Good morning! There has been chatter that this could be a "Black Monday" if panic continues. At IG, I see that the FTSE is being marked at 7890 (down 2%), while the Dow Jones is marked at 37,200 (down 2.7%), which are on top of the 5% falls on Friday. Looks like we may have another interesting day ahead of us!

To give some context, a year ago the FTSE was 7900. So it's still flat year-on-year, but it has given back all of the gains it made to its recent high at 8870. It has been a sharp 11% correction.

1-year FTSE chart.

The Dow is down 4% year-on-year and it did reach as high as 45,000 a few months ago. So it is down 17% from its high.

Similarly, based on the overnight price of 4910 (down 3%), the S&P 500 is now down by 20% from its high. So it looks like we may officially have a US bear market this week.

8.10am update: the indexes are currently at the following levels in volatile early morning trading.

- FTSE at 7580, down 5.9%

- AIM All-Share at 617.7, down 3.6%

- S&P overnight at 4825, down 4.8%

- Dow Jones overnight at 36,750, down 4.1%

- NASDAQ overnight at 16,410, down 5.7%

The AIM is the best-performing index - who would have guessed!

I haven't sold a single share and look forward to adding to positions when I have available funds.

12:50pm: wrapping up the report there for today. After the initial shock, markets have calmed down with the FTSE recovering slightly and no further overnight falls in the United States. See you tomorrow!

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Shell (LON:SHEL) | Q1 update note | Lower Q1 LNG/gas production due to weather/maintenance issues in Australia. Trading results in line. | AMBER (Roland) Today’s update contains a c.4% downgrade to LNG production expectations, but I don’t worry too much about this kind of detail with Shell. For me, this is a macro/commodity play – and in my opinion, the shares remain in the upper half of their likely cyclical range. I don’t think Shell is cheap enough to justify a positive stance, but I am comfortable with a neutral view given the group’s robust health and useful dividend yield. |

Volex (LON:VLX) (£367m) | FY Trading Update | FY26 profit ahead of exps. Rev exp >$1,060m, +16% YoY. Op profit >$100m. | AMBER (Roland) Today’s full-year update from the industrial wiring specialist is positive, but does not include any outlook commentary for the year ahead. While this is understandable, it also makes it hard for me to have any conviction about the near-term outlook here. I’m opting for a neutral stance ahead of the FY results, when we will hopefully get some more granular commentary on the trading outlook and potential impact of tariffs. |

Applied Nutrition (LON:APN) (£278m) | Interim Results | H1 revenue £47.6m “ahead of guidance” given at the IPO, but this revenue figure was already revealed at the February trading update. Adj. EBITDA of £13.8m is “in line”. Outlook for full year also in line. Trading since half year end remains strong. Expected FY revenue up c. 19% to £100m. Revenue capacity is now around £160m as planned. In the medium term does not expect to be materially impacted by US tariffs. Says it could move production from the UK to the US. | AMBER (Graham) [no section below] I was AMBER/RED on this in February at 148p due to concerns that it appeared to be very richly valued for a sports nutrition brand (which I consider to be a difficult sector for investors). It's also a recent IPO, having listed at 140p in October. I'm happy to upgrade my stance one notch to neutral today as some air has come out of the valuation at the current 108p share price. Today's results are fine with H1 PBT of £11.8m and that is after spending nearly £2m on the IPO. Please note that the IPO did not raise any funds for the company and was purely to enable exits for existing shareholders, including £82m for the founder. |

De La Rue (LON:DLAR) (£212m) | Update on sale of Authentication unit | Conditions now satisfied for sale of this unit for £300m, to be held in escrow for 18 mo post completion. | PINK (Graham) [no section below] Edi Truell's consortium previously expressed an interest in taking out De La Rue at 125p. the company launched a formal sale process in February and according to the March trading update, the company continued to be in discussions with various potential counterparties. It will be interesting to see where the best bid finally lands, assuming it proceeds to a takeover. Today's update helps to clear the way for the disposal of the reminder of the group. |

