Good morning! And welcome to the final report before the Easter break.

1.05pm: wrapping up there, have a great Easter! Cheers.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

BHP (LON:BHP) (£87.9bn) | Record copper (1.5kt) and iron ore (192.6 Mt) production. Production guidance for both unchanged. | ||

GSK (LON:GSK) (£55.4bn) | Recommended by CDC as part of adolescent schedule. Ready for use in US from Summer 2025. | ||

Rentokil Initial (LON:RTO) (£8.4bn) | Q1 revenue $1,635m. Organic revenue growth 1.8% | ||

J Sainsbury (LON:SBRY) (£5.8bn) | FY sales (excl fuel) £26.6bn, up 4.2%, Argos FY sales £4.9bn, down (2.7)%, Fuel FY sales £4.7bn, down (8.9)%. £200m buyback | AMBER (Megan) | |

South32 (LON:S32) (£5.8bn) | Net cash up $299m to +$252m. Cannington guidance lowered 10%, other guidance unchanged. | ||

Deliveroo (LON:ROO) (£1.95bn) | Gross transaction value +9% (made up of 7% growth in the number of orders, and 2% growth average order size). Same 9% growth in both UK & International. Revenue take rate (revenue as a % of gross transaction value) fell slightly year-on-year, “due to our continued investments in the consumer value proposition” (plain English: cutting the price for their customers). FY 2025 guidance maintained. High single-digits percentage growth in GTV with adj. EBITDA £170-£190m. | AMBER/GREEN (Graham) [no section below] This IPO’d in 2021 at 390p and a £7.6bn market cap. With nearly £6bn of air having been removed from the valuation since then, perhaps this is now interesting? Results for 2024 showed net cash of £668m and that was after already spending £90m out of a £150m share buyback. The stock is categorised as a “High Flyer” and enjoys a positive trend in EPS forecasts. Normally I would demand double-digit growth from a stock trading at a very high earnings multiple (PER >20x according to Stocko and that will be on an adjusted basis). However, given its extraordinarily strong cash position for a company with a sub-£2bn market cap and its potential quality as a marketplace business (c. 27% market share I believe), I think it deserves a positive stance from us | |

Dunelm (LON:DNLM) (£1.91bn) | Sales +6.3% to £462m. On track for PBT in line. Gross margin guidance unch. at 51.5%-52%. | AMBER (Mark) | |

Man (LON:EMG) (£1.88bn) | AUM $172.6bn (Mar 2025) +2% in the quarter. Q1 net inflows $3.6bn. 14th April AUM: $167bn. | AMBER/RED (Mark) [no section below] As perhaps could have been predicted, the trend-following part of this listed hedge fund (AHL) is struggling in a whipsaw market. They say “Estimated AUM of $167.0bn and run-rate net management fees of $1,020m as at 14 April 2025” but this looks like a big gap to forecast FY25 revenues of $1.3b in the Stock Report. I'm not sure anyone really knows what the FY outcome will be in these markets. The algorithms rate this neutrally, but I think with the chance of a big miss, then I am a bit more negative than that. | |

Alphawave IP (LON:AWE) (£918m) | Bookings +34% but revenue down 4% and adj. EBITDA down 18% ($51.1m), in line. No guidance. | PINK (AMBER/RED) (Mark) [no section below] Revenue growth is impressive, but it leads to an increased operating loss. Most worryingly, they have removed all guidance due to an uncertain tariff impact. Prior to this, the market consensus was trending downwards, so this is further bad news. This doesn’t seem to have perturbed the market. Perhaps because, as far as we know, Qualcomm remain interested in buying the company. However, it seems to me that the same risks that led to the withdrawal of guidance may also lead to Qualcomm walking. The company clearly have valuable IP, it just seems impossible to value to me. | |

Ninety One (LON:N91) (£834m) | AuM £130.8bn as of March 2025 (Dec 2024: £130.2bn). | AMBER (Mark) [no section below] | |

Workspace (LON:WKP) (£819m) | Like-for-like rent per square foot up 0.9%. Occupancy down 1% to 85% (or 83% under a new calculation methodology). Net debt £820m, LTV 34%. Completed or exchanged on the sales of six properties for £52.5m in Q4. Outlook: macro events/ slower economic growth will continue to affect sentiment among some of our customers. Time needed to work through larger unit vacations already seen and expected in H1. | AMBER/GREEN (Graham) [no section below] | |

