Good morning - it's the last trading day of the week, and the month!

Calling it there, thanks everyone. Have a fine weekend. Spreadsheet accompanying this report: link.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our View (Author) |

|---|---|---|---|

International Consolidated Airlines SA (LON:IAG) (£20.9bn | SR89) | Revenue +3.5%, operating profit before exceptional items +13.1% (€5,024m). ROIC 18.5%. “Positive outlook for 2026 supported by compelling market dynamics and secular long-term demand.” | ||

Flutter Entertainment (LON:FLTR) (£16.0bn | SR22) | FY2025 revenue +17% benefiting from M&A. Adjusted EBITDA +21%. Net loss $407m due to $556m impairment charge. 2026 guidance: revenue +12%, adjusted EBITDA +4%. “US current trading largely reflects the impact on our customer base of the very high gross revenue margins achieved in the second half of Q4, driving lower levels of customer engagement into 2026.” | ||

Melrose Industries (LON:MRO) (£8.0bn | SR46) | Revenue +8%, adjusted operating profit +23% (£647m). New £175m buyback. Dividend up 20%. 2026 guidance: adjusted operating profit of £700 million to £750 million. | ||

Intertek (LON:ITRK) (£7.2bn | SR68) | Expanded its footprint in Colombia with agreement to acquire QTEST, “a market-leading provider of high-quality electrical testing and certification services”. 2025 revenues £2m. | ||

Pearson (LON:PSON) (£6.1bn | SR73) | 2025 sales +4%, adjusted operating profit +6% (£614m). “Confident in outlook, guiding to mid-single digit sales growth for 2026 and beyond. Strong financial position, with £350m share buyback well underway.” Medium term guidance reiterated. | ||

Tritax Big Box REIT (LON:BBOX) (£4.6bn | SR65) | Net rental income +10.6%. EPRA net tangible assets per share 187.76p (last night’s close: 170.3p). LTV 33.2%. “We enter 2026 very well positioned with a clear strategy, multiple organic growth drivers, a supportive market backdrop and a strong balance sheet.” Anticipating acceleration in adjusted EPS growth in FY26. | AMBER/GREEN = (Graham) The discount to NAV has narrowed to only 9%, compared to 20% a year ago. But I think I can stay AMBER/GREEN on the basis that trading remains very solid, with stable vacancies and gradually rising rents, and with an interesting growth opportunity in data centres. Perhaps the discount can narrow even a little more and approach the NAV? | |

Rightmove (LON:RMV) (£3.3bn | SR35) | All 2025 metrics in line with guidance. Revenue +9%, underlying operating profit +9%. “Property end-market trends remain supportive for our partners' businesses.” H2 weighting expected in 2026, H1 impacted by “fewer developments coming into the year and the strong mortgage comparator last year”. | GREEN ↑ (Graham holds) I’m going to upgrade this back to GREEN today, on the grounds that this is a very strong results statement, with a confident outlook, and the market has reacted positively to it (potentially signalling a positive change in sentiment). | |

Rathbones (LON:RAT) (£2.4bn | SR79) | FUMA £115.6 billion (Dec 2024: £109.2bn). PBT +53.5% (£152.9m), underlying PBT +4.6% (£238m). “We remain confident in achieving our 30% underlying operating margin target by the fourth quarter of 2026, assuming FUMA growth of 3% in 2026, stable inflation and interest rates in line with current market expectations.” | ||

Just (LON:JUST) (£2.3bn | SR41) | Planning to be acquired by Brookfield Wealth Solutions in H1 2026. | PINK | |

