Good morning! I hope you had a good weekend.

Overnight action is fairly dire in the major indices:

- FTSE futures are down 1%

- S&P 500 futures are gapping lower and currently down 1.6%

- EURO STOXX 50 down 2.9%

US oil futures are up $12 at $102.50, while Brent crude is up $14 at $107.

It looks set to be another dramatic week as financial markets digest the impact of the ongoing conflict in the Middle East.

8am update: The FTSE is opening down 1.2%. Reuters reported yesterday that "Iraqi oil production from its main southern oilfields has fallen by 70% to just 1.3 million barrels per day as the country is unable to export oil via the Strait of Hormuz due to the Iran war, three industry sources said on Sunday." Perhaps it's prudent to assume that this situation is going to persist for some time?

We're finished for today, thank you. Spreadsheet accompanying this report: link.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

GSK (LON:GSK) (£83bn | SR92) | Alfasigma will acquire worldwide exclusive rights to develop, manufacture and commercialise linerixibat, which is being developed as a treatment for cholestatic pruritus in primary biliary cholangitis. GSK will receive $300m upfront, plus up to $390m for various regulatory and sales milestones. GSK will also receive “tiered double-digit royalties”. | ||

Pan African Resources (LON:PAF) (£3.2bn | SR72) | PAF will acquire ASX-listed gold explorer Emmerson for £163m or 0.1493 new PAF shares for each Emmerson share. Deal will allow consolidation of Tennant Creek JV project (75% PAF/25% Emmerson). PAF will apply for ASX listing. | ||

Clarkson (LON:CKN) (£1.36bn | SR82) | Revenue down 5%, adj pre-tax profit down 21% to £90.6m, in line with expectations. | AMBER/GREEN = (Roland - I hold) Today’s results show the expected decline in profits last year. This was mainly caused by a difficult H1, when US tariffs caused widespread disruption. H2 was much stronger, despite disruption caused by Russia-related sanctions. Clarkson’s profit metrics were slightly weaker than usual last year, but the broking division’s forward order book has expanded and the Financial and Research divisions both made strong contributions last year. Broker forecasts are upgraded for the second time in three months today. In this context, I think the valuation remains reasonable and in keeping with Stockopedia’s High Flyer styling, so I’m leaving my broadly positive view unchanged. | |

Newriver Reit (LON:NRR) (£327m | SR70) | Completed sale of Cuckoo Bridge Retail Park to institutional investor for £26.5m, reflecting a net initial yield of 6.9%, “an excellent outcome in southwest Scotland”. Now completed £100m of disposals in FY26, in line with book value. Proceeds will reduce LTV to “close to” medium-term target of <40%. | AMBER/GREEN (Roland) [no section below] Today’s update seems encouraging although management doesn’t specifically say that this disposal was in line with book value, leading me to think it may have been slightly below. However, £110m of recent disposals collectively in line with book value does not seem a bad result. While the company’s comment about the sale being a good result for the region flags up the challenge of owning retail property in non-prime areas of the UK, portfolio occupancy of 96.1% (reported in January) does not seem a bad situation to me. Management suggests this sale will reduce leverage towards its target of 40%, but LTV was reported at 42.3% in September. This suggests to me that any benefit to leverage from this disposal is relatively modest. NewRiver currently trades at a c.25% discount to NAV. Broker forecasts suggest the 9% dividend yield should be covered by cash flows this year. I think it’s fair to take a broadly positive view, with the caveat that I’d want to do some further research into the remaining portfolio before considering an investment. | |

Ferrexpo (LON:FXPO) (£301m | SR67) | Following suspension on 20 Jan 26, improved electricity supply has allowed production to restart at FPM. One pellet line is currently in operation, FXPO is using its own rail wagons to export to Eastern & Central Europe. The ability to make payments outside Ukraine is currently limited due to the liquidation of the group’s Swiss bank. Other issues are complicating the appointment of a replacement bank. Due to this, “there is a risk of material negative consequences for the Group”. | ||

Kitwave (LON:KITW) (£246m | SR98) | Cash consideration to be paid by buyers will now be funded by a combination of equity from the OEP Funds and new debt facilities, rather than wholly with equity from OEP Funds. | PINK | |

