Good morning! What are the chances of another day without any profit warnings, mishaps, or unwanted surprises?

Update at 7.30am: it looks like we have possibly started a streak of days without any profit warnings!

1pm: thanks for dropping by, see you tomorrow!

Spreadsheet accompanying this report (updated to 17/1/2025)

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Intermediate Capital (LON:ICG) (£6.2bn) | TU | $22bn raised in 12 months, 2x 2023. Fee-earning AUM +2.8% QoQ to $71bn. | |

easyJet (LON:EZJ) (£3.9bn) | TU | Q1 LBT of £61m, improved vs LY. ASK capacity +11% YoY. Holiday profit +39%. FY25 outlook in line. | AMBER/GREEN (Roland) |

Quilter (LON:QLT) (£2.2bn) | TU | Core net inflows £2bn in Q4, £5.2bn for the year. | |

J D Wetherspoon (LON:JDW) (£747m) | TU | H1 LfL sales +5.1%. LfL sales for main Christmas period +6.1%. Labour-related costs to rise £60m. | AMBER (Graham) Downgrading this as I'm not sure it has enough of a profit margin (after interest costs) to absorb higher NICs from April. |

LBG Media (LON:LBG) (£261m) | Full-year Results | Ahead of exps for 2024 and positive Q1 for FY Sep 2025 gives confidence for new financial year. | AMBER (Graham) US expansion provides a growth opportunity. Perhaps it's fairly valued at current levels. |

Enquest (LON:ENQ) (£246m) | Acquisition of Harbour Energy Vietnam business | $84m. 53% interest in 2 production fields. Fast payback, low capex, reduced carbon intensity. | |

Beeks Financial Cloud (LON:BKS) (£177m) | Exchange Cloud now live with Nasdaq | Agreement enables Nasdaq to offer cloud infrastructure and analytics. Underpins FY25 exps. | AMBER/GREEN (Roland) |

| Secure Trust Bank (LON:STB) (£88m) | Media: Reeves bids to intervene to cut lenders’ £30bn bill | Treasury applies to Supreme Court to prevent economic harm from excessive compensation. | AMBER/GREEN (Graham) A proportionate outcome to legal situation is now more likely. |

Headlam (LON:HEAD) (£112m) | TU | Rev -9.7% to £593m. Adj. pre-tax loss c. £34m. Cash £11m and remaining properties worth £95m. | AMBER (Roland) |

Colefax (LON:CFX) (£46m) | Half-year Results | H1 sales+1.8%. PBT -0.5% to £4.4m. Strong in US, challenging in UK/Europe. Cash £18.6m. | |

Transense Technologies (LON:TRT) (£24m) | TU | FY25 in line. H1 revenue +37% at £2.4m, but net earnings exp c.20% below prior H1, due to hiring. | |

Itaconix (LON:ITX) (£21m) | TU | 2024 results to be in line with expectations. Rev $6.5m, GP margin +4% to c.35%. | |

Cordel (LON:CRDL) (£17m) | Half-year Results | Revenue +16% to £2.3m, EBITDA loss reduced to £159k. No. clients +3 to 11 during half year. |

Graham's Section

Secure Trust Bank (LON:STB)

Up 33% yesterday to 462p (£88m) - Close Brothers, Lloyds Banking, Secure Trust jump on UK bid to protect car-loan providers - Graham - AMBER/GREEN

I’ve chosen STB to be the main stock mentioned here, as it had the most extreme reaction to yesterday’s news (up 33%).

We also had Close Brothers (LON:CBG) up 22% and S&U (LON:SUS) up 15%. At the bigger end of the spectrum, Lloyds Banking (LON:LLOY) was up 4%.

The case in question is not just about discretionary commission arrangements for car loans, but about the presence of commissions arrangements in the first place, where the active consent of the customer has not been obtained.

The Court of Appeal ruled on this in November, and the case is now progressing further to the Supreme Court.

The Court of Appeal ruled that a car dealer, when acting as a broker, had a fiduciary duty to their customer, and this implied the requirement that it needed the fully-informed consent of a customer to the payment of a commission for arranging a loan.

I’m not a lawyer, but I’ve always understood that a fiduciary duty - the obligation to put someone else’s interests ahead of your own - is something that falls on a doctor or a lawyer, someone who is entrusted with a great responsibility for the welfare of another person. Or in the financial sphere, a fiduciary responsibility often arises when someone is entrusted with the financial wellbeing of others, for example when they are investing other people’s money on their behalf.

