Good morning and welcome back! I hope everyone is feeling refreshed after the break.

The FTSE continues its post-tariff recovery, scheduled to open up 0.7% this morning around 8250.

12:30pm: that will do it for today, a pleasant start to the week if not for the Argentex fiasco!

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

DCC (LON:DCC) (£4.9bn) | Sold for £1,050m, 12x adj op profit. Expect net cash proceeds of £945m, inc defcon. “Significant return of capital” to shareholders planned post completion (Q3). | GREEN (Roland - I hold) Today’s disposal looks reasonably priced to me, even if it’s not a blockbuster valuation. Personally, I’m happy to see DCC focusing on its much larger and more profitable Energy division. With the stock trading on c.10x earnings, I remain positive. | |

ITM Power (LON:ITM) (£178m) |

Revenue now expected to be £25.6-26.5m, 30% ahead of previous guidance of £18-22m. Net cash £204-205m (£185-195m previously). FY25 EBITDA loss exp unchanged at £32-36m. | AMBER/RED (Roland) [no section below] This hydrogen electrolyser company went through a spectacular hype cycle during the pandemic, before crashing back to earth when investors remembered that revenue was minimal and profits were negative. The potential appeal here is that the shares are trading below net cash. However, I think the risk is that ITM has massively overinvested in capacity and could still run short of cash again – recent broker coverage projects losses out to at least FY27 and predicts expected FY27 factory utilisation of just 6%. | |

City of London Investment (LON:CLIG) (£176m) | FUM unchanged at $9.9bn as net outflows of $212m were offset by market gains of $218m. FUM $9.95bn at the end of March. Emerging markets strategies represent ⅓ of FUM with presumably high tariff exposure, e.g. CLIG’s funds are the largest shareholder in Templeton Emerging Markets Investment Trust (LON:TEM). FUM as of 15 April is c. $9.7bn, where the fall is presumably a combination of further outflows and market falls. | AMBER/GREEN (Graham) [no section below] This one was covered by Roland in January and by Mark in February. Today’s update shows continued quarterly net outflows but at a slower pace than that seen in Q2 ($369m), and only slightly higher than Q1 ($195m). There has been another c. $200m fall in FUM since the end of March. Despite tariff exposure at CLIG’s funds, I continue to see value in these shares with a PER of c. 10x and a dividend yield c. 10%. The company is transparently trying to increase its dividend cover and so for income seekers, I think this stock could remain interesting. Modest outflows can be offset by market returns and at the current rate of outflows, the company can stand still instead of shrinking further. | |

Ricardo (LON:RCDO) (£141m) | FY25 trading “within the range” of analyst expectations despite recent order volatility. 91% of net revenue for the year has been secured, which is actually up on last year. £5m of cost savings will “largely offset” the expected market turbulence this year and net debt would be below expectations if not for the planned restructuring costs. Then an incremental £10m of cost savings will be delivered in FY26. Finally, Ricardo criticises Science Group’s track record in M&A, arguing that previous takeovers were on unattractive terms for those companies’ shareholders. | AMBER/RED (Graham) [no section below] | |

Aoti (LON:AOTI) (£88m) | Topical Wound Oxygen therapy included in NHS Advanced Wound Care 2025 framework. Management says a recent trial has shown this treatment lowers diabetic foot care costs by 16% to c.£26k over a two-year period. | AMBER (Roland) [no section below] | |

Celebrus Technologies (LON:CLBS) (£83m) | FY25 rev to be below exp at c.$38.6m. Adj PBT ahead at $8.7m, due higher margin sales. Net cash expected to be around $31m at year end. | AMBER/RED (Roland) Today’s update has rightly been given a poor reception by the market, in my view. The company has combined a revenue warning with news of a significant (adverse) change to its relationship with a major client. At the same time, big changes to revenue recognition have been announced. The end result is that the outlook is completely unclear and FY26 guidance has been withdrawn. Net cash provides some protection and the core business may still be attractive. But there’s no visibility for investors, hence my mildly negative view. | |

