Good morning!

Today's Agenda is complete with post-7am stragglers now added. Spreadsheet accompanying this report: link.

The report is now finished.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our View (Author) |

|---|---|---|---|

Standard Chartered (LON:STAN) (£41bn | SR92) | SP -2% Underlying return on tangible equity of 14.7%, exceeding three-year plan a full year early. Operating income up 6%. Full year dividend per share up by 65%. New $1.5 billion share buyback. Guidance: Reported operating income growth year-on-year to be around the bottom end of 5-7 per cent range at constant currency. ROTE to be >12%. | BLACK (guidance at bottom end of range) | |

| Greatland Resources (LON:GGP) (£4.7bn | SR65) | Half-year financial results (published 23/2 am) | H1 revenue of AU$977.3m with net profit of AU$342.9m. Net tangible assets per share up 24% to AU$2.47, net cash of AU$948m. Gold production of 167koz with an AISC of AU$2,176/oz. In line with guidance for FY26 production of 260-310koz. | AMBER (Roland) [no section below] Greatland has rapidly stabilised and extended the life-of-mine plan for Telfer to help bridge the gap while the Havieron mine is developed. According to broker Canaccord, Telfer is now expected to produce for 2-3 more years – and further extension opportunities may arise. Even so, the latest forecasts I can see from Canaccord (Jul ‘25) suggest production will peak in FY26 before falling somewhat over the next 2-3 years. With the stock already trading on 24x FY26 and 42x FY27 consensus earnings (per the StockReport), this situation strikes me as a little riskier than some other gold miners. While I don’t have any reason to doubt the company’s expectations for Telfer and Havieron, any weakness in the gold price could combine with lower production to cause a sharp decline in profits over the next couple of years. |

ConvaTec (LON:CTEC) (£4.4bn | SR36) | SP +12% Revenue +6.5%. Adjusted operating profit +10.2%, actual operating profit down 2.7%. Adjusted EPS +16%, actual EPS down 7.1%. FY26 outlook: “another year of double-digit EPS growth”, which is unchanged. Medium-term organic revenue growth target from 2027 increased to 6-8% (previously 5-7%). | AMBER/GREEN (Graham) [no section below] This is a "global medical products and technologies company". Today's results have been well-received thanks to the upgrade of the medium-term organic growth target (from 5-7% to 6-8%), along with an expectation of "sustainable double-digit adjusted annual EPS growth". For companies of this size, even modest increases to the growth outlook are meaningful. This year's statutory results include the $72m impairment of an intangible asset and the market is clearly willing to look past that. The leverage multiple of 2x is "in line with target" and is at a level which investors can often accept for large, predictable businesses. Convatec's profits have grown impressively during its life as a listed entity, and its earnings forecasts have been stable or even gently rising. It has "leading market positions in advanced wound care, ostomy care, continence & critical care, and infusion care", which are all areas with high and broad demand. Overall, I'm satisfied to take a moderately positive stance on this. ROE has been running at double digits for the past few years, and again in FY25, and the shares trade at about 17x earnings (on conversion from dollars to GBP). | |

Croda International (LON:CRDA) (£4.2bn | SR81) | Sales +6.6% (cc). Adjusted operating profit +7.9% (cc). Actual operating profit more than halves due to various adjustments including impairments. 2026 outlook: organic sales growth within 3-6% range. Adjusted operating profit in line with current market expectations at constant currency. | ||

Balfour Beatty (LON:BBY) (£3.8bn | SR72) | CFO will step down from the Board later this year. Group Financial Controller at BAE Systems has been appointed to succeed him. | ||

Unite (LON:UTG) (£3.1bn | SR55) | Results for the year ended 31 Dec 2025 & Disposal of £186m asset to USAF | “Robust” performance: “strong trading across the majority of our portfolio offset by weaker demand in a small number of cities”. Adjusted earnings +9%, adjusted EPS +2% (47.5p). Actual EPS down 79%. EPRA net tangible assets down 2% to 955p. Guidance: 2026/27 income expected at lower end of range for 2-3% rental growth and 93-96% occupancy. Empirc’s income below expectations ahead of integration. Adjusted EPS guidance 41.5p-43p. | |

| Georgia Capital (LON:CGEO) (£1.17bn | SR87) | Final Results | NAV per share +14.1% in Q4 and +61.2% in FY25. FY25 Revenue +9.8% to GEL625m with EBITDA +19.3% to GEL89m. New $50m buyback. | |

