7.2% to 6.7p (£16.6m) - Trading Update & new Store Agreements - Roland - AMBER/GREEN

This women’s fashion retailer has seen its share price fall by more than 75% over the last three years. Today’s update shows sales of £12.2m during the three months to 31 December (Q3 FY25), down from £14.3m in the prior year. The company says this reflects a transition away from promotional activity to full price sales.

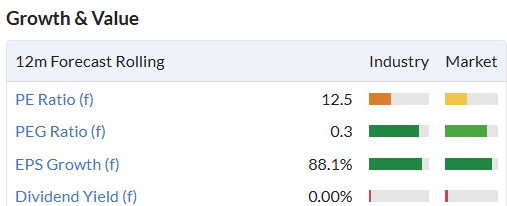

Gross margins were improved at 64.7% (Q3 FY24: 58.3%) and the company says trading remains in line with market expectations for a pre-tax profit of £1m for the year ending 31 March 2025. Stockpedia’s consensus forecasts suggest a rolling P/E of 12.5 with a potentially attractive PEG ratio of 0.3:

Sosander has switched strategy from being online only to pursuing an omnichannel model. It’s opening stores, and today confirms new locations in Bath and Harrogate “where Sosander customers over-index” and says it’s also a top-selling brand on the NEXT and M&S marketplaces.

My main concern here is that you can’t shrink your way to growth – I would want to see revenue starting to rise fairly quickly to justify a more positive stance. But I think this business could be worth a closer look for micro cap investors, at current levels. AMBER/GREEN (Roland).

Graham adds: I am very sceptical of the change in strategy at SOS. The whole point of this company was to provide a pure-play online women’s fashion brand, not just another fashion chain with physical stores. As it is now just another clothing chain, I don’t see any attraction here except for the cash balance (£8m), much of which is likely to be spent on the store roll out. Personally, I’d stay AMBER for now while they try to prove their new business model.

Graham's Section

Polar Capital Holdings (LON:POLR)

Unch. at 486p (£496m) - AuM Update - Graham - GREEN

This is a Q3 update, as Polar’s year end is in March.

In November, we reported on how Polar was one of the vanishingly few fund managers in the UK experiencing net inflows (net flows of £472m for H1, April-Sep 2024).

Unfortunately, this is no longer the case as net flows for the 9-month period (April-Dec 2024) are now only £212m, implying outflows of £260m in Q3. While the Emerging Markets funds continued to enjoy inflows, there were outflows from the European Opportunities Fund, the Global Technology Fund and the UK Value Fund.

CEO Gavin Rochussen points out that flows during this Q3 period are still much better than they were during the corresponding Q3 period last year. Last year, clients withdrew a net £1.1bn in Q3.

He also notes that the broader funds industry, and Polar itself, was particularly weak during the Budget period:

"Net outflows during the quarter were primarily concentrated in October, mirroring the broader UK funds industry, which experienced its third worst month on record ahead of the Chancellor's Autumn Budget. Including the impact of a fund closure, net outflows for the month of October totalled £301m. Net outflows in December were £76m. November saw net inflows of £17m.

Looking on the bright side, market movements have been very positive and have boosted AuM by almost £1.5 billion in Q3, having a far larger impact than the outflows during the quarter. AuM has risen to £23.8 billion.

Performance fees: good news here with £8.3m of performance fees earned in the financial year to date, not far off last year’s £9.6m. Most of these fees relate to one fund.

Graham’s view

I’m slightly disappointed that Polar couldn’t pull another rabbit out of the hat and give us another quarterly inflow. However, there are many consolation prizes: the improved year-on-year performance, the stabilisation in Nov/Dec, the fact that the entire industry funds industry suffered in Oct, and the positive market movements helping to sweep Polar’s AuM up to fresh highs.