Empiric Student Property (LON:ESP) (£593m) | Completed the acquisition of Selly Oak Apartments in Birmingham for £9.0 million. Planning consent received at College House, Bristol. | ||

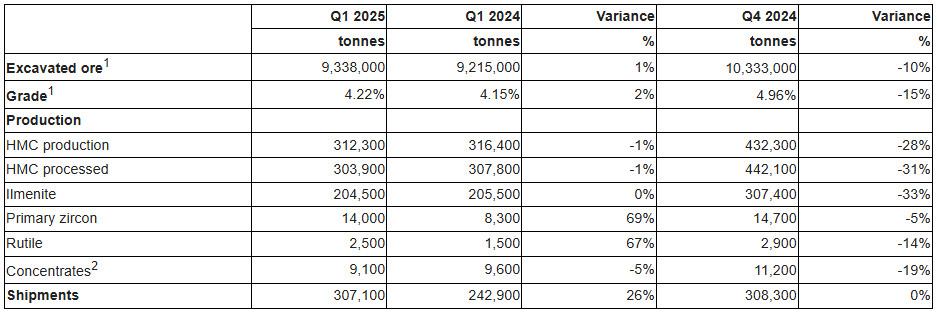

Kenmare Resources (LON:KMR) (£361m) | HMC production down 28% compared to 24Q4. Sales flat due to drawdown of stocks. On track to achieve its 2025 guidance on all metrics. | PINK (Mark) | |

Griffin Mining (LON:GFM) (£323m) | Gold production down 54% on 24Q1, Silver -39%, Zinc -43%, lead -9%, due to overhang from fatality in previous quarter, and holiday timings. |

AMBER/RED (Mark) | |

Impax Asset Management (LON:IPX) (£180m) | Investment Advisory Agreement with BNP Paribas Asset Management. Quarterly fee based on AUM. No figures given. BNP owns nearly 14% of Impax so this is technically a related party transaction. | AMBER/GREEN (Graham holds) [no section below] | |

Integrated Diagnostics Holdings (LON:IDHC) (£142m) | 39% full-year revenue growth and 115% growth in Net income. At current exchange rates, I think the net income figure translates to £14.9m. Cash balance EGP1.7bn (GBP25m). Dividend deferred to after HY Results. 2025 outlook: “we expect to see a further recovery in margins”, with a digitalisation strategy to extract cost savings. However, "in light of the current market uncertainties, the Board believes it is prudent to... defer the declaration of a dividend for the year ended 31 December 2024 until after the release of our half-year results in August. This will allow us to better assess our capital needs in light of these potential opportunities and prevailing market conditions." | AMBER/RED (Graham) [no section below] The main difficulty here is that IDHC is a foreign stock whose reporting currency is the Egyptian Pound, with 82.5% of the company's revenue derived from that country and most of the remainder being generated in Jordan. It's difficult to understand how meaningful the growth figures are in the context of Egpytian currency depreciation. Egypt has received funds from the IMF and the EU and its currency collapsed by 60% when it was allowed to float last year. Inflation was 24%. IDHC management says that 2025 is shaping up to be another successful year as they roll out new branches in strategic locations. However, given the big-picture risks which I don't think I can assess properly, I leave our moderately negative stance unchanged. Greater confidence in the Egyptian economic environment might enable a future upgrade. | |

Camellia (LON:CAM) (£114m) | MOU for the sale of Leesh River Tea Estate (via subsidiary). No figures given. | AMBER/GREEN (Mark - I hold) [No section below] | |

Iofina (LON:IOF) (£40m) | Lower than anticipated production due to low temperatures. Now expects total iodine 25H1 prodn. closer to 300MT (previous guidance 320MT-355MT). No tariff impact so far. | AMBER (Mark) | |

Rentguarantor Holdings (OFEX:RGG) (£30m) | Intention to Move to AIM (from Aquis) | Expects that admission to trading on AIM would occur this summer. | AMBER (Graham) |

RC Fornax (LON:RCFX) (£21m) | In line. Rev. £3.8m up 8%. PBT up 8% to £0.6m. on track to meet market expectations for the full year. | AMBER (Mark) [no section below] |

Graham's Section

Rentguarantor Holdings (OFEX:RGG)

Unchanged at 252p (£30m) - Intention to move to AIM - Graham - AMBER

Beggars can’t be choosers and in an environment without (many) IPOs I’m happy to see anyone joining AIM, even if it’s simply an Aquis company looking to join a bigger league.