Oxford BioMedica (LON:OXB) (£936m | SR29) | 2025 revenues + c.30%, at the upper end of guidance. Underlying operating EBITDA “low single-digit £ million”, in line with guidance. Net cash £55m. Expectations for 2026 unchanged and guidance reiterated. Revenues to grow 25-30% year-on-year, operating EBITDA margin to exceed 10% in FY26 and be at least 20% for FY27. | ||

| Sylvania Platinum (LON:SLP) (£312m | SR88) | Interim Financial Results | Revenue +110% to $99.8m due to 25% increase in PGM production and 55% increase in basket price. Net profit of $23.2m (H1 25: $7.2m). Outlook unchanged from 27 Jan 26 update. | AMBER/GREEN = (Roland) [no section below] Today’s results contain few surprises as many of these numbers were included in January’s Q2 update, which I covered here. Although there’s clearly some commodity price risk (platinum prices have doubled over the last year), I am comfortable remaining broadly positive on Sylvania as I think the valuation reflects this risk to a greater extent than with many gold stocks currently (where I am typically neutral). A forward P/E of 5 and 1.6x price/book multiple are not unreasonable at this point, in my view and are fairly reflected in the StockRanks’ High Flyer styling. |

| McBride (LON:MCB) (£296m | SR94) | Interim results for 6M ended 31 December 2025 | H1 revenue down 2.1%, adjusted operating profit down 1.7% (£31.5m). On track for full-year targets. H2 started in line with expectations. Good momentum expected as a healthy pipeline of contract wins are set to launch. Consensus expectations: adjusted operating profit £64.7m. | AMBER = (Roland) These results don’t look too alarming, but sales growth is minimal and there seems to have been further pressure on margins. Debt levels are also a little higher than I’d like for a negative working capital model. Forecasts imply a modest H2 weighting that doesn’t seem too challenging, but I’d like to see stronger evidence of a return to sales growth before turning more positive. As things stand, I think the shares may be fairly priced, or perhaps only slightly cheap. |

Brooks Macdonald (LON:BRK) (£265m | SR58) | FUMA +5% to £20.1bn with FUM of £17.8bn. Net inflows of £2m. Revenue +12% to £58.2m, adj pre-tax profit -12% to £13.6m due to 20% rise in operating costs. Expect FY25 performance to be in line with market expectations. | ||

Avacta (LON:AVCT) (£249m | SR21) | New data demonstrates “favourable delivery profile” of proprietary pre|CISION platform compared to marketed antibody drug conjugate (ADC) for certain cancer treatments. | ||

B.P. Marsh & Partners (LON:BPM) (£241m | SR85) | Eight new investments completed in y/e 31 Jan 26. Two disposals, generating £30.7m of proceeds from £1.9m invested. “Robust pipeline of new opportunities”. Group funds of £49.5m at 31 Jan, intend to pay £13m of dividends in FY27 and minimum of £5m in FY28. | GREEN = (Graham) | |