Videndum (LON:VID) (£70m) | FY24 results to be in line. Discussions “progressing positively” with lenders to reset covenants. Work on refinancing is also underway. | RED (Roland) [no section below] Some small comfort today as VID says it expects to reach agreement with its lenders to reset its banking covenants. However, we don’t know what the amended terms might be on the company’s debt facilities. With FY25 forecasts suggesting minimal profitability, the existing equity remains at risk of dilution, in my view. | |

| Argentex (LON:AGFX) (£52m) | Financial Position & Suspension of Trading | FX volatility has impacted liquidity. Margin calls on forwards/options. Material uncertainty. Suspended. | BLACK (RED) (Graham) It's an automatic RED from me until this situation is resolved. Shocking news as the company gets into liquidity difficulties despite having a cash balance that appeared adequate a few months ago, and strong assurances around the company's management of market risk and liquidity risk. |

Riverstone Credit Opportunities Income (LON:RCOI) (£37m) | NAVps -$0.04 to $0.88. Dividend “nominal” but exp $16-17m return when H&W payment received. | ||

Ebiquity (LON:EBQ) (£33m) | 2024 rev -4.3%, adj PBT -33% to £6.5m. Encouraging Q1 trading. FY25 remains in line with exps. | ||

Shield Therapeutics (LON:STX) (£24m) | Initial payment $665k. Milestone payments on reg approval and sales targets, and royalties. | ||

Braime (LON:BMTO) (£22m) | Revenue £48.9m, PBT £3.2m (2023: £3.3m). “Relatively strong position”, but outlook uncertain. | ||

Arecor Therapeutics (LON:AREC) (£14m) | Revenue £5.1m, loss after tax £10.2m, cash £3.3m. Material uncertainty re: going concern. | RED (Graham) [no section below] |

Graham's Section

Argentex (LON:AGFX)

Shares suspended at 42.68p (£51m) - Financial Position & Suspension of Trading - Graham - BLACK (RED)

This is a shocking announcement:

…Argentex has been exposed to significant volatility in foreign exchange rates, particularly in relation to the rapid devaluing of the US Dollar against other major benchmark currencies which has been precipitated by the various recent announcements from President Trump regarding tariff policies and US government spending cuts…

As a result, the Company has experienced a rapid and significant impact on its near term liquidity position, driven by, inter alia, margin calls linked to its FX forward and options books. The Company has taken a number of steps to preserve cash and increase the collateral received from its counterparties. In addition, the Company is considering a number of options for the business…. In the event that the volatility in currency markets worsens materially then the Company's financial liquidity position, if not strengthened in the near term, would be significantly stretched.

AGFX shares are suspended “in light of these developments and the current material uncertainty”.

Graham’s view

I was AMBER/GREEN on this back in January noting that the balance sheet had a tangible value of £40m, backing up a large chunk of the market cap.

I would have been AMBER if I was valuing it purely on earnings, but with that balance sheet strength (or so I thought), I was happy to take a moderately positive view.

Mark was AMBER in April when the full-year results came through with a small operating loss (previous year: operating profit £8m) despite £4m of EBITDA (previous year: £12m of EBITDA).

Checking the full-year results for clues as to what happened, there is a section on “Financial Risk Management Objectives”. Let’s see what the company was previously saying about the risks it faced:

Market Risk

Market risk for the Group comprises foreign exchange risk and interest rate risk. Foreign exchange risk arises from the exposure to changes in foreign exchange spot and forward prices and volatilities of foreign exchange rates.

Foreign exchange risk is mitigated through the matching of foreign currency assets and liabilities between clients and institutional counterparties which move in parity. The Group maintains non-sterling currency balances with institutional counterparties only to the extent necessary to meet its immediate obligations with those institutional counterparties.

It is clear that Argentex should not have any long position in USD forwards or options that is not offset by a corresponding short position held by its clients, i.e. that any exposures are eliminated by the "matching" of opposite positions. The company itself is not supposed to be speculating on currency movements. And for now I don’t have any reason to suspect that has happened here.

But moving on the next major risk:

Liquidity Risk

Liquidity risk is the risk that the Group will not be able to meet its financial obligations as they fall due. The Group has extensive controls to ensure that is (sic) has sufficient cash or working capital to meet the cash requirements of the Group in order to mitigate this risk. The Group monitors its liquidity requirement daily, and the Group stress tests its liquidity position to review the sufficiency of its liquidity in stressed market scenarios.

That sounds fine but in reality, I think it’s fair to say that liquidity risk has not been adequately managed.