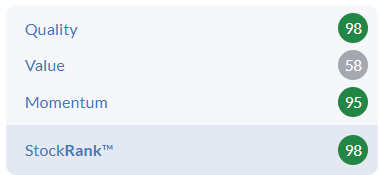

I continue to view this as a quality business trading at an attractive price. The StockRanks are in agreement: the QualityRank is 99, while the overall StockRank is 94.

Plus500 (LON:PLUS)

Down 3% to £25.60 (£1.19bn) - Year End Trading Update - Graham - GREEN

At its Q3 update, CFD trading platform PLUS said that its market expectations were:

Revenue $724.5m

EBITDA $338.3m

It also said that it was trading in line with expectations.

Today we learn that the full-year outcome is going to be:

Revenue $768m

EBITDA $342m

The question that immediately springs to mind is why EBITDA hasn’t come in much higher, given that that revenue is “meaningfully” ahead of expectations.

The answer is that they’ve been spending heavily on new customer acquisition:

The Group's sophisticated and proprietary marketing technologies drove a significant increase in New Customer acquisition during the year, including more than 36,000 New Customers in Q4 2024 alone, which equates to an increase of c.45% versus Q3 2024. As the Group has consistently demonstrated historically, current customer acquisition lays the foundation for future performance, making it an investment in Plus500's medium to long-term growth.

However, as I’ve argued before, customer churn is a big issue at PLUS. In the first nine months of 2024, the company recruited 82,000 new customers (15% higher, year-on-year), but its total number of active customers nudged up only very slightly to 211,000. Is it possible that customer churn is getting worse?

Today we learn that the company just recruited 45,000 new customers in a single quarter, helping to boost revenues by $40m+ vs. expectations, but the EBITDA result didn’t budge. All of that customer recruitment must have been very expensive - as these new customers continue to trade in H1 2025, perhaps we will see the investment feeding through to a better EBITDA result in the new year?

A falling EBITDA margin is not a new issue at PLUS. In October we were told that falling margins were due to “the ongoing investment which the Group has made and will continue to make to enter new markets, develop new products”.

It’s fortunate that the company has such enormous profit margins to begin with (over 40%), so that it can afford to go heavy on investment. The full-year result is now headed for an EBITDA margin of 44%.

Cash falls from $950m in September to $900m in December.

Strategic progress: PLUS has gained a clearing membership with ICE Clear US (part of the Intercontinental Exchange, one of the biggest exchange groups in the world), and a new license in the United Arab Emirates.

2025 outlook: confident. PLUS is “well positioned to continue executing against its strategic roadmap of expanding into new markets, developing new products and deepening engagement with customers…”

Graham’s view

I’ve always been a little bit critical and a little bit sceptical about this one. However, I’ve also learned to stop doubting its ability to generate cash, and I’ve been fully GREEN on this for a year, during which time it has generated a total return of over 50%.

If I was to put my sceptical hat on, I would argue that customer churn seems to be getting worse, raising the ever-present risk that the company’s marketing machine runs out of prospective customers to target. EBITDA margin is falling and cash is falling as the company has to spend ever larger sums in order to find new recruits.

But that would be overly negative, I think. An EBITDA margin of 44% is still excellent, no matter which way you look at it. It’s the sort of margin that most companies in most industries would envy.

Furthermore, the cash balance is still (probably) large enough to manage any risk associated with customers’ unhedged trades, even after all the investment activity in recent months, and after $360m was returned to shareholders in 2024 in the form of buybacks and dividends.

Finally, the company's new licenses point to an increasingly diverse and sophisticated product set.

I’m going to stay GREEN on this, while reiterating that I consider CMCX and IGG to be lower-risk investments (I’m long IGG).

Macfarlane (LON:MACF)

Down 1% to 106p (£169m) - Acquisition of the Pitreavie Group - Graham - GREEN

This Glasgow-based packaging group announces a meaningful acquisition, costing c. 10% of its market cap.