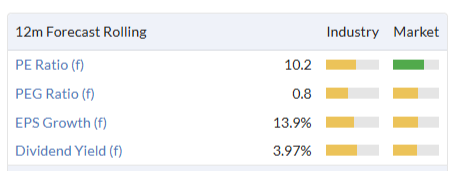

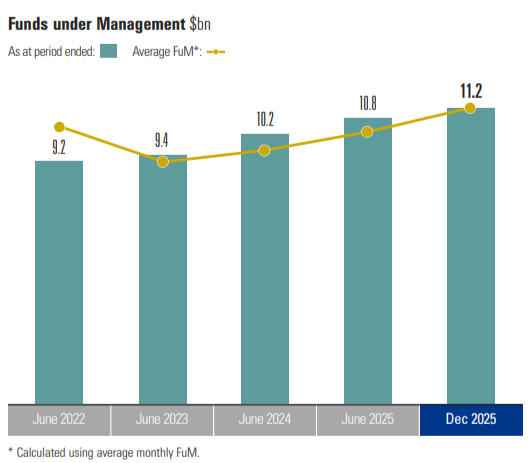

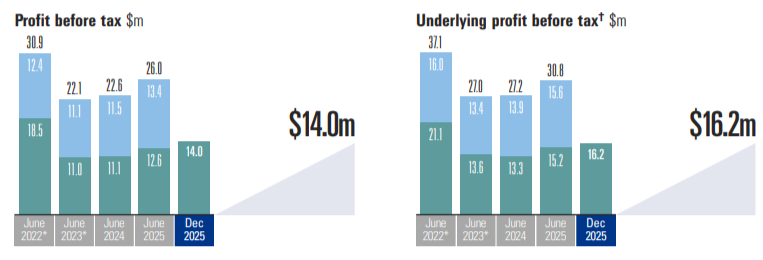

City of London Investment (LON:CLIG) (£195m | SR95) | FUM +3.7% to $11.2bn at 31 Dec 25. FUM on 18 Feb of $11.9bn. H1 net fee income +5.7% to $37.3m, adj pre-tax profit +6.6% to $16.2m. Dividend held at 11p per share. | AMBER/GREEN = (Roland - I hold) Today’s results strike (almost) all the right notes, showing strong investment performance and a useful increase in profits. The missing ingredient is net inflows – investor cash continued to flow out of the business during the half year, despite some very strong investment returns from CLIG specialist strategies. I am hopeful that the combination of new management and more favourable market conditions will help to reverse this long-running negative trend, but I have to recognise the risk that things may not improve – active fund managers remain under pressure. Support for the 8% dividend yield has improved with today’s upgrade and I remain happy to hold, but I’m going to leave our recent AMBER/GREEN view unchanged today. | |

BTG Consulting (LON:BTG) (£190m | SR82) (formerly Begbies Traynor) | Full year expectations unchanged (consensus: PBT of £23.7m-£25.4m). Positive levels of new instructions in restructuring and an increase in financial advisory transactions. Real estate “in line with expectations”. | AMBER/GREEN = (Graham) barring any further M&A, growth is expected to continue at a moderate pace with mid-single digit organic growth. If the balance sheet was stuffed with cash, then perhaps I could take a more positive point of view. But there isn't any significant amount of net cash to speak of. Net debt was £6m as of October 2025. I therefore view our existing AMBER/GREEN position as fair. | |

Smarter Web (LON:SWC) (SR21) | $30m facility secured against Bitcoin held within Coinbase. Will allow SWC to deploy capital into Bitcoin immediately following new equity issues, without “settlement-related timing risk”. | ||

Ten Lifestyle (LON:TENG) (£66m | SR72) | New multi-year contract with “a leading financial services provider within the AMEA region”. Expected to be a large contract (£2-5m annualised revenue from FY27). | ||

Tpximpact Holdings (LON:TPX) (£36m | SR94) | “Strong trading in Q3 and continued momentum during Q4”. New business secured for the year to date now exceeds £110m. Upgrading outlook for y/e 31 March 2026. Adj EBITDA now to be not less than £7m (prev. £6-7m), net debt to be below £6m with leverage reduced to c.0.85x EBITDA. | ||

Fiinu (LON:BANK) (£33m | SR3) | Plugin Overdraft product is undergoing testing with Conister Bank and is now expected to launch in Q2 2026 (previously Q1). | ||

One Health (LON:OHGR) (£32m | SR67) | Planning sign off for Surgical Hub in Scunthorpe has been completed and construction will start imminently. The Board remains confident the project can be delivered within one year and within the previous £8-9m cost estimate. | ||

IMC Exploration (LON:IMC) (£13m | SR9) | A laboratory study of 2024 drilling at the Boley prospect shows the drillhole intersected “free gold in quartz veins”, with 1m at 5.8g/t Au and 1m at 1.1g/t Au. | ||

essensys (LON:ESYS) (£12m | SR19) | SP -8% to 16.5p | PINK (Graham) [no section below] | |

RC Fornax (LON:RCFX) (£10m | SR43) | Revenue -36% to £4.1m, adjusted loss before tax of £1.6m (FY24: £0.5m profit). Raised £2.1m in December. £4.3m of new orders/extensions booked in H1 FY26. Current visibility over £4.5m of sales for FY26. | [Roland] Issuing results almost six months after the year end is a warning flag. |

Graham's Section

B.P. Marsh & Partners (LON:BPM)

Up 2% to 682p (£247m) - Trading Update - Graham - GREEN =

B.P. Marsh & Partners Plc (AIM: BPM), the specialist venture capital investor in early-stage financial services businesses, provides an update on trading for the Group's financial year ended 31 January 2026.