Admittedly the financial overview contains quite a lot of red:

The company provides a rent guarantor service to “students, people who are employed, self-employed, retired or those in receipt of benefits”, who can’t get a family or friend as a guarantor.

I think they charge about one month’s rent for the service, if paid in advance, or c. 10% of the rent if paid monthly.

Checking the 2024 annual report, I see revenue growth confirmed at 72% to £1.27m. The balance sheet was slim with close to zero net tangible assets (c. £300k) and the cash position was £270k. Fresh equity was raised during the year (c. £500k).

A more recent Q1 update said that Q1 revenues were up 91.9% year-on-year, and partnership agreements had been signed with 91 introducers, including four councils. A further £455k was raised in convertible notes.

The founder, CEO and 39% shareholder is a private landlord "with a large portfolio of properties in South East England".

Graham’s view: as is my habit these days, I’m going to take a neutral stance on any new company joining AIM (even if it is merely stepping up from Aquis). I’d like to see more companies listing and so I won’t be "RED" with my initial coverage.

It’s clear that the cash position here is not all that strong vs. the losses incurred in recent years. The company has raised funds in 2023, 2024, and 2025. But none of the fundraisings has been particularly large. And at a £30m market cap, every £500k equity raise causes dilution of less than 2%. So let's hope that major dilution can be avoided here, until it reaches lift-off in terms of profitability. The headline growth rates are certainly impressive.

Mark's Section

Iofina (LON:IOF)

Down 5% to 20p - Q1 Update - Mark - AMBER

Weather-related issues mean that production is flat on the previous year for Q1:

Whilst production during the winter months has always been lower due to the colder temperatures affecting the IOsorb® process, during January and February 2025, Oklahoma experienced extremely low temperatures that affected all our partners' hydrocarbon production operations. Consequently, this led to limited brine water at times being pumped to all our plants. Since early March, the situation has been improving, with the brine water flow to our operations increasing and approaching levels experienced in Q4 2024, but it has not completely recovered to those levels.

This has led to an 11% drop in production guidance for H1 versus the midpoint of the previous range:

Given the lower-than-anticipated Q1 2025 production, the Company now expects total iodine production for H1 2025 to be closer to 300MT compared to the previously guided range of 320MT-355MT. The Company will provide a further update on Iofina Resources' production as part of its year-end 2024 financial reporting.

Here is what that production looks like in a historical context:

While it’s growing, continued issues make the actual growth in production rather pedestrian. However, pricing has remained strong:

The iodine spot price has been consistently above $70/kg in the Period, which is higher than the H2 2024 average price, and the Company expects prices to remain at these levels throughout 2025.

When I looked at the company in the DSMR in January, it had missed EBITDA forecasts due to a delay in recognising $2m of revenue. However, despite this downgrade, their broker, Canaccord, didn’t upgrade 2025:

Today, Canaccord reduce their EBITDA from $9.9m to $9.8m, saying:

We are making minor amendments to our forecasts, essentially moving 2025 volume to 745 tons (was 775) and average 2025 sales price to $68.5/kg (was $67.5). This implies 2H2025 volume of 445 tons, up 25% y/y, largely on 8 plants operating rather than 6½ (the extras being IO#10 and IO#11). The net impact is a marginal change in forecast EBITDA and earnings. If we were to assume $72/kg benchmark for the full year (+$3.5/ kg), in-line with SQM's current guidance, this would move our EBITDA up by around $1.0-1.2mn or 10-12%

So there is scope for upgrades if pricing remains strong. However, it is worth bearing in mind the FX impact here. $9.9m EBITDA in January was £7.92m, $9.8m today is £7.42m, around 6% lower, negating half of that potential commodity pricing gain. Again, this potentially includes the gain from the slippage into 2025 of $2m of revenue.

I’m also not convinced that EBITDA is a great measure for a capital-intensive business. While their processing of well byproducts means they don’t bear drilling costs, they have to build new processing plants every time they want to expand. Canaccord leave their forward EPS unchanged at 2.5c, which puts the company on a forward P/E of around 11:

Canaccord have 3.2c in for 2026, which would be a P/E of around 8. Potentially an interesting proposition if their production growth can accelerate as planned.