Kenmare Resources (LON:KMR) (£226m | SR47) | Tax authority in Mozambique is seeking to impose “updated terms” on Kenmare that would effectively increase the group’s tax burden and working capital requirements and might also complicate its offshore banking situation. Changes had previously been under negotiation for a more incremental solution. | ||

AdvancedAdvT (LON:ADVT) (£219m | SR31) | AdvancedAdvT chairperson Vin Murria has been appointed to the board of M&C Saatchi as non-exec deputy chair. AdvancedAdvT does not intend to make an offer for M&C Saatchi. | ||

Mkango Resources (LON:MKA) (£194m | SR20) | Mkango subsidiary HyProMag has commissioned a second automated hard disk drive pre-processing unit in the UK with the potential to process more than 30,000 HDDs per week. Magnets will be separated and sold for precious metals recovery. | ||

KEFI Gold and Copper (LON:KEFI) (£173m | SR35) | All the Tulu Kapi Project physical activities and associated financing arrangements are flowing in accordance with the schedule for first gold pour in early 2028 and full production by mid-2028. | ||

M&C Saatchi (LON:SAA) (£146m | SR58) | SP +5% By mutual agreement the CEO is stepping down from 31st March 2026. Vin Murria (major shareholder) appointed NED and Deputy Chair. The Chair becomes Exec Chair. | AMBER = (Graham) This advertising agency issued a profit warning last November before following it up with an "in line" update in January. That more recent update confirmed net cash of £13m at the end of 2025, having increased over the H2 period - and the net cash position is the main reason I'm not more bearish on this stock. Today we learn that Vin Murria is taking a more hands-on approach to this company, where both she and her corporate vehicle AdvancedAdvT (LON:ADVT) are major shareholders. She will be a NED, while the existing non-Exec Chair will become Exec Chair. It's a significant shakeup and I can't argue that it's a bad idea, considering the extent to which profit forecasts have been slashed here over the past six months. The 2026 EPS forecast, previously 23.4p, is now just 14.6p. While I admire the energy that's being applied to fix the company's problems, I believe it's probably still too soon for me to upgrade our stance. | |

Strix (LON:KETL) (£107m | SR93) | The Group now expects to generate revenue of c.£150 million and adjusted profit before tax in the range of £9.8 million to 10.2 million for the financial period ending 31 March 2026 ("FY26"). | BLACK (RED =) (Graham) | |

Aurrigo International (LON:AURR) (£78m | SR37) | £6.28m contract with Ultra Global Limited, the developer of personal rapid transit systems, to design and manufacture an initial quantity of 25 autonomous guided vehicles for use in airport and passenger transit settings in the UK. Ultra Global is owned by Aurrigo’s largest shareholder. | ||

Helix Exploration (LON:HEX) (£61m | SR16) | Helix has executed a lease agreement for a high-pressure jumbo tube trailer, “marking a key operational milestone for the Company.” The trailer has a service capacity of 156,300 standard cubic feet of compressed helium, providing the Company with dedicated helium transport capability. | ||

Cobra Resources (LON:COBR) (£47m | SR13) | Results from 4 of 18 recently completed Reverse Circulation drill holes from Blue Rose, a copper-gold-molybdenum prospect within the Manna Hill Copper Project (South Australia). “Cobra considers that these results validate the potential of the Manna Hill Copper Project.” | ||

Tekmar (LON:TGP) (£13m | SR69) | FY25 revenue of £28.7m (FY24: £32.8m) and Adjusted EBITDA of £0.1m (FY24: 1.7m) is in line with market expectations. FY26: “continued positive business momentum… has yielded £43m of new orders since 1 July 2025 and a current record order book of £40.7m.” The Board expects H1 2026 to be ahead of H1 2025 and full year performance to be in line with current market forecasts. | ||

Cordel (LON:CRDL) (£11m | SR18) | Further upgrade of its contract with Genesee & Wyoming Inc. , owner and lessor of more than 100 short line and regional freight railroads in North America. The contract has been further extended to cover 7 regional sub-divisions across the G&W Canadian division. |

Graham's Section

Strix (LON:KETL)

Down 12% at 41.5p (£94m) - Review of Last Six Months and Trading Update - Graham - BLACK (RED =)

Strix Group Plc (AIM:KETL), the global leader in the design, manufacture and supply of kettle safety controls and other components and devices involving water heating and temperature control, steam management and water filtration, announces a trading update, cost optimisation programme and CEO update.