However, I’ve never ever thought that a car dealer had a fiduciary responsibility. If a car dealer has a fiduciary responsibility, then I think almost anyone you do business with has a fiduciary responsibility. But that’s where we are, apparently.

Rachel Reeves and the Treasury are trying to stop another PPI-style disaster for the financial industry:

…the Treasury submitted an application to the court arguing it should be able to contribute evidence in a case that could “cause considerable economic harm” and make car loans harder to get and more expensive.

The Treasury submission on Monday added that the case might “generate a perception that regulation in the UK is uncertain”. The letter, first reported by the Financial Times, also warned judges that “any remedy should be proportionate to the loss actually suffered by the consumer and avoid conferring a windfall”.

Not everyone is happy with this intervention. Law firms such as Slater & Gordon (you may remember them as the purchasers of Quindell) can make a fortune from these compensation cases:

Elizabeth Comley, chief operating officer of the law firm Slater and Gordon, said her firm represents “tens of thousands of individuals who have been unfairly impacted” by car finance sellers’ practices.

She said: “While we recognise the importance of maintaining confidence in British lenders, this cannot come at the expense of justice for the individuals affected.

Consumers deserve accountability and redress when they have been wronged, and Rachel Reeves’ attempts to shield lenders from the consequences of their actions risk undermining public trust in the financial sector as a whole.”

Graham’s view

I was GREEN on STB at much higher levels (836p), while Paul was RED after legal issues arose in Nov 2024 (see here).

The difficulty is that STB was (and I still think is) extremely cheap, but the risks are difficult to quantify.

I’m going to moderate my view to AMBER/GREEN: it remains amazingly cheap, but for a reason. If it turns out that consumers can only claim compensation for harm actually caused - at worst, this might be a slightly higher cost of finance than they would have agreed to - then I don’t think there is much to worry about. That outcome is more likely now than it was yesterday, but I can’t predict what might happen.

J D Wetherspoon (LON:JDW)

Down 1.5% to 602.4p (£738m) - Trading Update - Graham - AMBER

This is a brief H1 update, the main purpose of which is to have a pop at people who prefer dinner parties to pubs.

On the financials:

25 weeks to mid-January: LfL sales up 5.1%, led by slot/fruit machines up 11.7%.

Total sales up 4%, lower than LfL sales as there have been a few disposals.

LfL Christmas sales up 6.1%.

Debt is expected to finish the current financial year (FY July 2025) between £680-700m, slightly up on the £660m at which it finished FY July 2024.

Property: nine pubs to open this year. The estate currently consists of 796 pubs.

Outlook: it’s another funny outlook statement from Tim Martin, but with a political point, calling on the government to end the VAT discrimination against pub-goers and in favour of people who like to have dinner parties in their homes (supermarkets pay no VAT on food, while pubs pay 20%).

The other main point is that labour-related costs will increase by c. £60m annually (from April when the new tax changes kick in), and Tim Martin argues that this is another instance where supermarkets have an unfair advantage over pubs, as supermarkets are less impacted by government-mandated wage increases.

Graham’s view

Given that JDW only earned £74m of adjusted PBT last year (FY July 2024), under the old national insurance regime, I’m very concerned as to how it’s going to mitigate £60m of additional wage costs. Even if it fully mitigated 50% of the increased costs, that could still potentially cut down profits by about half.

If it was debt-free, it could have absorbed these costs into its c. £140m of operating profit.

But after paying its hefty interest bill, it doesn’t seem to have a lot of wiggle room to pay extra costs.

The shares have de-rated since around the time of the official announcement of the upcoming changes (marked blow in pink), but only by around 15%, not by an amount that suggests great alarm:

Tim Martin isn’t promising much, only saying:

"The company is confident of a reasonable outcome for the year, although forecasting is more difficult, given the extent of the increased costs."

Consensus forecasts suggest that the company can earn after-tax profits of about £60m in the current year (FY July 2025), but this only includes four months of higher NICs. What about the financial year after that, which begins in a little over six months? Forecasts suggest that earnings will increase pleasantly that year, despite it being the first full 12 months during which the company must face these higher wage-related costs.