Mark’s View

While the issues here are largely out of their control, recent events have shown that they are not always masters of their own destiny. This means we have to take their growth plans with a pinch of salt(y brine). There is the potential for this to look cheap if they hit forecasts further out. However, it should be relatively lowly rated as any growth requires capex on new plant and machinery. It is still an AMBER for me.

Griffin Mining (LON:GFM)

Down 6% to - Q1 Production Report - Mark - AMBER/RED

Production here continues to be impacted by a mining suspension following the fatality of a Caijiaying mining contractor's employee in October 2024. Not that you’d know it from looking at the share price chart:

With mining companies, it is impossible for outside investors to judge the company’s operational effiiciency. However, the similar process controls are what delivers a strong safety record. I believe that investors absolutely should pay attention to safety figures, not just for their ESG aspect, but because they indicate important insight into operational performance. Here the company appears to be found wanting.

Instead, the rise in gold price seems to have covered a multitude of sins, as there is also the impact of holiday shutdowns this quarter:

In addition, first quarter production at the Caijiaying Mine was impacted by the Chinese Lunar New Year and Spring Festival holidays causing disruption to operations by lack of certain administrative approvals due to government department shutdowns and the travel of staff and contractors to their home Provinces, towns and villages throughout the period. The slower activity period was utilized by scheduling mine and processing plant maintenance.

The company don’t appear to have calculated the percentage impact, so I’ve added these in:

3 months to 31 March 2025 | 3 months to 31 March 2024 | Change | ||

Ore mined | Tonnes | 223,745 | 335,234 | -33% |

Ore processed | Tonnes | 241,344 | 327,529 | -26% |

Zinc in concentrate produced | Tonnes | 6,552 | 11,423 | -43% |

Gold in concentrate produced | Ozs | 2,433 | 5,270 | -54% |

Silver in concentrate produced | Ozs | 43,618 | 72,026 | -39% |

Lead in concentrate produced | Tonnes | 251 | 277 | -9% |

Average zinc price received per tonne | USD | 2,278 | 2,091 | 9% |

Average gold price received per oz | USD | 2,740 | 2,026 | 35% |

Average silver price received per oz | USD | 26.9 | 20.1 | 34% |

Average lead price received per tonne | USD | 2,634 | 2,868 | -8% |

These are pretty hefty falls in production. However, the company is guiding a return to more normal production going forwards:

Since early March, there has been an increase in ore mined, ore processed and higher ore grades such that the Company expects ore mined and processed will be able to achieve the equivalent annualised rate of 1.5 million tonnes of ore per annum in the remainder of 2025.

This should see production in line with 2023 levels, assuming similar grades. The Chairman comments:

We hope this is the last of the "black swan" events for the foreseeable future and that the Company can resume normal operations at its normalised throughput and production results.

The point of "black swan" events is that they are unforeseeable. What the events here have shown is that this isn’t a business that is particularly robust to unforeseen events. With high gold prices and production returning to normal, this is forecast to be on a forward P/E of 9:

This is expensive for the sector, though. More worryingly, the long-term chart shows a business listed since 2005, which has been in production for much of that, and hasn’t paid a dividend since 2008!

Nor have they been able to reduce their share count:

Mark’s View

This update highlights the lack of robustness of this business with significant falls in Q1 production. Strong commodity pricing and a forecast recovery in production mean that the rest of the year should be ok, which puts them on a single-digit forward P/E. However, this is actually high compared to other miners with gold and silver production. My biggest concern is that despite many years of production, they haven’t paid a dividend since 2008. All of their profits are simply reinvested into maintaining production. As such, I have to question who is really benefiting from all this activity. The algorithms rate this as a High Flyer. However, operational issues tend to be bad news for such companies, hence my AMBER/RED rating.

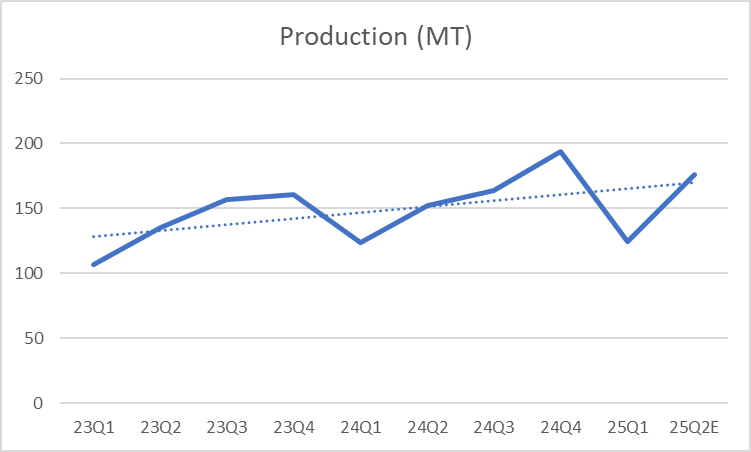

Kenmare Resources (LON:KMR)