Pitreavie (external link) “designs, manufactures and distributes protective packaging, supplying to customers in the food & drink, energy, electronics and industrial sectors, primarily in Scotland.” It has 159 employees at four locations across Scotland.

Rationale: “The blend of businesses Pitreavie operates complement both the Distribution and Manufacturing operations of Macfarlane.”

Financials: Pitreavie generated sales of £24.8m in 2024, adj. EBITDA of £2.5m and adj. PBT of £1.3m.

The price: £18m, including an earn-out of up to £4m over two years.

Macfarlane will inherit debt of £4m but will get paid a “completion adjustment” to reflect this, effectively a refund on the purchase price..

How to fund it: using MACF’s £40m bank facility. Checking the most recent trading update in November, I see that MACF’s net bank debt was only £5m, so it sounds like they have plenty of headroom available to fund this.

CEO comment:

"Pitreavie is a fast-growing, well-invested company with an experienced management team that is fully committed to the business. The acquisition represents a unique and exciting opportunity to grow our business in Scotland and provide in-house supply to our businesses in the North of England."

Graham’s view

I do like small, debt-funded acquisitions that are still large enough to make a useful contribution to overall profits.

The price paid for Pitreavie is arguably a little punchy. The trailing price to sales ratio for the deal is 0.72x, which is higher than MACF’s own trailing price to sales ratio.

Similarly, the adjusted P/E ratio for the deal is 18x, much higher than MACF’s own P/E ratio.

At least the risk has been mitigated by the earn-outs: if Pitreavie doesn’t meet targets over the next two years, then the P/E ratio would reduce to 14x.

And as part of a larger group with shared buying power and expertise, we can of course hope that Pitreavie’s profitability will be reinforced in the years ahead.

Overall, I’m going to give this deal the thumbs up. The price does seem a little high to me, but MACF can afford it. MACF itself remains an interesting proposition at this valuation:

Both its share price and its profits have treaded water in recent years:

Roland's Section

Eagle Eye Solutions (LON:EYE)

Down 22% to 366p (£109m) - H1 FY25 Trading Update & Multi-year global OEM agreement - Roland - AMBER

Eagle Eye specialises in providing software that creates tailored customer discounts for retail loyalty scheme members. Unfortunately today’s update appears to be a profit warning.

FY25 & FY26 Revenue is now expected to be c. 15% and 18% below current market expectations, respectively

The company has also issued a second RNS today about a new partnership agreement. No numbers are provided but the deal has been hailed as a “game changing opportunity” by management.

However, investors seem more focused on the numbers today. The shares are down by 22% as I write:

Checking back in the archives, we’ve covered Eagle Eye regularly in the past, most recently here.

Let’s unpack today’s updates in a little more detail – and try to estimate the impact of today’s downgrade on expected earnings.

H1 trading update: new wins secured during the first half of the year have included “a leading UK retailer”, plus Waterstones, Côte, RONA (in Canada) and Transa Backpacking (Switzerland). The company’s previous last TU in November also mentioned work with Asda and “increased engagement” with Morrisons.

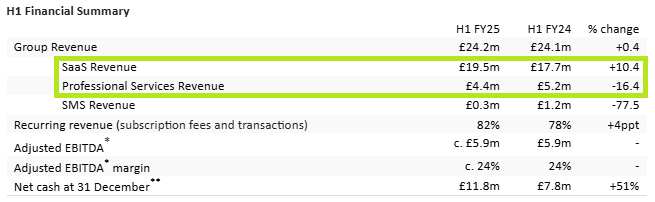

However, this work does not appear to have translated into an improved financial performance. The H1 financial summary today shows flat revenue and EBITDA profits for the half year:

Like many software companies, Eagle Eye is trying to shift its business away from one-off fees and towards recurring subscription revenues. This does sometimes result in weaker near-term revenue, but stronger long-term performance.

We can see this in today’s update – highlighted above – with SaaS (subscription) revenue up and professional services revenue down. SMS services are largely being phased out, from what I understand, so I’d ignore these.