This investment business continues to busily deploy its large cash balance, although its cash balance remains stubbornly high.

Key points from today’s update for FY January 2026:

8 new investments during the year

Two disposals generated £30.7m upfront proceeds from £1.9m of invested capital

“Robust pipeline of new opportunities”

I did wonder if BPM might be getting so large and successful that it might start to struggle to find new investments that could move the needle. So far at least, that doesn’t appear to be the case:

The Group is currently assessing nine prospective opportunities, each aligned with B.P. Marsh's disciplined investment strategy and long-standing focus on insurance and broader financial intermediary businesses.

Cash of £49.5m as of January 2026, down from £74m (January 2025).

Besides disposals, some of the key factors affecting cash during the year were:

£37.8m of new equity investments

The loan portfolio increased from c. £28m to c. £41m.

£8m of total dividends, £1.9m of buybacks.

A total of £13m of dividends are expected in FY January 2027, but beware that £10.5m of these are being paid early in the year, with £2.5m already due to be paid with the shares having been marked ex-dividend. A further £8m will be going ex-dividend soon (I think on 5th March.)

New investments: the max size of a new equity investment was £10m. There were also individual loan agreements of up to £10m.

Market outlook

BPM remains very much focused on its sector niche. What I’m taking away from its market commentary today is that while insurance pricing pressures are downward, this isn’t going to affect BPM’s investees too much:

While capacity remains abundant and the sector continues to attract institutional capital, overall profitability within insurance distribution remains broadly stable, especially within the more specialist segments in which the Group invests.

The fee- and commission-based revenue of brokers and MGAs provide a degree of insulation from rating pressures. In addition, rate volatility in specialist risk segments, where many of the Group's portfolio companies operate, has typically been more moderate. The Board, therefore, remains confident in the resilience of underlying revenue generation.

Graham’s view

I’ve been something of a cheerleader for this stock over the years, and even added it to my 2026 watchlist (a list that’s not very easy to get onto!).

After today’s update, I see no reason to change stance.

The July 2025 NAV was £349.5m with only a £2.5m reduction needed for dividend payments since then (the dividend that is due on Friday of this week).

With a discount to NAV approaching 30%, it’s little wonder that BPM continues to slowly buy back its own shares.

Brian Marsh OBE has stepped back to the role of Non-Exec Chair but the new execs have been with the company for many, many years and I expect they will continue to do well. So I’m staying GREEN on this.

The StockRank is 85 but beware that metrics such as the trailing earnings multiple are not representative of normal earnings - the timing of any big, profitable disposals will always be unpredictable.

BTG Consulting (LON:BTG)

Up 1% at 119p (£190m) - Third Quarter Trading Update - Graham - AMBER/GREEN =

This is the company formerly known as Begbies Traynor, now with a more modern collection of letters as its name.

This is a straightforward “in line” update:

Financial performance across the Group has been consistent with the board's expectations during the quarter. As a result, our expectations for the full year remain unchanged, which would extend our track record of profitable growth.

Full year expectations are helpfully provided: adjusted PBT of £23.7 - 25.4m, with a consensus of £24.3m.

The restructuring team gets singled out for “positive levels of new instructions, supported in part by the challenging macroeconomic backdrop”. Traditionally, as an insolvency practitioner, Begbies has been a counter-cyclical stock, as greater economic difficulties translate into more insolvencies.

CEO comment:

"During the period, we completed our rebrand and name change, bringing our market-leading financial and real estate advisory businesses together under common branding. This change reflects the evolution of the Group in recent years into a broad-based advisory business.”

Estimates

Many thanks to Equity Development for publishing on BTG today.

They have made no changes to forecasts, which are as follows:

FY April 2026 revenue £167.3m, adj. PBT £24.2m, adj. diluted EPS 10.7p

FY April 2027 revenue £178.4m, adj. PBT £26.1m, adj. diluted EPS 11.6p

FY April 2028 revenue £186.3m, adj. PBT £27.6m, adj. diluted EPS 12.2p

Graham’s view

As you can see from the above, barring any further M&A, growth is expected to continue at a moderate pace with mid-single digit organic growth.

There’s nothing wrong with that but I’m not sure I’d be able to get behind the view that the shares are dramatically undervalued here, given the sector (professional services).:

Indeed, the ValueRank is 55, implying average attractiveness from the point of view of valuation.