Down 1.6% to 398p - Q1 Production Report - Mark - PINK

Given the ongoing takeover process, for which we also got a one-month PUSU extension today, the actual production results matter less. Production is flat against the previous year, but down 28% versus the previous quarter:

This is partly due to the weather, where they say:

HMC production was down 1% YoY, which was due to higher slimes impacting recoveries at WCP A and a short-term change in mining conditions at WCP B. This resulted in the excavation of oversized material, which reduced recovery of excavated ore to rougher feed. Operating time at all mining plants was also negatively impacted by adverse weather conditions, including those associated with Tropical Cyclone Jude, which limited excavated ore volumes.

This is why they can say:

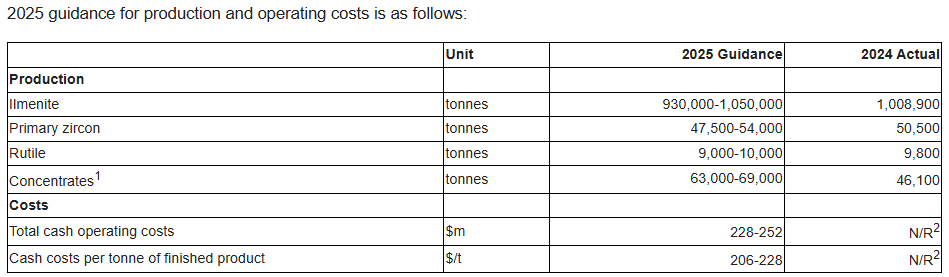

At the end of Q1, Kenmare is on track to achieve its 2025 guidance on all metrics. Ilmenite production is forecast to strengthen from Q2 onwards due to improving weather conditions following the end of the southern hemisphere rainy season.

This is what they had previously given as guidance:

Shipments are flat as they utilised stocks to meet customer demand. Pricing is largely stable, with ilmenite benefiting from strong pigment production and a thriving titanium metal market. Zircon is still suffering from weak ceramics demand, though. They summarise this as:

Kenmare has good visibility and a strong order book for its products in 2025. The market for ilmenite suitable for beneficiation remains tight, supporting demand for the Company’s ilmenite. Long-term zircon offtake agreements further support stability. While evolving global trade policies present a potential risk, titanium feedstocks and zircon appear likely to continue to benefit from exemptions due to their critical mineral status.

However, they don’t mention the potential for weaker global GDP as a result of US trade actions (in the long term, demand for Heavy Mineral Sands tends to track global GDP). Nor do they consider the impact that tariffs may have on the end products that HMS go into, such as paint or ceramics, much of which is manufactured in China for the US and European markets. So while the initial impact is muted, I do see the potential for tariffs to be broadly negative for HMS pricing.

Mark’s View

The short-term outcome for investors here is based on the likelihood of the company receiving an offer that can be recommended by the board. As such, I think the PINK rating remains the most appropriate, indicating that it is the offer, or lack of, that matters. These production numbers don’t move the needle on that either way. The tariff situation, or at least the secondary effects of it, does have the ability to derail the talks, or lead to a lower offer price. However, the long-term value of a multi-decade asset is probably not affected that much by these factors, so the acquirer may well look through these.

Dunelm (LON:DNLM)

Up 7% to 1012p - Q3 TU - Mark - AMBER

This is an impressive trading update, given the market backdrop:

Q3 sales growth is above that of H1, marking Dunelm out as a quality operator in a difficult space. They don’t give like-for-like figures. However, their store growth is modest, meaning that the LFLs are probably at most a couple of % lower than the quoted figures above. Most importantly, this growth isn’t achieved at the expense of margins:

Gross margin improved by 30bps year-on-year. We continue to exercise operational grip on input costs and with prices held broadly stable, customers continue to find great value in our ranges at all price / quality tiers. Our full-year gross margin guidance is unchanged, at between 51.5% and 52.0%.