I’m worried that the FY July 2026 could be a poor one, and that JDW might have taken on a little too much leverage given the deterioration in trading it could be about to suffer. I’m going to downgrade this to AMBER, as I’m concerned that current forecasts may need to be revised quite a bit lower.

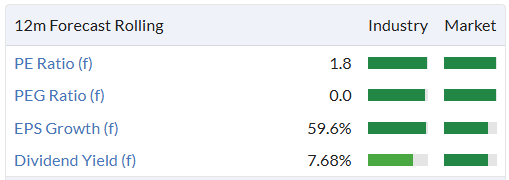

LBG Media (LON:LBG)

Unch. at 125p (£261m) - Full Year Results - Graham - AMBER

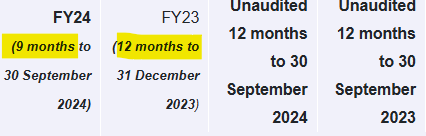

LBG Media, the global digital entertainment business with a focus on young adults, is pleased to announce its results for the nine months ended 30 September 2024 ("FY24" or "the period"). Following the change in year-end, statutory financial results are being reported for the nine months ended 30 September 2024.

It’s a little confusing straight away, as the company reports results for nine months but then immediately tells us that its performance is ahead of market expectations “for the calendar year to December 2024”.

These expectations, for what its worth, are revenues of £86.3m and adj. EBITDA of £23.4m.

None of these time periods given are entirely satisfactory:

FY24 (9 months) can’t be directly compared to FY23 (12 months), and the unaudited 12-month periods to September don’t include the three most recent months.

For now, I’ll use the unaudited 12-month periods to September. The headlines are that revenue rose 22% to £86m and that PBT rose 32% to £14.5m.

LBG owns Unilad, Lad Bible, Sport Bible, etc. It claims to be “one of the largest publishing groups in the world”.

It makes nearly as much money from “Direct” sources as “Indirect” sources, meaning revenue that is shared with a social media platform such as Facebook.

It is one of Facebook’s largest publishers, which unfortunately I would view as a risk as sites such as Facebook can change their policies and algorithms on a whim.

This happened during 2024, but LBG seems to have survived it ok:

From July to September 2024, changes to Facebook's commercial model resulted in lower Indirect revenues from Social compared to the same period in the prior year. As with previous platform changes, we were able to adapt quickly and saw a return to normalised levels on exiting Q1 FY25, providing positive momentum for the remainder of the new year ahead

Outlook:

The Group has entered FY25 with good momentum across its three growth lenses of Direct, Indirect, and U.S. expansion. The Board remains confident in the size of the opportunity ahead and may consider further investment to accelerate the U.S. growth strategy.

Building on a robust first quarter that achieved double-digit growth compared to the same period last year, management is confident in the growth trajectory for the remainder of FY25 and expects revenue to increase by approximately 10%.

CEO comment:

"2024 was a transformational year for LBG Media. We are running more campaigns for more blue-chip brands, particularly in the U.S., the largest advertising market in the world…

More than half a billion people globally, including Gen Z and Millennials, see us as the go-to destination for digital content. The biggest brands and the biggest celebrities therefore want to partner with us to access the growing buying power and influence of this hard-to-reach demographic…

Estimates: Zeus have updated their forecasts to reflect the change in the accounting year-end.

They see current year (FY Sep 25) revenues of £94m, rising to £104m for FY Sep 2026.

Over these two years, adj. PBT is forecast to rise from £21.6m to £23.1m.

They calculate that that stock is trading at a PER of 15x for FY26.

Graham’s view

I’m too old now but even when I was younger, I never saw the appeal of LADbible or Unilad.

But I should put that bias to one side and look at the facts and figures.

The brands that LBG works with are undeniably blue-chip and of the highest quality: Google, Lloyds, and Costa Coffee are mentioned as examples where LBG has built “deeper, more strategic partnerships”. LBG says it has become “an integral part of corporate marketing strategies”.

The cash position is fine at £27m, with no debts, even after £20m was spent on an acquisition to boost US-led growth.

Balance sheet equity is about £36m after you deduct intangibles - not enough to support its market cap but it’s nice to see that the company has a positive position.

Overall, perhaps I’m biased by my (generally negative) attitude towards its main titles, but I can’t bring myself to give this a positive stance, even though I admit that there is nothing obviously wrong with these results or with the outlook.