Senior (LON:SNR) (£1.08bn | SR65) | SP +18% Following three proposals, the Board appointed Lazard and Jefferies to initiate discussions with third parties. The company confirms it has received two further, superior all-cash proposals from other potential offerors. Discussions with potential offerors remain ongoing. £40m buyback postponed. | PINK (Graham) [no section below] Clearly I got this one wrong, as I thought it was full-priced last August when the market cap was merely £814m. The market cap is now pushing £1.3 billion and I calculate that the P/E multiple has today reached a remarkable 32x. This has always seemed to be a rather dependable defence stock but with rather average ROE and ROCE metrics and single-digit growth forecasts, I simply don't understand the attraction to a buyer at this sort of price. The Board are surely doing right by shareholders if they negotiate a sale price anywhere around this level? | |

Hays (LON:HAS) (£717m | SR30) | SP -10% Net fees down 9%, operating profit before exceptional items down 25%. “Continued macroeconomic and political uncertainty.” “New Year Temp & Contracting Return to Work volumes are building in line with prior year and our expectations. Perm remains tough but stable overall, with activity returning to pre-Christmas levels.” The CEO also steps down with immediate effect, "for personal reasons". | AMBER/RED = (Graham) [no section below] We've been AMBER/RED on this (e.g. see here) which appears to have been the correct call as both the company and its share price continue to suffer. The company blames macroeconomic and political uncertainty, but I don't buy it at this stage - there is something structurally broken with many recruitment companies, in my view. Economic challenges may be a factor, with employees reluctant to switch jobs and employers reluctant to expand, but I don't see how this can explain the consistent underperformance of the sector for a few years now. I think that another explanation - disintermediation by LinkedIn, for example - is needed. The Hays share price has been broadly declining for about five years now and on these reduced earnings, it does not even appear cheap to me yet. | |

Castelnau (LON:CGL) (£315m | SR33) | Hornby agrees sale of Scalextric & CEO departure and succession plan | Portfolio company Hornby Hobbies Ltd has agreed to sell Scalextric for £20m. £8.5m upfront, the remainder deferred and payable out of free-cash flow. | |

SRT Marine Systems (LON:SRT) (£209m | SR38) | Follow-on contract with an existing sovereign customer to expand the scope of the system. | ||

Gooch & Housego (LON:GHH) (£207m | SR63) | The order book has grown strongly and is currently at £168.3m (30 September 2025: £142.3m). “The Board's expectations for the current year remain unchanged, and are underpinned by the order book, self-help measures and new business pipeline…” | ||

Jubilee Metals (LON:JLP) (£137m | SR38) | The sale of the chrome and PGM Operations in South Africa has now been completed. Now focused on operations in Zambia. Discussions well advanced with a range of shareholders to ascertain views on future distributions (dividends/buybacks). A High Court process is needed to create distributable reserves. | ||

Rentguarantor Holdings (LON:RGG) (£42m | SR25) | RentGuarantor has developed AI-powered tools capable of automatically reading and analysing tenant documents. | RED = (Graham) [no section below] I was hopeful that this might prove itself to be a quality AIM stock, but since joining the exchange it has unfortunately proven itself to be rather promotional with a steady stream of RNS announcements, not all of which seem to be RNS-worthy. February alone has seen five announcements of this nature, and they seem to be increasing in their frequency. There have been four in the past week alone: if they keep going at this rate, they will soon be releasing multiple announcements per day. | |

Directa Plus (LON:DCTA) (£14m | SR40) | The Board is in advanced discussions with its long-standing substantial shareholder, Nant Capital, LLC, regarding a €4 million potential loan. |

Graham's Section

Rightmove (LON:RMV)

Up 5% to 448.9p (£3.42bn) - Annual Financial Report - Graham - GREEN ↑

(At the time of writing, Graham has a long position in RMV.)

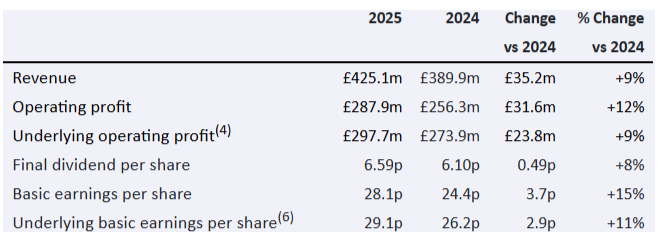

Rightmove plc, the UK's largest property portal, today announces its audited results for the year ended 31 December 2025

Rightmove has been under pressure for most of the past year, as the market digests the potential impact of AI. The share price is down by 45% from the peak last summer:

Thankfully, these results read well.