PBT is said to be in line with analysts' forecasts, which they helpfully give as a consensus of £208m, with a range of £204m to £214m. It is worth noting that these had been trending down, though:

There also appears to be considerable caution in their outlook comments:

We are pleased that our own performance and that of the wider market has been stronger in Q3 than we saw in the first half, however it is too early to say whether or not we are seeing an improved trend. We are also mindful of increased levels of uncertainty and volatility in the current environment, and the known labour cost headwinds.

This is why the forecast sales growth in FY26 only turns into a 5% increase in EPS. The algorithms are neutral on the stock at the moment:

If Q3 is the start of a new sales trend and they can offset labour cost increases then this may yet become a High Flyer or even a Super Stock. However, of the current value metrics, only the dividend yield is rated green:

Mark’s View

I really like this company. Their ability to generate very good returns on capital marks them out as an excellent operator:

However, they simply haven’t been able to deploy capital to grow their EPS, which is the only thing that really matters, at the end of the day:

That this is largely the macro environment means that they are doing little wrong internally. However, that this isn’t their fault doesn’t mitigate that it is the reality they face. Their outlook statement gives little confidence that this is going to change anytime soon. As such, I’m going to stick with the algos and give this a neutral rating. AMBER

Megan's section

J Sainsbury (LON:SBRY)

Up 2.5% to 254p (£5.96bn) - Final results - Megan - AMBER

Sainsbury’s final results for the year to February 2025 are interesting off the back of numbers from Tesco last week.

While Simon Roberts has this morning set a positive tone for Sainsbury’s outlook, Tesco’s boss, warned of fiercer competition and the potential fallout that could have on pricing. Perhaps this positive momentum from Sainsbury’s is what the larger supermarket group is referring to. Sainsbury’s has this morning said that it is making bigger strides to take market share that at any point in the last decade. It’s winning more customers buying ‘big baskets’ worth of groceries and recently acquired 14 new supermarkets at strategic locations.

It’s worth being slightly wary of the company’s positive comments on market share. Market research group Kantar Media has put Sainsbury’s market share around 15% for most of the last five years and there have been surges in momentum before, which have never managed to take a meaningful chunk out of the position of Tesco.

Plus, the ‘widening market share’ narrative isn’t quite translating into further sales acceleration. In FY2024, like-for-like sales growth averaged 9%, peaking in the first quarter at the 11% mark. In FY2025, like-for-like sales growth averaged 4.2% and 4.5% for groceries alone.

Grocery sales were £24.7m, compared to £23.6m last year, which management says was largely driven by volume rather than price. The breakdown of the impact of price and volume on overall sales isn’t given, but the company is seeing increased uptake of the Nectar card, which (like Tesco’s clubcard) offers discounts and rewards customer loyalty. It’s a scheme which has worked wonders at Tesco and it’s encouraging to see similar results starting to bear fruit at Sainsbury.

Financially, the company has reported a slight recovery in margins thanks to its major ‘Retail Restructuring Programme’ which has been ongoing since 2020. Underlying operating margins were 3.17% compared to 3.01% last year, which is still a little short of the margins boasted by Tesco, but a positive step in the right direction. In addition to its long term restructuring plans, the company also initiated a ‘Next Level Sainsbury’s’ strategy last year, which seems to revolve around staff streamlining (redundancies) plus the closure of less profitable retail locations.

Working capital ticked down slightly in the year, which had a knock-on effect in the company’s cash inflows, but on an underlying basis operating cash inflows benefitted from higher profits. The company has also increased its capital expenditure, which is encouraging.

Megan’s view:

There is no escaping the fact that as a retailer and an investment, Sainsbury’s has been the inferior choice to Tesco in the last decade. Unless you’re looking for income.

The company’s dividend (which was cut and rebased during the Covid-dividend rout of 2020) is now well covered by free cash flow and just covered by earnings. The yield of just over 5% is pretty attractive and looks sustainable.

But share price appreciation? I’m not confident. The strategy seems sensible, but management is taking a long time to kick the recovery fully into gear (probably because it’s trying to oversee two massive strategic overhauls at the same time and is getting distracted). A price to earnings ratio isn’t quite cheap enough for what’s on offer here, especially given the value elsewhere in the UK. Tesco remains my pick of the supermarkets and I’m neutral on Sainsbury’s.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.