The company’s net cash position - £18m as of Dec 2024, with £6m being collateral held at counterparties - looked adequate a few months ago. But in hindsight, not so much.

The 2024 full-year results disclosed that the total value of the derivatives on AGFX’s books was nearly £3 billion, with roughly the same amount being assets and a matching amount in the form of liabilities.

If AGFX’s institutional counterparties have demanded a slightly higher margin on those derivatives, I suppose it’s not hard to imagine how £18m could quickly be used up in providing that margin.

There’s also the potential for credit risk with clients who don’t post margin in a timely manner if their positions have moved against them. The company says it "is trying to increase the collateral received from its counterparties", and this may be the biggest problem the company faces.

I’m going to have to switch to RED here immediately, as it appears that financial risk management has been below par and that the company’s cash resources are either already insufficient, or are close to insufficient, for the positions it has taken on behalf of its clients.

The best-case scenario is that volatility calms down, margin calls can be met, and margin requirements are then relaxed before too long. We go back to business as usual, with the company having learned something about the risks it’s carrying.

A more realistic scenario might be that the company raises some fresh equity to cover any potential gap between its cash resources and what it needs to maintain its positions.

A bearish scenario would be that it cannot raise enough equity to do this.

As there is a “material uncertainty”, it’s an automatic RED from me for now. Let’s hope we get a positive resolution soon. It's another nasty reminder of the risks that can lurk below the surface of financial companies.

Roland's Section

DCC (LON:DCC)

-4.5% to 4.756p (£4.7bn) - Disposal of DCC Healthcare - Roland - GREEN

At the time of publication, Roland has a long position in DCC.

Sale of DCC Healthcare at a total enterprise value of £1,050 million

In November last year, Irish distribution group DCC set out plans to focus its operations on its core Energy business. As part of this, the company said it planned to sell DCC Healthcare in 2025, with a later disposal planned for its Technology distribution business.

Today’s update appears to mark the completion of the first stage of this process. DCC has agreed to sell its Healthcare business to European private equity group Investindustrial on the following terms:

Enterprise value: £1,050m

Total expected net cash proceeds of c.£945m, including unconditional deferred payment of £130m within two years

Sale price represents a multiple of c.12x 2024 adjusted operating profit

DCC expects “a significant return of capital to shareholders post completion”

The business being sold includes both a manufacturing and distribution element. Healthcare generated 13% of DCC’s group operating profit last year, with a return on capital employed of 10.2%.

Given this rather average level of profitability, the sale multiple of 1.4x book value (c.£765m) seems fair to me. However, the Healthcare business has been more profitable than this at times in the past. Depending on the outlook for Healthcare, the sale valuation is arguably not too demanding.

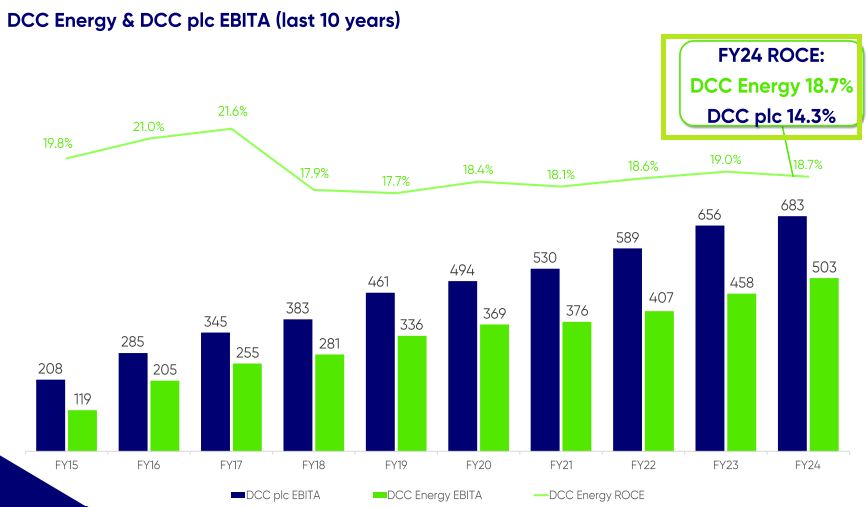

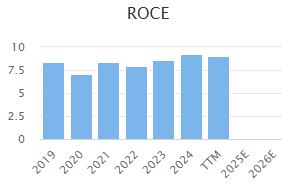

What’s left for shareholders? DCC’s Energy division generates about 75% of the group’s operating profit and is more profitable than its other units. Based on the company’s own calculations, Energy generated ROCE of 18.7% last year, versus 14.3% for the whole group.