It took me quite a while to decipher this trading update first thing this morning,

There has been a change of accounting date here, announced in September, which means that we now have a 15-month financial “period” rather than a financial year.

I’m generally suspicious of changes to financial year-ends, and the fact that Strix is doing one is not going to change that.

In my mind, changes to financial year-ends are most often associated with companies that are performing badly, and where the straight presentation of their financial results will not do them any favours.

In September, Strix said:

The Audit Committee has reviewed the date of the Group's financial year end and, to align better with industry cycles, especially around the key holiday season sales, as well as to allow Strix to integrate industry insights gained from attending the Canton Fair in April and October into its forecasting, the Company intends to change its accounting reference date and financial year end from 31 December to 31 March.

I can accept it more easily when a company is in a very early stage of its development, and is still setting itself up. But Strix was founded in 1951 (as “Castletown Thermostats”). It has evolved over the years but kettle safety controls are still its core business and it should already be aligned with the relevant industry cycles, if that is something that is really necessary. So I’m afraid I simply do not buy the reason given for the change in accounting year-end.

With that out of the way, let’s try to decipher the rest of this update.

Debt reduction

They remind us of the recent £105m disposal of Billi, which has enabled massive debt reduction.

Net debt at the prior interim results (to June) had been £69m. Net cash on completion of the Billi disposal was £35m. They subsequently launched a £10m share buyback programme (average purchase price so far: 48.7p).

Inventory reduction: they achieved their targeted £8m inventory reduction ahead of schedule, by 31 December 2025.

Rising commodity prices: in response to the rising cost of copper and silver, they raised their product prices and reduced capacity in order to forward fund these costs.

Therefore apart from the outflow caused by the £10m buyback, we should see an incredibly strong full-year cash flow statement, with various cash-generating activities happening on top of the Billi disposal.

Current trading: I had to read this section a few times, and I still think it’s very unintuitive.

Whilst market conditions remain challenging, Strix is encouraged to report that the early indications of post-tariff improvement in the Controls division that it experienced in Q425 have continued to build in early 2026. With trading volumes, most notably in the lower margin, less regulated markets to date, and order books for March, now holding at consistently higher levels than the Group saw in Q125.

However, what the Group has not experienced to date, is any anticipated catch-up of volumes lost over the course of 2025, particularly in the regulated markets, which it had previously anticipated to come through in the run-up to the busier April to June production period. Alongside this, the Board has made the commercial decision to reduce seasonal promotional activity in the final quarter…

So trading volumes are holding at consistently higher levels than they saw in Q1 2025, but at the same time they haven’t seen the recovery of volumes lost over the course of 2025?

It might be entirely my fault for having difficulty comprehending this, but I think it is poorly written

I think the plain English explanation may be that trading volumes are up in less regulated markets, and down in more regulated markets.

In any case, this update is most definitely a profit warning:

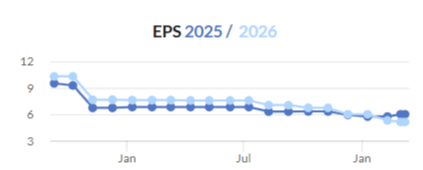

As a result of the above, the Group now expects to generate revenue of c.£150 million and adjusted profit before tax in the range of £9.8 million to 10.2 million for the financial period ending 31 March 2026 ("FY26").

CEO search: their existing CEO is stepping down in May, and they continue to search for a new one.

Estimates

Thanks to Equity Development for publishing on this today. Their changes to key estimates are as follows:

15-month period to March 2026: revenue £148.5m (previous estimate: £152.5m), adj. PBT £9.8m (previous estimate: £12.1m).

FY March 2027: revenue £93.5m (previous estimate: £97.5m), adj. PBT £6m (previous estimate: £9.3m).