Quartix Technologies (LON:QTX) (£93m) | TU |

In line for FY expectations. Q1 ARR +6% to £34.2m, price indexation now in “virtually all” customer contracts. Q1 customer signups +18% to 2,206, total customer numbers +10% YoY to 31,040. | GREEN (Roland) [no section below] Since returning from retirement to take charge again, founder Andy Walters is getting the business back in shape, focusing on core operations and addressing issues such as price erosion. Today’s update highlights an 18% increase in customer acquisition in Q1, with new ARR split roughly equally between new and existing customers. Given the strong profitability and positive outlook, I think the High Flyer style looks justified. On this basis I remain positive. |

Likewise (LON:LIKE) (£42m) | TU | Gross rev +10.7% in Q1, branded +14.6%. “Every confidence” in achieving FY objectives. | |

EnSilica (LON:ENSI) (£38m) | Trading Update | Profit Warning. Contract delays. FY25 EBITDA forecast slashed. FY26 revenue £33-35m (cons: £38.3m). | BLACK (RED) (Graham) Downgrading this to RED on the back of a serious profit warning that also reduces guidance for future years. I do still believe that the company has speculative potential but our quantitative rules are clear that this should be considered very high-risk. |

Made Tech (LON:MTEC) (£33m) | Contract wins | Year-to-date sales bookings £68.2m, up 89% on prior full-year performance. Outlook in line. Forecasts at Singers are unchanged including FY May 2025 revenues of £43m, EBITDA £3m and adjusted PBT £2.1m. | AMBER/GREEN (Graham) [no section below] This has fallen nearly 30% since I covered it in February. Valuation is therefore less unnerving than it was previously. The company’s cash balance is c. £9m making for an enterprise value of only £24m. Looking ahead, the FY May 2026 adjusted PBT forecast is £2.4m although I do think the adjustments are questionable, including for example share-based payments. Given the strong underlying momentum I’m happy to upgrade this a notch to AMBER/GREEN. |

Pennant International (LON:PEN) (£12m) | Sale of property (£1.2m) | Contracts exchanged on 3 commercial properties. Proceeds to reduce overdraft borrowings. | |

Smarttech247 (LON:S247) (£8m) | Multi-Year Framework with a London Airport | Total potential value of up to £7m across all four suppliers. No guaranteed minimum spend. | |

| Mycelx Technologies (LON:MYX) (£18m) | Operational and Trading Update | SP down 8% Successful US water trial. Tariff revenue warning: new 2025 range $12.5-15.5m (cons:$15.4m). Steel equipment bought by Mycelx in the US is made from imported raw materials and will be more expensive. Projects quoted by Mycelx but not yet signed must be requoted for customer approval. The CEO says she does not expect any major change to the order backlog. | BLACK (RED) (Graham) [no section below] The news of a successful trial in the United States sounds impressive with MYX’s patented solution removing oil from water (which can then be solid) and enabling the recycling of the water. However, I am obliged to give this a red as it is a Sucker Stock with a revenue warning (albeit one that was beyond its control) and also market cap below £10m, which I consider to be a danger zone. The company does say it will be profitable this year even at the lower end of the new revenue guidance, if we include the gains it made on a recent asset sale. I’ll be open to revising my stance when this materialises. |

Graham's Section

EnSilica (LON:ENSI)

Down 15% to 33.04p (£32m) - Trading Update - Graham - RED

EnSilica plc (AIM:ENSI), a leading chip maker of mixed signal ASICs (Application Specific Integrated Circuits), announces the following trading update for the year ending 31 May 2025 ("FY 2025" or the "Period").

I suggested recently that Ensilica might be focusing a little too much on PR after a spate of contract win announcements that didn’t seem to move the needle in terms of the company's financial forecasts.

We now have a full-on profit warning from them. So when it came to actually delivering a financial result, they are unable to deliver what was expected this year. I’m relieved that I stayed sceptical about this one!

Today’s announcement starts off with positive commentary around contract wins, which I guess is not surprising.

They have won six new design and supply contract wins in first ten months of FY May 2025, that will generate non-recurring engineering revenues of more than $40m over the next two years.