The highlights table:

If you didn’t know that sentiment around this stock was so poor, it would be hard to guess it from these numbers.

Market share: this stands out to me.

Record share of time spent on Rightmove at year-end (89% Comscore; 75% SimilarWeb/data.ai/Sensor Tower)(1) with over 85% of traffic direct and organic(2); strong usage of a range of new consumer features, with several powered by AI

My reason for involvement in Rightmove - and the reason it’s such a controversial company at times - is the natural monopoly (or duopoly with Zoopla) which it appears to enjoy.

And with its share of time now apparently at a record, this monopoly is as strong as ever.

The fact that 85% of traffic is “direct and organic” is also key: everybody who is interested in property knows that Rightmove is there and will visit it without any need for an ad to prompt them. This is a serious competitive advantage.

OnTheMarket, now owned by CoStar Group, does not appear to be having any detectable impact on Rightmove’s market share.

AI: the market has been concerned by the threat of AI to existing internet platforms, and was also spooked by Rightmove’s intention to spend big on its own AI tools. Here is the latest on that topic.

Let’s quote extensively from Rightmove’s comment on its data and AI tools, as I think this is key to the story. I’ve highlighted some snippets that strike me as important:

Rightmove benefits from 4 petabytes (PB) of historic and live data - all stored on its unified and cloud enabled data platform - with over 90% proprietary to Rightmove. This data is processed by c.200 proprietary models to create differentiated outcomes to both consumers and partners

o Highest ever delivery of technology releases from our product teams - more than 6,000 during the year - leveraging Rightmove's data and technology, along with insights from c.20,000 minutes of user testing, over 85,000 surveys, and c.500,000 recorded web and app sessions

o Examples of new products for partners included Online Agent Valuation and AI-enhanced Opportunity Manager for Estate Agents, Direct Appointment Booking for New Homes, a new data API and property details pages for Commercial partners, and upgrades to Rightmove Plus and the Rightmove Hub

o Examples of new features for consumers included MyPlaces, Style with AI, AI Keywords within the app, a global-first Property Checker within Mortgages, and a Renters Checklist within MyRightmove

o A multi-year collaboration with Google Cloud enables Rightmove to lead digital innovation in the property ecosystem, leveraging its extensive datasets and accelerate products that deliver value to consumers and partners

Personally, I think it makes sense for Rightmove to spend big on innovation during a period in which there is a lot of change in how business is being done online.

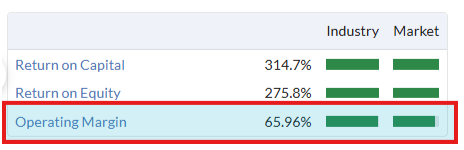

There is no question in my mind that they can afford it, given their profit margins:

Of course it’s hard to say in advance if all of this AI/product spending is going to generate an attractive return, but I have no problem with them taking that risk.

My main priority is that Rightmove remains the #1 place to research properties, and anything that ensures this happens is fine with me. I am happy for profits to not be maximised for a couple of years, if that’s what it takes. For me, the bigger risk is that they don't spend enough, and then lose out to superior products at other platforms.

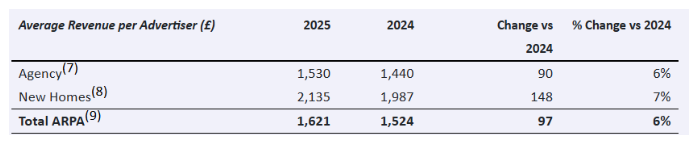

Average revenue per advertiser

The number of estate agent/developer customers is very stable (only up 1%), but they continue to spend more each year. The key ARPA metric just keeps rising:

End-market trends: the property market is “supportive” for Rightmove’s customers, with more Bank of England rate cuts expected in 2026 and mortgage rates down year-on-year.

