Good morning!

4pm update: after studying various individual shares today, I'm bemused to see that the FTSE is down by over 2.5% this afternoon.

As always, I try to keep things in context: year-to-date, the FTSE is still up by 1%.

But a move such as we've seen today is always going to rattle people's emotions, especially considering that the primary reason for it is the expansion of war in the Middle East.

According to Reuters, "Qatar says Iran’s strikes damaged 17% of its LNG export capacity for three to five years".

Gas prices have soared, and the Strait of Hormuz is still effectively closed.

The latest developments come after Israel attacked Iran's South Pars gas field - the largest natural gas field in the world.

Some of Israel's oil refineries have in turn been attacked, with Iran saying that its response "is underway and not yet complete.”

It's all very concerning and financially it has been compounded with central bank developments today, the main one being:

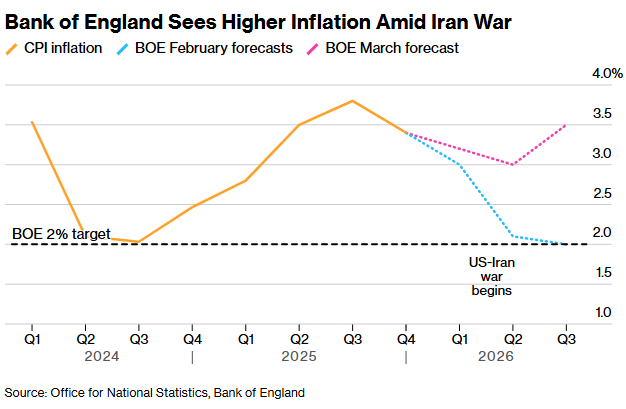

Bank of England - there has been a change in the mood music at the BoE, with traders now betting on interest rate hikes to combat inflation arising from the war in the Middle East.

At the meeting today, there was a unanimous vote to leave rates unchanged.

From the MPC meeting summary (emphasis added):

Conflict in the Middle East has caused a significant increase in global energy and other commodity prices, which will affect households’ fuel and utility prices and have indirect effects via businesses’ costs. Prior to this, there had been continued disinflation in domestic prices and wages. CPI inflation will be higher in the near term as a result of the new shock to the economy.

Monetary policy cannot influence global energy prices but aims to ensure that the economic adjustment to them occurs in a way that achieves the 2% target sustainably. The MPC is alert to the increased risk of domestic inflationary pressures through second-round effects in wage and price-setting, the risk of which will be greater the longer higher energy prices persist. The MPC is also assessing the implications for inflation of the weakening in economic activity that is likely to result from higher energy costs.

The Committee will continue to monitor closely the situation in the Middle East and its impact on global energy supply and energy prices. It stands ready to act as necessary to ensure that CPI inflation remains on track to meet the 2% target in the medium term.

This is a huge shift from the Bank's previous stance, prior to the outbreak of war, which saw markets anticipating that the gradual downward trend in rates would continues.

Bloomberg produced this chart showing how inflation expectations changed at the BoE:

ECB: The ECB already has rates at 2%, and is expected to raise rates this year. According to Bloomberg, expectations are unchanged today: markets expect two rate increases of 0.25% each, with a 50% chance of a third such increase.

So the really big shift in direction is at the BOE.

All told, it's been a bad day for markets, and for humanity: war, higher energy prices, and higher interest rates in response to the first two problems.

That's it for today, thanks everyone. Spreadsheet accompanying this report: link.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

BP (LON:BP.). (£87.3bn | SR89) | Agreement to sell Gelsenkirchen refinery and related businesses to Klesch Group, an independent European refiner. Terms are confidential. bp's structural cost reduction target increases by around $1 billion to $6.5 to $7.5 billion by 2027. | ||

Investec (LON:INVP) (£5.26bn | SR64) | FY March 2026: The Group is expected to deliver a resilient performance. Adjusted EPS up 3% to 6% (81.6p to 84p). Basic EPS up 6% to 9% (76.9p to 79.2p). Adjusted operating profit before tax to be between £940.3 million and £965.9 million (FY2025: £920.0 million). | ||