But then the bad news:

Despite these successes and as highlighted as a potential issue in the Company's announcement on 10 February 2025, the Company has experienced two customer delays that will materially reduce NRE revenues in the current financial year. The NRE revenues are the fees charged to customers for the design of their chips, including high-value costs such as tape-out fees and other significant third-party costs.

More detail is provided on the two specific contracts.

This is a company that has a history of heavy customer concentration. Checking the 2024 Annual Report (which also included a going concern warning), I find:

The nature of the design services and projects is such that there will be significant customers as a proportion of revenue in any one year but that these may be different customers from year to year. Revenue in respect of one customer amounted to £8.8 million representing 35% of the revenue for the year ended 31 May 2024, with only one other customer contributing over 10% of revenue.

This is phrased in such a way as to not sound very alarming, but it means that about half of revenues came from just two customers for the year. I do expect that customer concentration for FY 2025 will not be as bad as this, but it remains a key risk.

New FY25 guidance: revenues of £19-20m (StockReport estimate: £29m) and EBITDA of £0.1 - 0.5m (the net income estimate was £2.5m).

2026 outlook: guidance is slashed here, too.

The Board is focused on scaling the business and is confident of doing so given the strength of the forward orderbook. However, predicting the timing of contract completions that include customer dependencies has proved difficult as evidenced by the delays in the current financial year. In response, the Company has adopted a more conservative view on future guidance to allow greater flexibility for project completions. To that end, the Board now expects to deliver revenues of between £33 million and £35 million in FY 2026, with approximately 80% of FY 2026 revenue already covered by existing customer contracts.

At the midpoint, this is a 10% cut in revenue guidance and it also implies a substantial cut to EBITDA/net income guidance.

Graham’s view

I’ve been AMBER/RED on this on the basis that it had a small net debt position that I wasn’t sure it could afford, given its lack of profitability. The going concern statement in the Annual Report last year was also a major red flag.

These factors would ordinarily make this an automatic RED from me. However, Ensilica’s stream of contract win announcements made me think that its customers must have confidence in the company’s ability to perform these contracts and therefore that the financial situation must be somewhat stable.

The company insists today that it is stable and sufficiently funded:

With a strong NRE order book coupled with increasing profits from chip supply, the Board is confident of having sufficient capital to reach positive cash generation at the end of financial year 2026.

Should I now admit that this is too risky to be anything but RED on it? Reasons to have misgivings:

Stockopedia categorises it as a “Sucker Stock”

A serious profit warning for the current year along with downgraded guidance for future years, delaying meaningful profitability

The going concern warning in the last annual report

Heavy customer concentration

Potential impact from tariffs on the chip market? Not mentioned in today's update.

Looking for positives, I would point to:

Backing from customers and partners including the UK Space Agency and European Space Agency

Raised £1.2m in new equity last June

Refinanced its loans in November

Net debt was only £1m as of June 2024, and this includes £2m of lease liabilities.

I think our quantitative rules are clear that this should be a RED, although personally I do still see some high-risk potential upside here.

Roland's Section

Volex (LON:VLX)

Up 10% at 219p (£416m) - FY Trading Update - Roland - AMBER

Volex (AIM: VLX), the specialist integrated manufacturer of critical power and data transmission products, today releases a trading update for the financial year ended 30 March 2025 ("FY2025").

According to Stocko’s index listings, Volex is one of just five shares in the AIM 100 index that have risen this morning!

Today’s update is ahead of expectations, striking a confident note against a chaotic market backdrop (my emphasis):

Underlying operating margins are anticipated to be at the upper end of the target corridor of 9% to 10%, with operating profit of at least $100 million, well ahead of the top end of market estimates.

Here are the main financial highlights from today’s update:

Revenue up 16% to “at least $1,060m” (+8% constant FX)

Underlying operating margin expected to be “at upper end of 9%-10%”

Operating profit of “at least $10 million”, well ahead of market estimates

Net debt to EBITDA leverage 1.1x at 30 March

Last year’s underlying operating margin was 9.8%. This dropped through to a statutory figure of 7.0%. So my impression is that margins for the year just ended were probably similar to the last couple of years on both a reported and adjusted basis:

Trading commentary: executive chairman and 25% shareholder Nat Rothschild says the group had “a strong fourth quarter”, with good success in securing new projects.