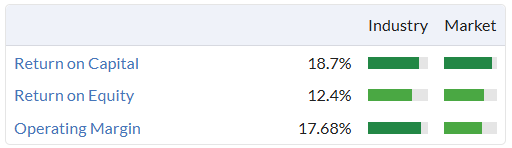

Quality metrics are good:

The valuation arguably reflects this:

Where the investment case falls down for me personally is that I don’t have any conviction that LADbible/Unilad will be relevant long-term. But again that may just be a reflection of my personal bias.

What is more objective is the risk faced by publishers that the likes of Facebook will change their algorithms or payout calculations. That risk is always, always there, and I do think it should affect how investors think about the publishers who rely on these platforms.

I’m happy to put this at AMBER, but I can see that someone else might give it something better.

Roland's Section

Beeks Financial Cloud (LON:BKS)

Up 9% to 287p (£193m) - Beeks’ Exchange Cloud now live with Nasdaq - Roland - AMBER/GREEN

Beeks Financial Cloud provides cloud computing and connectivity for financial markets. Today’s update confirms the identity of a major new client as exchange operator Nasdaq.

[Beeks] … is delighted to confirm that the major Exchange Cloud Customer announced on 6 February 2024 is the Nasdaq Stock Market (Nasdaq), a global technology company serving capital markets and other industries. The service is now live, with customers expected to be on-boarded at the end of February.

This news has been well received, sending the stock up 8%, but it does appear to have been an open secret due. I’ve seen it commented on previously (including here), but it’s good to have confirmation.

Beeks says that its Exchange Cloud service will initially be deployed in Nasdaq’s core data centre in New Jersey, “with the potential for further expansion”. The agreement enables Nasdaq to offer Beeks’ services to its customers, but does not appear to guarantee a specific level of demand.

Guidance unchanged: this deal appears to have the potential to make a significant contribution over time. But it looks like the impact on FY25 earnings (y/e 30 June) will be modest, merely supporting existing guidance (my bold):

Consequently, this material multi-year contract has scope to grow, further supporting the Group's growth aspirations, as well as underpinning the Board's FY25 expectations.

Estimates: with thanks to broker Canaccord Genuity, we can see that earnings forecasts are unchanged today:

FY25: 7.7p per share (+21% vs FY24)

FY26: 9.5p per share (+23% vs FY25)

Canaccord also says it expects to see c.40% revenue growth and a c.1.8% improvement in operating margins for FY25. Operating margins have deteriorated as the group has expanded, so I think this would be welcome news:

Roland’s view

Nasdaq is clearly a valuable reference customer and is presumably endorsing the value of Beeks’ services to its exchange members. The acid test will be how strong takeup is over the next 12 months or so.

I do not know all that much about Beeks’ services, but I assume that Nasdaq exchange members currently use alternative low-latency colocation services to meet their needs. So the test will be whether Beeks can demonstrate sufficient benefits to justify members switching to a new provider.

Revenue has grown at an average 31.5% CAGR since 2019 – an impressive record that suggests to me the company could have some competitive advantages:

However, this revenue growth has not yet really translated into improved profitability. Last year’s results (covered here) showed an operating margin of just 5.5%, with a sub-4% return on capital employed.

My understanding of Beeks’ business model is that it requires fairly heavy upfront capital expenditure to set up the necessary infrastructure in client data centres. This should then be followed by years of sticky, recurring revenues. At least, that’s the bullish investment case.

The StockReport shows Beeks generating positive free cash flow last year for the first time (since at least 2019):

One concern for me might be the possibility that equipment renewal costs will be high and fairly frequent – last year’s accounts showed a £5m depreciation charge, for example.

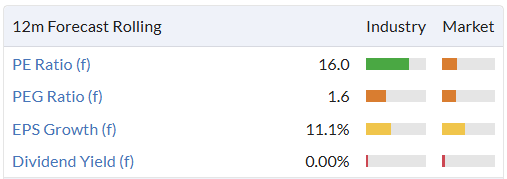

I can see the bull case here, but it’s probably fair to say that a certain level of optimism is already priced into the stock at >30x forecast adjusted earnings (Beeks is quite a heavy adjuster):

The shares are up 150% over the last year. The rolling PEG ratio of 1.0x above suggests to me the stock may be reaching a point where it’s fairly priced for expected growth.