IG group (LON:IGG) (£4.54bn | SR91) | Revenue +7%, or +6% organically. EBITDA +1%, adjusted EPS +5% (115.3p), supported by ongoing share buybacks. New £125m buyback. Outlook: The Group expects 2026 EBITDA broadly in line with current consensus of £538.1 million, assuming market conditions broadly consistent with 2025, and is comfortable with consensus adjusted EPS of 119.5 pence. | GREEN = (Graham) | |

Land Securities (LON:LAND) (£4.39bn | SR31) | 192,000 sq ft lease with bp for its office development at Timber Square, SE1. The lease covers the entire 15-storey Ink building, which will become bp's new global headquarters. Good customer interest in the remaining Print building. | ||

Grafton (LON:GFTU) (£1.74bn | SR91) | Agreement, subject to approval from the Spanish National Commission for Markets and Competition, to acquire the entire issued share capital of Mercaluz. Mercaluz is a distributor of domestic and commercial air conditioning equipment to professional SME installers. Total consideration €175m but is expected to be €165m on a cash and debt free basis. | ||

Energean (LON:ENOG) (£1.66bn | SR55) | Production in Israel is currently suspended following a government-ordered shutdown in response to the recent geopolitical situation in the Middle East. Average working interest production in 2025 was 154 kboed (85% gas) (the upper end of the revised guidance range of 145-155 kboed). Loss after tax $258m “is reflective of exceptional non-cash items”. 2026: Israel guidance suspended, Rest of Portfolio production guidance of 32-36 kboed remains unchanged. | ||

Atalaya Mining Copper SA (LON:ATYM) (£1.26bn | SR89) | FY25 copper production 51.1 kt, the higher end of the guidance range. EBITDA €179.8m, free cash flow generation €107.4m. “…while the start of 2026 has been affected by challenging weather conditions at Riotinto, we remain confident in our production guidance for the year and in the medium‑term growth potential of our portfolio.” | ||

Elementis (LON:ELM) (£870m | SR60) | The new non-Exec Chair has served as Non-Executive Senior Independent Director of Elementis since April 2022. New Independent NED appointed, previously CEO of Croda from 1999 to 2011. | ||

Gulf Keystone Petroleum (LON:GKP) (£466m | SR82) | Gross average production of 41,560 bopd, up 2% and towards the top end of guidance range. On 28 February 2026, the Shaikan Field was shut in as a safety precaution. 2026 production guidance under review. | AMBER/RED ↓ (Mark) | |

Picton Property Income (LON:PCTN) (£414m | SR69) | The Board has received proposals regarding the Strategic Review and Formal Sale Process from a wide range of interested parties and with a variety of structures. Progressing with a shortlisted number of these proposals. They have decided to delay the release of the Annual Results to a later date. | ||

DFS Furniture (LON:DFS) (£350m | SR93) | Revenue +8.6%, underlying PBT(A) £30.9m (up by £13.9m), reported PBT £30.3m (up by £14.5m). Net bank debt £60.6m (reduced by £56.1m). Since the half year we have seen some softening in footfall linked to adverse weather conditions… we are comfortable reiterating our guidance of full year PBTu(A) in the range of £43-50m (assuming no material supply chain disruption). | ||

Capital (LON:CAPD) (£313m | SR92) | Revenue down 0.6%, adjusted EBITDA +1.1% (£79.5m), operating profit +23% (£46.6m). Operational EPS 5.4 cents (down 11.6%), basic EPS 34.9p cents (up 325.6%). Outlook: Revenue guidance for FY 2026 of $410 - 440 million, representing a 23% increase on FY 2025 at the midpoint. | ||

Central Asia Metals (LON:CAML) (£301m | SR99) | Revenue +7% to $229.9m, EBITDA -1% to $101.8m, Cash $80.1m (FY24: $67.6m). Production guidance for 2026: Copper of 12,000 to 13,000 tonnes, Zinc-in-concentrate of 18,000 to 20,000 tonnes, lead-in-concentrate of 26,000 to 28,000 tonnes. Capex guidance for 2026 of between $14.5 million and $17.5 million, compared with $19.0 million spent in 2025. | ||