The proportion of recurring revenue has risen to 82% from 78% in H1 last year. I see this as positive, as it should help to support predictable cash flows.

Adjusted EBITDA isn’t my favourite measure of profit but has remained stable, with an EBITDA margin of 24%. This suggests the shift from professional services to SaaS is not affecting profitability.

Net cash was £11.8m at the end of December, an increase of £1.4m from the end of June 2024. This represents 10% of the market cap after today’s fall – a useful buffer to support continued growth and protect equity holders. Hopefully this means no further dilution will be required:

Outlook: this is the bad bit.

Eagle Eye says that SaaS revenue is expected to continue growing at double-digit levels in FY25 (y/e 30 June) and FY26, but group revenue is expected to be c.15% and 18% below current market expectations, respectively.

The company says this is due to “lengthening sales cycles due to the macroeconomic climate” and a continuing decline in professional services revenues.

Consensus revenue forecasts on Stockopedia were previously £56.4m (FY25) and £64m (FY26). My sums suggest the updated figures based on today’s guidance should be £48m and £52.5m, which is supported by updated estimates from broker Shore Capital today.

The company says the impact on profit will be mitigated by (implied) higher EBITDA margins of between 24% and 25%.

I say implied, because Eagle Eye reported a 24% EBITDA margin in both FY24 and in today’s H1 numbers. So this only seems to be a very modest improvement in profitability.

However, Shore Capital was apparently expecting margins to fall to 22%/23%, so today’s guidance does represent an improvement on prior expectations.

Dropping down to the bottom line, Shore has made the following changes to its earnings estimates today:

FY25 adj EPS down 11% to 20.1p (previously 22.5p)

FY26 adj EPS down 17% to 17.6p (previously 21.3p)

Previous consensus estimates shown in Stockopedia were just under 20p for both years. This means that today’s update represents a significant downgrade to the outlook for FY26, in particular, which is now expected to see a material drop in profits versus FY25.

“Game-changing” OEM agreement: in a separate RNS today, Eagle Eye has reported (limited) details on a new five-year partnership with “one of the world’s largest enterprise software vendors”. The company isn’t named.

Eagle Eye’s software will now be integrated into the vendor’s own “new cloud-based loyalty solution”. This is due for launch in 2025 with first customers live in early 2026.

The new loyalty solution will apparently have key elements of Eagle Eye’s platform embedded into it:

including its highly flexible and scalable Omnichannel Promotions, Real-Time Loyalty and Cloud-based Basket Adjudication services

No figures are provided, but this partnership is said to provide Eagle Eye with the opportunity to expand into new global markets and sectors:

Once the product is live, the agreement provides the opportunity for significant contribution to Eagle Eye's Annual Recurring Revenue over time, with a minimum three-year commitment commencing in the current year.

Roland’s view

Today’s partnership news sounds positive, but at this stage I think it’s impossible to know how much value we might attach to it in terms of future earnings.

Today’s cut to FY26 revenue guidance suggests to me that management and the company’s brokers are not factoring more than a minimal contribution in FY26 at this stage.

Using Shore Capital’s updated earnings estimates, Eagle Eye shares are now trading on a FY25 P/E of 18, rising to a FY26 of c.21.

That’s actually cheaper than the stock’s rating at last night’s close:

I think the caution implied by the market’s de-rating of the stock is sensible.

Although today’s update does not suggest any fundamental problems with the business to me, I am concerned by the apparent low profitability of this business. Slowing growth suggests to me that improvements in margins could take longer to come through:

I am not tempted to rush in and buy after today’s profit warning. However, Eagle Eye does appear to have positive cash flow and benefits from a substantial net cash balance, so there doesn’t seem to be any near-term risk of financial distress.

I’m going to reduce our view to AMBER for now, pending a review of the half-year results when they’re published in March.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.