Current trading: Rightmove has entered 2026 “with strong momentum”. The outlook sounds strong although it does have an H2 weighting.

In line with our guidance set in November, we continue to expect 2026 revenue growth of 8-10%...

We expect year-on-year growth in the second half of 2026 to be stronger than the first half. First half growth is impacted by fewer developments coming into the year and the strong mortgage comparator last year.

We anticipate c.1% growth in membership and ARPA growth of £110-120 across Agency and New Homes.

CEO comment: contained within his very confident statement, he says “we will introduce a Rightmove app-in-GPT on OpenAI in the near future.” Interesting!

Dividend: the final dividend increases from 6.1p to 6.59p. There is also going to be a £90m share buyback (reduces the share count by less than 3% at the current market cap).

Graham’s view

Without wishing to get too philosophical on you, I do think the share price movement here over the past year is consistent with the Mr. Market metaphor: the one where he is an emotional neighbour, shouting house prices at you every day.

Rightmove hasn’t changed all that much over the past year, and yet the share price has been cut nearly in half.

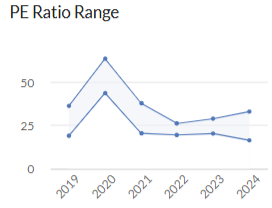

The P/E multiple has often been in the mid-20s and high 30s:

And then it fell to less than 14x:

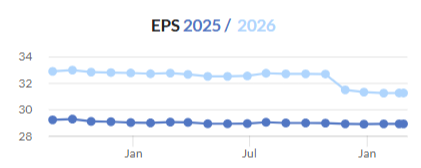

If you didn’t know any better, you’d assume that the earnings outlook had dramatically changed. And maybe it has in the long-term, if AI disrupts it. But that’s not reflected in short-term forecasts:

The cut to the FY26 EPS forecast was from 32.7p to 31.5p. That does not seem of great significance to me.

I’m going to upgrade this back to GREEN today, on the grounds that this is a very strong results statement, with a confident outlook, and the market has reacted positively to it (potentially signalling a positive change in sentiment).

Granted that as a shareholder, I may be biased.

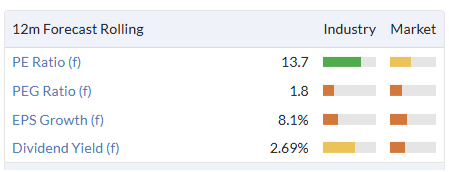

I also acknowledge that the StockRanks don’t like it yet:

I don’t like to disagree with the StockRanks very often, but in this case the main area of disagreement is Momentum - the StockRanks are wary of momentum, and I'm willing to look past that.

However, with the share price rising on the back of today’s results, I think we have a genuine piece of evidence that momentum and sentiment might be about to change.

I also note that the other area of StockRank weakness, the ValueRank, has been increasing. This is a stock that has rarely offered much fundamental "value".

So I’m taking a contrarian stance here by upgrading this back to GREEN, and I may be in a small minority with this view. But I hope you can understand my reasons, whether or not they prove to be valid.

Finally, checking shorttracker.co.uk to see how active the short-sellers are here, I see that disclosed short interest is about 2% of total shares outstanding. That’s a meaningful figure, but not too alarming. For context, there are 70 other UK companies where the disclosed short interest is higher than 2%.

Rightmove is 3% of my personal portfolio and if I didn’t have any other good ideas, I’d even consider topping up my position here!

Tritax Big Box REIT (LON:BBOX)

Unch. at 170.35p (£4.6bn) - Results for the year ended 31 December 2025 - Graham - AMBER/GREEN =

Tritax owns “the UK’s largest logistics investment and land development portfolio”.