I’m impressed by long-term revenue growth here and encouraged by the presence of founder management – CEO Gordon McArthur has a 31.9% holding. I’m going to take a cautiously optimistic view ahead of March’s interim results. AMBER/GREEN.

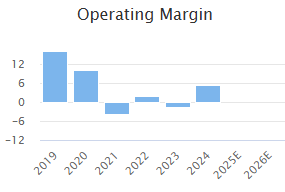

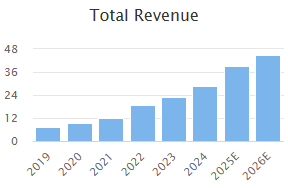

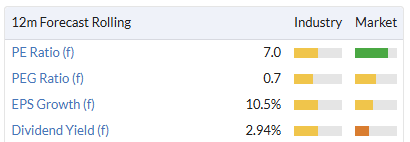

easyJet (LON:EZJ)

Down 5% to 485p (£3.7bn) - Q1 Trading Update - Roland - AMBER/GREEN

Today’s trading update covers the three months to 31 December 2024. That’s traditionally a quiet period for leisure travel. This is reflected in easyJet reporting a loss for the quarter, as is usual for this business.

The market seems a little disappointed by today’s statement. But it doesn’t read too badly to me and appears consistent with the guidance provided in November’s results, which Keelan covered here.

Q1 highlights: easyJet reports a headline pre-tax loss of £61m for the quarter, but this is less than half the £126m figure for the same period last year. Improved operating metrics supported a stronger Q1 performance:

Passenger numbers +7% to 21.2m

ASK* capacity +11%, avg sector length +6%

Load factor: 88% (Q1 24: 86%)

Total cost per ASK down 4%, due to 13% reduction in fuel costs

Revenue per ASK flat, as guided previously

*Available Seat Kilometre - an industry capacity metric

easyJet Holidays generated a £43m profit in Q1, an increase of £12m (+39%) from Q1 last year.

H1 guidance: it looks like H1 results will be negatively affected by the later timing of Easter this year, which means it will fall into H2. The company expects this to cause a £30m hit to profits.

Last year’s release of “aged balances” will also cause a £34m negative comparative versus last year.

However, the company also says that underlying unit revenue in Q2 will be “modestly lower” than in Q1 due to an increase in longer leisure routes. These newer routes are expected to perform better next winter as they mature.

Fuel costs are expected to continue falling in Q2.

FY25 Outlook: guidance is unchanged, with FY25 ASK growth expected to be c.8%.

The traditionally busy Easter period is seeing strong demand and bookings continue to build for Summer 2025. At this early stage of the year, the current booking trends are supportive of FY25 consensus

The company also helpfully provides an internally-compiled consensus estimate for FY25 headline PBT of £709m (FY24: £610m).

easyJet Holidays is expected to report customer growth of c.25% in FY25, although the company doesn’t translate this into expected profit growth.

Profits from the airline’s newish package holiday business rose by 56% to £190m last year, but extrapolating the 39% rate of growth in Q1 suggests the increase might be lower this year.

Slower growth rates are natural as a business scales. I think the holidays business is a valuable, margin-enhancing addition to easyJet’s offering. Presumably the airline saw the success of Jet2’s model and decided that it would quite like to replicate it!

Consensus forecasts on Stockopedia suggest adjusted earnings could rise by 16% to 71.3p per share this year, pricing easyJet on a P/E of 7.

Roland’s view

easyJet says it remains focused on its medium-term target of generating a headline pre-tax profit of £1bn.

Today’s update suggests to me that the business is performing largely as expected and is likely to make progress towards this target in 2024/25.

As we’ve seen with some other airlines, easyJet has been able to repair its balance sheet more quickly than expected following the pandemic. Last year’s results showed a net cash position for the second consecutive year.

This isn’t a sector that attracts high valuations, but easyJet’s share price does not look unreasonable to me.

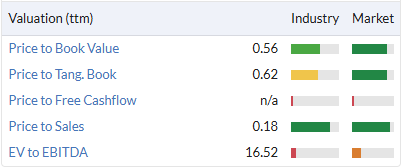

Looked at differently, the stock is currently trading at 1.3x its book value and reported a 15% return on equity last year. Buying the shares at this level would imply a return on cost of equity of 11.5%, which seems satisfactory to me, if not outstandingly good value.