Improved profit margins were driven by a “favourable product mix, including increased demand for data centre products”. There were also some “incremental operational improvements”.

Performance was mixed across the group’s divisions:

EV & Consumer Electricals: “strong momentum, securing several new key customer relationships”

Complex Industrial Technology: “notable strength, delivering low double-digit organic growth” – this appears to have been driven by data centre demand as “a major customer” accelerated their infrastructure investment

Medical: sales fell against a strong comparative period that benefited from catch-up sales

Off-Highway: revenue flat as softer conditions in some markets were offset by “several strategic customer wins”. Management says that “integration activity continues” in this unit, which includes the recently-acquired Murat Ticaret business.

Outlook/tariffs: no new broker notes are available to me today and perhaps understandably, there is very little commentary in today’s update on the outlook for the year ahead.

The company acknowledges that the impact of tariffs is currently hard to predict:

The breadth and rapid evolution of recent changes in international trade policies and market dynamics are unprecedented, making precise quantification of direct and indirect impacts challenging and increasing operational complexity.

However, Rothschild is keen to emphasise Volex’s value-added and embedded position in its customers’ supply chains:

The majority of Volex's products represent essential components within complex supply chains. In many instances, Volex is either the sole provider or one of very few qualified manufacturers capable of meeting demanding technical and operational requirements, fostering strong customer reliance. Incremental costs arising from tariff changes are expected to be passed through to customers, underscoring the robustness of Volex's competitive positioning.

Checking back to the H1 results, 42% of Volex’s revenue was generated by deliveries to customers in North America. As far as I can see from this map, the group’s manufacturing mainly takes place in China, plus Vietnam, Indonesia, Poland and Mexico.

Volex doesn’t appear to have any manufacturing capacity in the US, so it seems reasonable to assume at least some of its sales will be affected by tariffs.

For what they’re worth, consensus forecasts prior to today showed adjusted earnings falling by 7% to 31.3 cents per share in FY25, before returning to growth in FY26. This view was consistent with H1 adjusted EPS of 15.2 cents per share.

I’m not sure how much of an upgrade to expect to FY25 figures after today’s update, but in some senses I suspect it’s not that relevant. The FY25 year has ended and it looks as though the outlook for FY26 could change.

The forecasts shown above price Volex on a FY26E P/E of eight after this morning’s gains – that seems a reasonable valuation to me, given the likelihood that forecast earnings for the current year could be trimmed.

Roland’s view

Volex shares have drifted lower over the last year. They then de-rated sharply when Trump’s tariff ‘liberation day’ was announced:

I have owned this stock in the SIF folio in the past (no position at present) and have generally had a fairly positive view on the business.

At this stage, it’s not clear how much of a headwind the tariff regime will be.

In reality, we don’t even know if the situation will be the same in a month from now, far less how it might affect volumes and margins over the coming year.

However, it seems prudent to me to expect an overall negative impact. I think it’s also worth remembering that Volex has a material amount of debt – reported at $205m at the end of H1.

For these reasons, I’m going to take a neutral view on the shares until some clarity emerges and we get updated guidance for the year ahead.

It’s worth emphasising that my view is based on a review of the numbers and a superficial overview of the current trading environment. An investor with deep familiarity of this business might be able to have a stronger conviction (positive or negative) than me. Therein lies the opportunity of DYOR.

Shell (LON:SHEL)

Down 7% at 2,305p (£141bn) - Q1 2025 update note - Roland - AMBER

It’s a big day when Shell is down 7%, single-handedly knocking £9bn off the FTSE 100. I estimate that’s about 0.45% of today’s index fall – or around 10% of the entire UK market move so far this morning.

As we discussed on last week’s webinar, market concentration is a factor in the UK market too, not just the US.

However, I don’t think that much of today’s sell-off is directly linked to Shell’s update this morning. BP is also down 7%, after all.