Fortunately, the company is still expected to have net cash of close to £30m at the end of each period. The new estimate for FY March 2027 is that they will finish with net cash of £28m.

Looking beyond then, hopes for improvement performance include the potential for a contract manufacturing relationship with Billi, the adoption of next generation kettle controls, and widened use of these controls beyond just kettles to other small appliances.

Graham’s view

My main reason for caution here - the atrocious balance sheet - is no longer valid, with the company now sitting on a healthy cash balance.

However, this is still a pretty serious profit warning from Strix today. So I’m going to have to stay negative for the time being.

Looking ahead, assuming that trading stabilises, are there grounds for optimism? It could be argued that the current enterprise value (about £60-65m) is perhaps a little “cheap” against forecast PBT of £6m.

Personally, I don’t see it: there have been too many disappointments here over the years. Fundamentally, I no longer have faith in the value of the IP: I originally thought that Strix’s long-standing patents and market share implied that it was a quality company, but its actual performance has not borne this out.

I also think the CEO situation raises questions - it will be interesting to see who they appoint.

Having said all of that, I probably will upgrade this back to AMBER or AMBER/RED, whenever trading stabilises, as it’s no longer in a debt emergency.

Roland's Section

Clarkson (LON:CKN)

Up 1% at 4,435p (£1.37bn) - Preliminary Results - Roland - AMBER/GREEN =

(At the time of publication, Roland had a long position in CKN)

Clarkson is not as directly exposed to events in the Middle East as oil and gas producers, but it’s still very closely involved.

From offices in 25 countries on six continents, we play a vital intermediary role in the movement of the majority of commodities around the world.

As the world’s largest shipbroker (founded in 1852), it will be heavily involved in reshaping global tanker shipping flows (and rates) resulting from the near-closure of the Strait of Hormuz. Clarkson will also be exposed to any other second-order effects the conflict may have on global trade flows.

These come in addition to the existing disruption caused by sanctions relating to Russia. Clarkson notes that “nearly 1,000 vessels in the global tanker fleet” are currently sanctioned.

While these complex global conditions will keep Clarkson’s brokers busy, they are likely to be favourable for the group’s high-margin data business, which contributed around 10% of group profits last year.

The company cut profit forecasts early last year when President Trump’s tariff shock hit markets. But forecasts have stabilised and edged higher since then, with Clarkson’s most recent update upgrading guidance.

Today’s results appear to be in line with revised guidance for 2025 and have prompted a further, more substantial upgrade from broker Panmure Liberum.

Let’s take a look at today’s results and commentary.

2025 results summary

Profits were expected to fall this year so today’s 2% drop in earnings was not a surprise.

Revenue down 5% to £631.4m.

Underlying pre-tax profit down 21% to £90.6m.

Reported pre-tax profit down 23% to £86.7m.

Adjusted earnings per share down 21% to 225.8p.

Dividend up 3% to 112p per share.

Free cash resources up 7% to £232m.

Forward Order Book for invoicing in 2026 up 6% to $244m.

Commentary from chair Laurence Hollingworth suggests that 2025 was a year of two halves:

… the first half of the year [was] marked by significant political shifts, escalating tariff regimes, and the increase in use of sanctions by government authorities. These dynamics created a period of significantly reduced activity across many industries, with companies facing unprecedented challenges in decision-making and market engagement.

Conditions stabilised during the second half:

Despite these headwinds, the second half of the year started to see renewed momentum. Market sentiment improved, and businesses began to move beyond the earlier standstill, as larger players actively re-engaged in transactions and Clarksons supported its clients through turbulent times.

Profitability & Cash Generation: despite the somewhat mixed trading environment, Clarkson’s quality metrics remained fairly good last year, albeit below 2024 levels:

Operating margin: 12% (FY24: 14.9%).

Return on Capital Employed: 13% (FY24: 18.2%).

Return on Equity: 13% (FY24: 18.0%).

Free cash flow for the year fell to around £56m by my calculations (FY24: £108m), due to some large adverse movements in receivables. However, stripping these out suggests a more neutral picture to me.