LSL Property Services (LON:LSL) (£232m | SR55) | Revenue +6% to £182.9m, U/L Op profit +17% to £32.6m, Net Cash £27.8m (30 Jun 25 : £22.0m), FY dividend held at 11.4p. Made a positive start to the year across the Group, with trading in our businesses in line with expectations. | ||

Smiths News (LON:SNWS) (£162m | SR99) | New contract with The Guardian is for all of Smiths News's current distribution territories in the UK through to 2031. | ||

Mkango Resources (LON:MKA) (£160m | SR19) | Songwe: Capex $326m, NPV10 $339m. Pulawy: Capex $212m, NPV10 $779m | ||

Afentra (LON:AET) (£152m | SR88) | Sonangol E&P, the operator of both blocks, has elected to participate in the acquisition of Etu's interests. Following this development, Sonangol, Afentra and Etablissements Maurel & Prom S.A. ("M&P") will jointly acquire Etu's 10% interest in Block 3/05 and 13.33% interest in Block 3/05A offshore Angola. | ||

Focusrite (LON:TUNE) (£117m | SR78) | Revenue expected to be slightly ahead of the prior 12 month period at approximately £164m (slightly below consensus). Operating margins stable due to cost control. Adj. EBITDA to be in-line with current market expectations (£9.4-£11.0m). Net debt £9.0m (31 Aug: £10.8m) | BLACK (AMBER/RED ↓) (Graham) | |

Strategic Minerals (LON:SML) (£113m | SR42) | £4.7m raised at 3.5p per share, a 16.7% discount to last night’s close. | ||

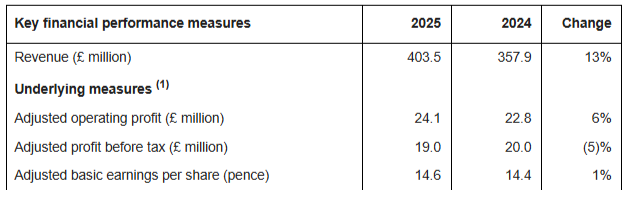

Eurocell (LON:ECEL) (£110m | SR77) | Revenue +13% to £403.5m (organic flat), Adj. PBT -5% to £19m, Adj. EPS +1% to 14.6p. Net Debt excl leases £22.1m (FY24: £3.1m). “Demand in the RMI market remains sluggish, and we are therefore continuing to focus on operational improvements and cost control. The potential impact of the evolving situation in the Middle East is difficult to assess at this time...” | AMBER/GREEN = (Mark) | |

InvestAcc (LON:INAC) (£82.3m | SR11) | Revenue +43% to £15m (+28% organic), Group EBITDA +52% to £4.3m. FY26 remains consistent with previous guidance. | ||

ECO Animal Health (LON:EAH) (£65.4m | SR97) | Revenue +8%, slightly ahead of market expectations, The combined effect of the stronger revenue and margins is expected to result in a material increase in adjusted EBITDA over the prior year with adjusted EBITDA also materially ahead of market expectations. | AMBER/GREEN ↑ (Mark) | |

Corcel (LON:CRCL) (£37.5m | SR8) | Raised £3.6 million through a subscription with a number of its existing strategic investors at £0.004 per share, in line with 15-day VWAP. | ||

Synthomer (LON:SYNT) (£29.4m | SR36) | SP +44% 2025 revenue of c.£1.74bn and continuing EBITDA in the range of £135-138m. Covenant net debt:EBITDA was 4.7-4.8x, well within the requirement of less than 5.25x, and liquidity was £385m. FY26 trading in line with the Company's expectations and momentum continues to build. Will pass on cost increases from Iran War. “...continues to explore options to support further leverage reduction and underpin the sustained delivery of the speciality chemicals strategy, the Board does not currently intend to issue new equity and is focused on concluding the debt refinancing process alongside the divestment programme.” | RED = (Mark) Overall, one line in an RNS doesn’t change our view that this is a high risk investment that may pay off if lenders keep the faith and the company recovers, but investors should be prepared to lose everything. Our negative rating reflects this continuing risk. | |

tinyBuild (LON:TBLD) (£24.8m | SR53) | Revenue +17% to $35.5m, Adj. EBITDA $5.6m (FY24: $6.1m Loss), Cash $4.6m (FY24: $3.1m). Remains confident the Company is on track to deliver results at least in line with expectations. | AMBER/RED ↑ (Graham) I think this is worth an upgrade to AMBER/RED. It’s still a stock that I’m worried about (but intrigued by). Overall, the performance in 2025 was much improved on 2024. It looks like it has the potential, maybe, to generate some cash. Probably not in the current year, given where EBITDA forecasts are sitting. But maybe in the year after? The worst might just be behind it. | |