If the balance sheet was stuffed with cash, then perhaps I could take a more positive point of view. But there isn't any significant amount of net cash to speak of. Net debt was £6m as of October 2025.

I therefore view our existing AMBER/GREEN position as fair.

Roland's Section

City of London Investment (LON:CLIG)

Up 1% at 387p (£202m) - Half-Year Report - Roland - AMBER/GREEN =

(At the time of publication, Roland had a long position in CLIG.)

Today’s results have received a cautiously optimistic reception. Perhaps that’s fair.

CLIG is achieving one of the core ambitions of any active manager – outperforming its benchmarks – but has once again failed to achieve the other – net inflows.

Fortunately, strong conditions in many of the CLIG’s core markets mean that overall funds under management rose once again and have subsequently reached a new record high of $11.9bn on 18 February:

Assets under management are the lifeblood of a fund management business as they drive higher fee income. CLIG’s H1 results show useful growth at both the top line and bottom line:

Net fee income up % to $37.3m

Operating margin: 32.9% (FY25: 33.2%)

Underlying pre-tax profit up 6.8% to $16.2m

Reported pre-tax profit up 10.9% to $14.0m

Underlying earnings up 9.7% to 19.3p per share

Interim dividend unchanged at 11.0p per share

Net cash ex-leases: $32.8m (FY25: $35.5m)

Underlying profits are adjusted to exclude investment gains and amortisation of acquired intangibles. I can see arguments in favour of each approach, but my sums show H1 free cash flow of $11.8m, so I am inclined to view reported pre-tax profit as most representative of cash generation.

Happily, both measures of pre-tax profit appear to be continuing the upward trend seen since FY23:

Investment performance

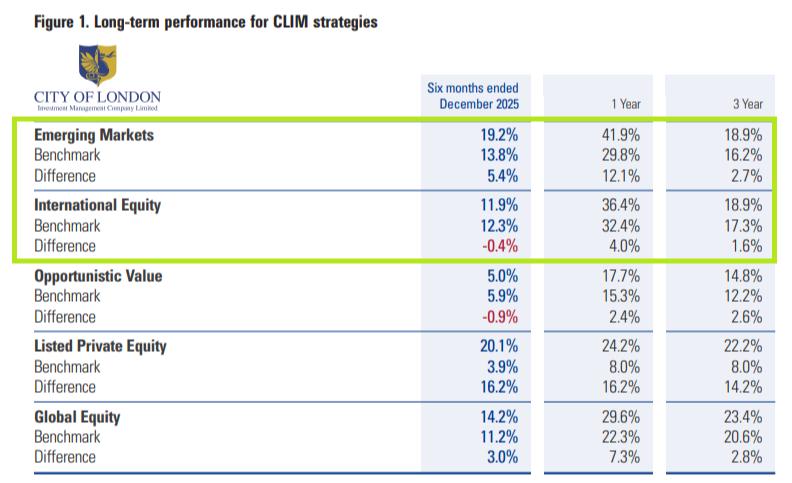

CLIG’s investment strategies primarily involve buying investment trusts at discounted valuations, particularly in emerging or non-US markets. One of the qualities of the business is that its strategies have tended to outperform their benchmarks.

The problem, in recent years, is that a simple S&P 500 tracker fund has outperformed almost everything else. This has reduced the appeal of strategies such as CLIG’s, regardless of their relative outperformance, making it harder to attract new inflows.

Fortunately, the balance seems to be shifting. Some of CLIG’s strategies delivered very attractive returns last year, both absolutely and relatively. Management says this was helped by “very strong country allocation, including overexposure to Vietnam and underweighting the underperforming Indian market”.

The strategies highlighted above accounted for 57% of group FUM at the end of December.