This view is supported by the 7% increase in the company’s measure of net cash, free cash resources, which rose to £232m last year. This is defined as net cash including amounts held as short-term investments, but excluding cash reserved for bonus payments or regulatory reasons.

As critics often comment, bonus payments are significant in this business, in line with normal practice in the shipbroking sector. The amount reserved for bonuses at the end of last year fell from £249.6m to £211.1m.

Segmental commentary

Broking (operating profit £93.9m (2024: £122.6m)): this is the core of Clarkson’s business. It matches ships with freight, is active in the commodity derivatives market and plays a major role in the sale and purchase market for ships.

Broking is inescapably cyclical, but also benefits from the diversification benefit of operating in all major shipping segments.

CEO Andi Case notes that the business strengthened its capabilities in a number of growing markets last year, including South America. The company also acquired a business specialising in “fulfilling freight contracts with US government agencies”, which seems a timely deal.

While last year was disappointing in terms of profit, I don’t see too much to worry about on a longer view – this business is deeply embedded into the global shipping market (my bold):

Our continued investment in all areas of broking is underpinned by its robust performance across market-cycles and by the strength of our forward order book ('FOB'), which now extends for almost 20 years and provides substantial visibility over future earnings.

Financial (operating profit: 12.9m (2024: £5.2m)): this business enjoyed a strong year, offsetting some of the weakness in broking. Management note “an increasingly active capital markets environment”, with “particularly strong” trading in debt markets.

Support (operating profit: £4.8m (2024: £7.7m)): this business provides support services such as Agency services and support services for the offshore energy sector. Disruption to Suez Canal traffic and delays in offshore wind projects held back performance during the year, resulting in lower profit.

Research (operating profit: £10.5m (2024: £9.5m)): Clarkson’s data and research unit saw recurring revenue rise by 15% last year to represent 91% of total sales of £27.2m.

This business generated an operating margin of 39% last year and saw profits rise by 12%, highlighting the quality of the service and the value of the company’s “wide-ranging proprietary database and [...] constant flow of market-leading insights”.

Management say AI is “being leveraged in a balanced way” and emphasises that its technology already includes a high level of sophisticated processing and proprietary algorithms. I don’t see generic AI as a threat to this business due to Clarkson’s proprietary data and deep sector knowledge, neither of which is likely to be generally available to would-be competitors.

Outlook & Estimates

In the year to date, momentum from Q4 2025 has continued, market sentiment has been positive and trading has been good, evidenced by new spot business negotiated being higher than the same period last year.

With thanks to broker Panmure Liberum, we have access to an updated note on Research Tree today.

After a modest upgrade in January, Panmure has upgraded forecasts again, largely to reflect the strong result from the Financial business in 2025:

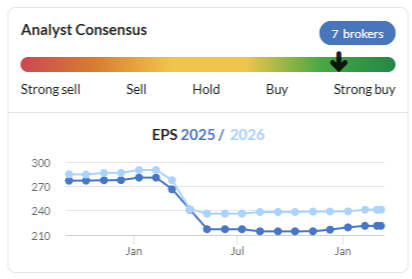

FY25 actual adj EPS: 225.8p

FY26E adj EPS: 257.8p (+7% vs prev. 241.9p)

FY27E adj EPS: 295.2p (+5% vs prev. 280.4p)

These estimates put Clarkson on a forward P/E of 17, falling to 15x for 2027.

Roland’s view

Clarkson is one of my largest personal holdings and a long-term position for me, so I am naturally biased.

That said, I like this business for the exposure it provides to global trade, shipping and commodity markets and for its long track record as a market leader.

The company has a strong balance sheet and a strong dividend history, with 2025 marking the 23rd consecutive year of dividend growth.

While critics point to the high level of remuneration enjoyed by CEO Andi Case and his brokers, my impression is that this is consistent with the wider shipbroking sector and has not prevented shareholders enjoying above-average returns over the last 20 years:

Clarkson shares aren’t as cheap as they have been at certain times in the last few years, but the valuation still looks reasonable to me on a long-term view. The StockRanks appear to concur, with High Flyer status and a notably high QualityRank.

I’m leaving my previous AMBER/GREEN view unchanged today.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.