The energy business has two main elements:

supplying petroleum-based fuels (liquid and gas) to industrial, commercial and residential customers

Supplying energy services to business customers, including renewable solutions

Organic growth has been supplemented with bolt-on acquisitions over many years, and this model continues. In my view, DCC has a strong record as a consolidator.

This chart illustrates why DCC believes it can become a more profitable (and valuable) group by focusing on Energy alone:

Roland’s view

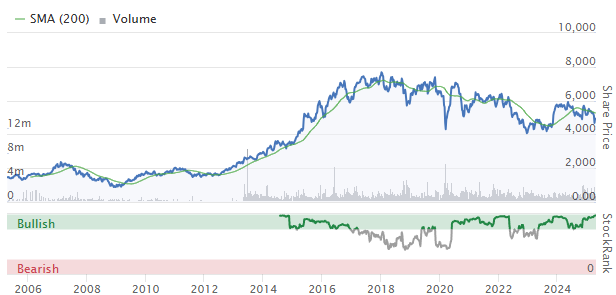

DCC’s growth has slowed in recent years, due to a variety of factors. This has been reflected in a significant de-rating of its shares:

As a shareholder, I don’t think there’s anything fundamentally wrong with the business and am encouraged by DCC’s plan to focus solely on Energy.

Aside from the superior financial performance and scale of the Energy business, I think a more focused group makes sense. The Healthcare and Technology divisions do not have any obvious overlap with Energy. Removing them should help management to focus more carefully on the group’s most valuable business.

In terms of valuation, the Energy business generated an adjusted operating profit of around £515m over the 12 months to 30 Sept 24, giving the shares an EBIT/EV yield of 8%.

Adjusting DCC’s enterprise value for today’s disposal implies an EBIT/EV yield of 9.5% – good value, in my view.

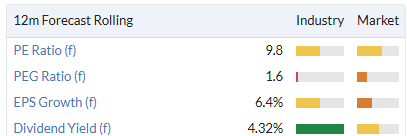

Prior to today, forecast multiples for the whole group (including Healthcare) did not look too demanding:

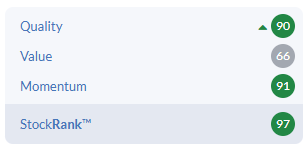

The StockRanks also have a positive view, with Super Stock styling and strong factor scores:

Perhaps my main concern with this business is that overall profitability has been fairly average in recent years, when calculated on a statutory basis. The high-teens ROCE figure provided by the company relies on an in-house calculation that’s reasonable, in my view, but flatters by excluding various factors:

When DCC’s operations are narrowed down to Energy alone, I would expect this ROCE figure to improve. This is one reason why I remain happy to hold despite this apparent average profitability.

The Healthcare sale is expected to complete in the third quarter, following which DCC is planning a “significant” shareholder return. No information has been provided on this yet, but it seems plausible to me to suggest that the company could return c.10% of its current market cap (i.e. around £490m).

The market seems underwhelmed by today’s news, but I don’t see too much to dislike. My positive view on DCC remains unchanged. GREEN.

Celebrus Technologies (LON:CLBS)

Down 19% to 170p (£68m) - Trading update & accounting policy - Roland - AMBER/RED

Celebrus Technologies plc (AIM: CLBS, the "Group", "Celebrus"), the AIM-listed data solutions provider, provides the following trading update for the year to 31 March 2025 ("FY2025").

The market has taken a dim view of today’s update from Celebrus Technologies. Reading through it, my impression is that it’s one of those onion-like updates that contains several layers of (mostly bad) news.

Let’s take a look at the main points, as I’ve understood them.

FY25 trading update: the company is suffering the consequences of global geopolitics, presumably referring to the USA:

As previously reported, there was some slowing down of customer decision making in the second half of our financial year reflecting the increasingly uncertain global geopolitical situation.

Revenue for the year to 31 March is expected to be below expectations, at c.$38.6m.