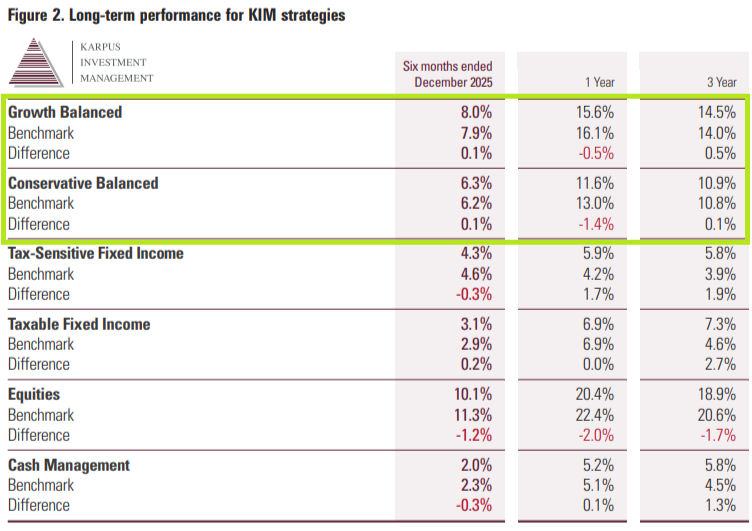

The other core strategies are run by the KIM division (Karpus Investment Management) and provide fixed income solutions aimed at wealthy US individuals. In this area, performance was aided by municipal bond funds “which benefited from strong NAV appreciation and narrowing discounts”, among other factors:

The strategies highlighted above accounted for 24% of group FUM at the end of December.

Flows: H1 net inflows were negative for both CLIM and KIM strategies, offset by positive investment performance:

CLIM: net outflows of $(739)m, investment performance +$1,036m

KIM: net outflows of $(114)m, investment performance +$239m

CLIG total: net outflows of $(853)m, investment performance +$1,275m

New CEO: CLIG announced the appointment of new CEO Cooper Abbott on 21 January. He appears to be a very well-qualified candidate, having previously founded and led the development of a boutique asset manager to have over $70bn FUM.

It’s early days yet, but in my view Abbott looks like a strong choice who is likely to bring an investor/owner mindset to the business.

Outlook & Updated Estimates

There’s no specific financial guidance in today’s outlook statement, but fortunately broker Zeus has issued update forecasts today and made these available on Research Tree – many thanks.

Zeus forecasts for FY26 have been upgraded and forecasts for FY27 and FY28 have been introduced:

FY25 actual adj EPS: 37.2p

FY26E adj EPS: 38.3p (+10.7% vs 34.6p previously)

FY27E adj EPS: 40.1p

FY28E adj EPS: 40.0p

It’s worth noting these forecasts are based on the assumption FUM will remain unchanged at $11.9bn over the whole forecast period. This is obviously unlikely, but provides a baseline against which Zeus (and investors) can judge future progress.

Upgraded earnings expectations for the current year suggest to me that the 33p dividend will remain safe, giving an 8.3% dividend yield.

Roland’s view

At current levels CLIG shares do not seem expensive to me, if Mr Abbott can finally achieve a long-awaited return to net inflows. Without this, the high yield may remain justified by a lack of underlying growth.

Today’s results highlight that CLIG shares have underperformed their total return target over the last five years:

Target total return of 7.5% to 12.5% annualised over rolling five-year period

5yr to 31 Dec 25: 5.6% annualised

Since listing in April 2006: 11.8% annualised

There’s no certainty this will change, as general market conditions for active managers remain quite challenging. However, I think conditions are more favourable than they have been over the last few years and am cautiously optimistic about the new CEO.

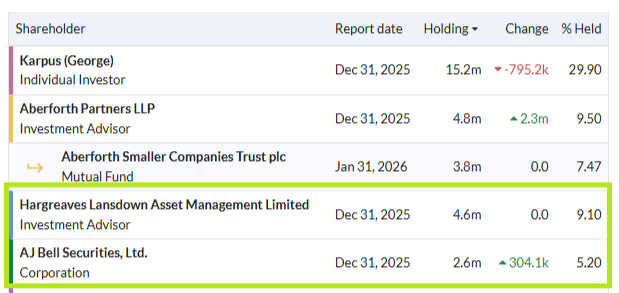

Interestingly, CLIG appears to have become a particular favourite with private investors, with Hargreaves Lansdown and AJ Bell now holding (as nominee) over 14% of the stock:

CLIG is a top 10 holding for me so I am naturally biased. However, I feel broadly reassured by today’s update and believe the valuation may remain attractive here:

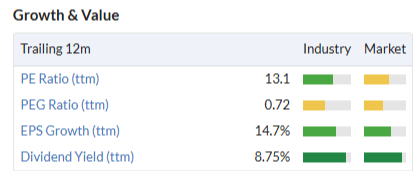

The StockRanks also have a positive view, with a perfect QualityRank and Super Stock styling:

I’m going to leave Graham’s recent AMBER/GREEN view unchanged today, out of recognition that CLIG has not yet achieved the net inflows needed to drive genuine sustainable growth.