Q1 update: Shell issues a quarterly “update note” ahead of its quarterly results. These notes contain a list of production metrics and financial details that might affect earnings estimates. It’s an unusual format that seems mostly to be designed for City analysts with detailed models of the group’s business.

I don’t have a detailed spreadsheet to model Shell’s earnings, so I usually just look for anything that suggests a significant variation from previous guidance.

Today’s numbers appear to flag up one main area of disappointment:

Q1 LNG production: now expected to be 6.4-6.8m tonnes, down from 6.6-7.2m tonnes previously. This is said to be due to bad weather (cyclones) in Australia and some unplanned maintenance outages.

All the other main numbers appear to be in line with the Q1 guidance included in January’s 2024 results.

Importantly, the contribution from Shell’s trading division (referred to as Trading & Optimisation) is expected to be in line with previous expectations. Shell and BP make a lot of money from commodity trading, although they’re usually careful to avoid revealing exactly how much.

The only other number I’ll point out is that the contribution from “renewables and energy solutions” is expected to be for adjusted earnings of ($0.3bn)-$0.3bn. Shell generated adjusted earnings of over $28bn last year – renewables are not currently making a meaningful contribution to the group’s bottom line.

Roland’s view

LNG sales are a key element of Shell’s business model, so I guess some analysts may tweak their Q1 forecasts slightly lower following today’s update.

However, I don’t see this as a stock where there’s any point in focusing on such minor details. In my view, this remains a macro commodity play, where what matters are oil and gas prices – and the health of the global economy.

For some time now, I have held the view that Shell’s valuation has been towards the top end of its likely cyclical range.

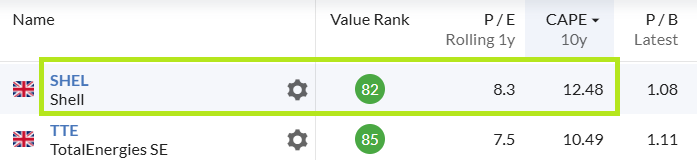

That remains true – the shares were still trading on a CAPE 10y of 12.5 (prior to today). I’d look for a mid-high single-digit number as an indicator of cyclical value here:

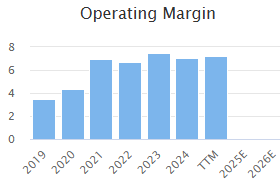

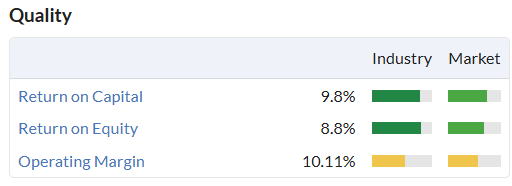

After all, this is a relatively capital-intensive business with quite average quality metrics:

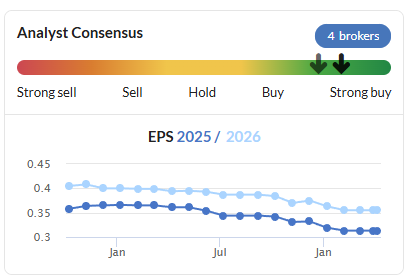

The StockRanks are also now starting to reflect this view, with a Neutral style rating and sharp fall in MomentumRank:

Brent Crude oil has fallen by 16% to $63/barrel over the last week. US natural gas prices are down 10% over the same period.

On a personal, anecdotal level, I’ve been bombarded with emails from my usual heating oil supplier, inviting me to buy oil at “six-month low prices”.

I don’t know if oil and gas prices will drop further, but if the US and other markets do see a recession, I think Shell shares could still have further to fall. Historically, peak-to-trough falls of 30%+ are not unusual for this business:

It’s possible I’m being too pessimistic here. Shell stock does offer a useful and well-covered 4.5% dividend yield and I think the business is in robust health.

However, for me, Shell just isn’t cheap enough to justify a strong positive stance, especially given the macro backdrop. I think a neutral view is probably the most appropriate choice, reflecting both risks and possible reward. AMBER.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.