However, cost control and a higher-margin mix of software sales means that adjusted pre-tax profit is now expected to be $8.7m, slightly ahead of broker Cavendish’s estimate of $8.5m

Year-end net cash is expected to be around $31m – more than a quarter of the market cap prior to today’s fall.

Accounting policy change: Celebrus is planning to change the structure of its contracts, leading to a change in revenue recognition policy. In essence, the company is moving from recognising the whole value of a contract upfront to monthly recognition through the life of a contract.

This will result in a change to the company’s Annual Recurring Revenue (ARR) calculation.

The Board believes that the redefinition of ARR gives investors a more meaningful view of the most valuable and significant part of the Group, and its growth trajectory, and that monthly software license revenue recognition will remove a seasonal pattern from the Group's results, in which first half revenues are much lower than second half revenues

Restated for these changes, Celebrus’s annual recurring revenue rose by 13.9% to $18.8 million last year (31 March 2024 restated: $16.5 million). That seems a respectable growth rate.

Impact & Outlook: Celebrus’s management have also slipped in some bad news, which I’d argue has been partly concealed in a discussion of the changes to accounting policy (my emphasis):

In addition to the changes outlined above, and in particular the move to monthly software license recognition, FY2026 will also be impacted by the restructuring of a longstanding agreement with a large, partner-led, on-premises customer. As a result of this restructuring, the Group will move away from reselling non-Celebrus software to support the client environment (the Celebrus product forms only a small proportion of annual revenue for this client). The Board believes that the change is likely to result in lower non-Celebrus revenue in FY2026 and is in line with the increased focus on higher quality Celebrus software revenue.

It’s not entirely clear to me, but my reading of the statement above is that overall group revenue could be significantly lower next year, even before the change in revenue recognition.

Planned accounting changes seem likely to exaggerate this drop, in my view.

The FY25 ARR figure provided today of $18.8m is roughly half today’s FY25 revenue guidance of $38.6m.

If non-Celebrus revenue is falling and the company starts recognising revenue from multi-year contracts on a monthly basis, then I think there’s a chance near-term revenue expectations could fall very sharply as these changes work through the accounts over the next few years.

Management say they haven’t yet worked out the implications on revenue of the accounting changes client restructuring announced today. This doesn’t seem entirely reassuring to me:

The combined impact of these various factors on Group revenues for FY2026 and beyond is still to be determined. More details will be provided with the Group's full year results, due to be published on 8 July 2025.

Brokers Canaccord Genuity and Cavendish have both withdrawn their FY26/FY27 forecasts today and placed their ratings under review.

Roland’s view

Celebrus has gone from a High Flyer in November to a Falling Star today.

This transition has been accompanied by a sharp share price de-rating – the stock is now back where it was two years ago:

As we saw in a different context with Bunzl last week, today’s sharp drop was preceded by a sharp fall in StockRank after December’s interim results triggered a fall in momentum.

While the stock’s Quality and Value Ranks are largely unchanged from December, the stock’s MomentumRank has fallen rapidly since its results were published:

27 Dec 24: 90/100

7 Feb 25: 63/100

22 Apr 25 (prior to market open): 28/100

With hindsight, it looks like the switch from High Flyer to Falling Star could have been a sell signal, at least for traders and momentum investors.

We’re hoping to do some more research into this in the coming weeks – look out for a standalone article on this topic.

Today’s update does not fill me with confidence. The combination of accounting changes and (seemingly) adverse trading news means that I can’t see any way to sensibly predict the company’s financial performance next year.

In isolation, I think a shift from upfront revenue recognition to monthly revenue recognition should eventually come out in the wash. Given the growth of the company’s cloud-based services, this change doesn’t seem unreasonable. Over time, I think it’s fair to suggest it could lead to more predictable, higher-margin revenues.

However, the fact that Celebrus has chosen to announce these accounting changes at the same time as a change to its trading relationship with a major client gives me pause for thought.

I can’t help wondering if today’s changes may partly have been prompted by the client restructuring, as a means of trying to reframe an expected fall in revenue.

Celebrus’s $31m net cash position should provide a comfortable safety margin. But given the lack of forward guidance, I think it makes sense to take a moderately negative view here to reflect the lack of visibility on sales and valuation. AMBER/RED.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.