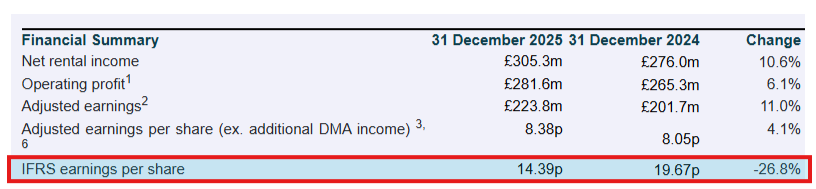

Some very decent figures here, until we get to the official earnings per share figure (“IFRS earnings per share”). More on that at the end.

Do bear in mind that the growth in net rental income has been boosted by an acquisition, so it’s not “like-for-like”.

Like-for-like rents grew 4.2%, while the portfolio’s like-for-like estimated rental value grew 4%. So the real growth in rents is clearly running at around 4%.

Vacancies are stable at 5.6%.

We get some interesting comments from the Chair:

"Over the past year, Tritax Big Box has taken important strategic steps that reinforce both the capabilities of our platform and our growth drivers. The successful integration of the UKCM logistics assets, together with the portfolio acquisition from Blackstone, has created a meaningful c.20% exposure to urban logistics, strengthening our end-to-end offer and further cementing our leadership position across the UK supply-chain spectrum.

"In parallel, we have launched our data centre programme, pioneering an innovative 'power-first' approach that unlocks opportunities in digital infrastructure. In just 12 months, we have assembled a high-quality pipeline and made significant progress, positioning the company to generate exceptional returns for Big Box shareholders from the most compelling structural growth opportunity in real estate.

The company’s stated growth drivers are 1) rental reversion (new leases at higher rates after old leases expire), 2) developing best-in-class logistics assets, 3) data centres. The data centres are “targeting exceptional risk-adjusted returns”.

Balance sheet: net debt is £2.6 billion and the loan-to-value is 33% which is pretty standard and safe for most REITs in my view. Indeed, a REIT with an LTV much lower than that might even make me suspicious - why not borrow more to maximise returns?

LTV last year was 29%, with the increase being due to the acquisition of a portfolio from Blackstone.

The weighted average cost of debt is a moderate 3.6%, although this is up from 3.1% a year ago. A £400m RCF has been refinanced along with a £300m 7-year bond. Average maturity is 4.3 years. Nothing out of the ordinary here, as far as I can tell.

Graham’s view

As always, the key metric for me when examining a REIT is net asset value vs. the share price.

NAV per share is calculated under normal accounting rules and under EPRA’s rules for real estate. In both cases, the result at BBOX is about 187p - 188p. So the current share price offers about a 9% discount to that figure.

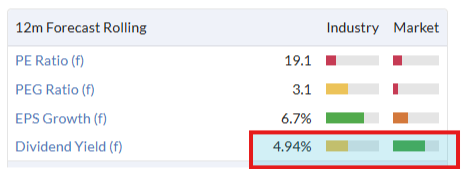

When I looked at BBOX a year ago, the discount was 20% and I took a moderately positive stance.

The shares are up by 18% since then, and a useful dividend yield has also been paid:

So perhaps I should have been more positive on this a year ago.

At the new, higher valuation, I think I’ll keep us moderately positive, as there is still some level of discount that could be narrowed, and the company appears to be trading very solidly.

The only issue I needed to investigate was the year-on-year decline in earnings per share under accounting rules. There were two main reasons for this, that I can find on the income statement.

Change in fair value of properties. Last year, there was a £244m gain in fair value. This year, there was “only” a £199m gain. This doesn’t concern me.

Impairments: last year, there were barely any impairments. This year, there were £29m of impairments. Checking footnotes, I find that it was due to a site where BBOX’s “expectation on the possible likelihood and timing of achieving planning consent changed in the period.” In the context of a multi-billion pound portfolio, this does not strike me as terribly important.

Neither of these factors require me to change my stance. So I’m staying where I was on this one.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.