McBride (LON:MCB)

Down 7% at 155p (£273m) - Interim Results for the 6mo to 31 Dec 25 - Roland - AMBER =

I took a neutral view on this private label consumer goods manufacturer in September, while noting that this “may be a little conservative”. McBride’s share price has risen by 29% since then, so it looks like I may indeed have been a little too cautious.

Today’s results cover the half year to 31 December 2025 and are billed as in line. However, the numbers suggest some weakness relative to the same period last year. Let’s take a look.

H1 results summary

Here are the key numbers from today’s results, stated at constant currency:

Revenue down 2.1% to £475.2m

Operating profit down 3.9% to £28.3m

Operating margin: 6.0% (H1 25: 6.6%)

Adjusted pre-tax profit down 1.3% to £26.2m

Adjusted earnings per share down 13.4% to 10.8p

Net debt up 3% to £120.6m (vs H1 25)

Adjusted return on capital employed of 30.8% (H1 25: 34.8%)

Management commentary: the company reports overall volume growth of 0.4%, with private label volumes up by 0.9%. Revenue rose by 0.8% at reported currencies but fell on a constant currency basis, but in either case I think it’s fair to assume that price remained flat or was slightly weaker. Perhaps unsurprising, given the current consumer environment.

Demand for private label products is said to remain strong through:

[…] private label household share of the top five markets at the end of 2025 ahead of recent all-time highs

Continued solid performance in the focus markets of laundry and Germany, supported by new contract wins

While management reports “profitability levels maintained”, both operating margins and the company’s own measure of adjusted ROCE were lower, so I’m not sure which profitability metric CEO Chris Smith is referring to.

The company is focusing the deployment of new capital on “automation and operational upgrades” as is also in the midst of a SAP rollout. This was completed in the UK last year and is now set to be extended to European operations.

Major IT projects always carry some risks and often overrun and the CEO reports “certain start-up challenges”, but this does appear to be proceeding without too much disruption.

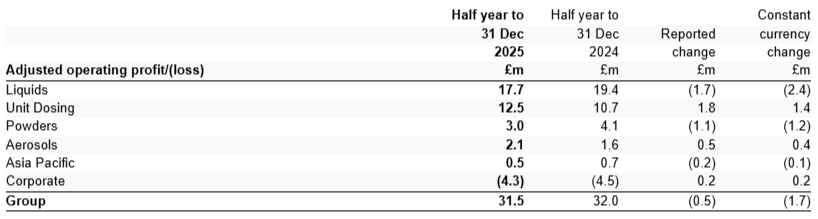

Looking across the business, profit performance was mixed across the group’s divisions, with the higher margin Unit Dosing business continuing to help support overall profits. At 10.8%, Unit Dosing margins are nearly double the 6.6% earned by the Liquids business (both of these refer to laundry products):

Outlook

Management says the business remains “on track to deliver full-year results in line with analysts’ expectations”.

Consensus forecasts are given as being for an adjusted operating profit of £64.7m. This implies a near-even H1/H2 profit weighting so does not look too challenging assuming performance remains stable.

Broker Zeus has left profit forecasts unchanged today:

FY26E adj EPS: 21.6p

FY27E adj EPS: 22.5p

These estimates put McBride on a forecast P/E of seven.

Roland’s view

McBride’s share price is down by 7% today, but I don’t think these results are particularly alarming. The only two niggles I would highlight are:

Continued pressure on margins, as I discussed in September;

Net debt of £120m is 1.4x EBITDA – within the company’s target range, but a little higher than I’d ideally like to see for a fairly low-margin manufacturer with negative working capital.

While McBride’s ROCE of c.30% is impressive, this is partly achieved through carrying high levels of payables that are presumably funded by customers paying for products before McBride pays its own suppliers.

While this model can work well and generate attractive returns, it’s not without risk either. In such scenarios, I prefer to see low levels of debt.

In terms of valuation, I am tempted to see McBride as being priced about right at current levels, or perhaps only slightly cheap.

I’m going to remain neutral today for the reasons I’ve highlighted above, and because I’d like to see evidence of a return to revenue growth to provide potential for meaningful profit expansion.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.