Airlines are traditionally a difficult investment, with high fixed costs and plenty of macro risk. But I’m broadly positive here. AMBER/GREEN.

Headlam (LON:HEAD)

Down 1% to 138p (£112m) - Y/E Trading Update - Roland - AMBER

We’ve commented on this struggling flooring distributor several times recently. It’s been selling some of its large freehold property portfolio to release cash and shore up its loss-making operations.

Today’s year-end update confirms the year-end trading position and cash position after recent property sales.

2024 group revenue down 9.7% to £593m

H2 revenue down 7.4%, improved versus H1 decline of 11.8%

Expected 2024 underlying pre-tax loss of c.£34m

Growth in the Larger Customers and Trade Counters divisions is being offset by weak trading in Regional Distribution.

However, Headlam’s strong balance sheet has proved its worth with property sales generating £54m in December (see here).

These transactions left Headlam with net cash of £11m and a property portfolio valued at £95m at the year end. Those items alone are nearly sufficient to cover the £112m market cap, even without the ongoing value of Headlam’s business and inventories.

Updated estimates: with thanks to broker Panmure Liberum, we have updated earnings estimates for Headlam today.

Unfortunately today’s update appears to have been slightly below Panmure’s previous expectations, so earnings estimates for 2024-2026 have all been cut:

FY24e: loss of 42.4p per share (previously 41.1p)

FY25e: loss of 29.3p per share (previously 26.0p)

FY26e: breakeven (previously earnings of 3.1p per share)

Roland’s view

I don’t think today’s downgrade is too significant. In reality, I think the exact pace of Headlam’s recovery will be dictated as much by external conditions as company actions.

In the meantime, Headlam shares continue to trade at a hefty discount to book value, underlining the value appeal of this stock which Mark discussed here.

I think this provides us with a useful reminder of the value of a strong balance sheet. Headlam seems near-certain to survive long enough for its trading to recover. That might not have been true if it had entered the current slump with too much leverage and a wholly-leased property estate.

The distant timing of a recovery prevents me from taking a positive view, but I’m comfortable remaining neutral. AMBER

Kooth (LON:KOO)

Down 2% to 170p - Trading Update - Mark - AMBER

Revenue is in line, showing some phenomenal growth rates here:

2024 revenues are anticipated to be in line with consensus market expectations of £65.8m (2023: £33.3m).

EBITDA growth is even better, and beats expectations:

Adjusted EBITDA is expected to be at or ahead of the top of the range of analyst forecasts of £12.7m (2023: £2.3m), helped by certain items which are not expected to recur in the current year.

However, it's this last line, which shows that the beat is likely a one-off, which is why the shares are actually down today in response.

I’m not sure I trust the broker consensus here, so doing some simple maths, at the half year, they said:

● Adjusted EBITDA to £7.8m (2023: £0.0m)

● Profit after tax of £3.9m (2023: £0.5m loss)

This gives H2 EBITDA of £4.9m. D&A in H1 was £2.6m, giving PBT of £2.3m and £1.7m PAT on a standard tax charge. That’s £5.6m PAT for the FY or 15.4p EPS. The P/E of 11, then, is potentially not that expensive for a company with their growth track record.

The problem is that their product, which is a mental health platform for teens, has faced some significant pushback in the US. The perceived issue is that parents do not have sight of the support given. My own view is that without something in place, there will be an increasing crisis in teen mental health, and the benefits outweigh the risks in this regard. However, logic rarely wins out in such emotive issues. The good news is that they keep winning pilot projects, although these won’t move the needle unless they become more than a pilot:

As announced in December 2024, Kooth has agreed terms for a new pilot contract with the State of New Jersey valued at $1.45m. Under the terms of the Contract, Kooth is providing mental health support via its Soluna platform to school districts within New Jersey, reaching 50,000 students aged 13 to 18. This pilot went live on 7 January. The Company continues to hold negotiations, which are expected to be concluded in Q1, regarding a second pilot contract in the US.

Mark’s view

This is a potentially interesting growth company, having a positive social impact and on a relatively modest valuation if my maths is correct. The problem is that the political risk in their key market of the US is almost impossible to quantify or mitigate. So it's an AMBER for me.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.