Robinson (LON:RBN) (£19.3m | SR82) | Planning approval received for Walton Works where contract was exchanged in Aug 23. £617k now payable to Robinson vs 540k Book Value, used to reduce debt. | AMBER/RED = (Mark) [no section below] A small surplus to book value continues to outline the excess value that their property portfolio contains. However, the proceeds are being used to pay down debt (taken on to expand via acquisition and paying an uncovered dividend for a few years), and to create more plastic packaging, something the world is trying to rid itself of! Overall, this doesn’t change our view which was reduced following a profits warning late last year. | |

East Star Resources (LON:EST) (£17.6m | SR16) | Formalisation of the joint venture agreement where Xinhai" will farm into the Verkhuba Copper Deposit, and advance it into production. East Star fully carried to production with 30% holding. | ||

LMS Capital (LON:LMS) (£15m | SR64) | NAV per share -20% to 35.9p.Y/E cash £6.8m (23% of NAV). | ||

Nanoco (LON:NANO) (£11.3m | SR16) | Confirms that it has submitted a joint motion with Shoei to stay the ongoing litigation following a binding term sheet being agreed between the parties. No compensation will be payable by either party, and both parties will be responsible for their own costs incurred. | AMBER/RED = (Mark) [no section below] | |

Titon Holdings (LON:TON) (£9.6m | SR74) | H1 Revenue +3%. H1 softer than expected, but anticipates stronger H2-weighting to achieve full year revenue and profits in line with its expectations. | AMBER/RED = (Mark) [no section below] This is an in-line update but one that requires a strong H2 to make up for H1 weakness. This is rarely a good sign, and many investors see this is a precursor to a warning. Even if they achieve expectations, this trades on a forward P/E of over 100, and the broker is unwilling to commit to forecasts beyond this year. There remains a discount to TBV which may be attractive for some. However, with little sign that these assets will be productive anytime soon, it makes sense to remain broadly negative after this update. |

Graham's Section

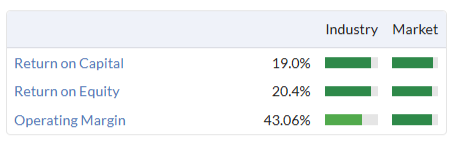

IG group (LON:IGG)

Up 4% to £14.20 (£4.8bn) - FY Results & Trading Update - Graham - GREEN =

(At the time of writing, Graham has a long position in IGG.)

IG has unfortunately changed its financial year-end, from May to December.

So this is a strange “7-month financial year”, the period from May 2025 to December 2025.

I tend to be critical of companies who do this, so I should make no exception for one that happens to be in my portfolio. IG say that the purpose of the change is “aligning our reporting calendar with common market practice”.

For the purposes of presenting today’s results, IG compare the calendar year 2025 against the calendar year 2024.

The headlines:

Revenue up 7%, or 6% organically.

Net trading revenue up 10%

EBITDA up 1% to £531m

EBITDA margin falls from 49.9% to 47.3%.

Adjusted EPS up 5% to 115.3p, “supported by ongoing share buybacks”.

There’s a new £125m buyback (takes out <3% of the shares at the current market cap).

The operational headlines include the acquisition of many low-value customers in Freetrade: active customers grew 174% to 742,000..

On an organic basis, which is the correct way to look at it, active customers increased 6%.

Strategic review: this is unexpected.

- IG operates in large, fast-growing markets being reshaped by structural drivers including technology and the convergence of trading, investing and gaming-adjacent experiences. Accelerating customer growth and record financial results highlight the strength of IG's platform. The Board is today announcing a strategic review to ensure IG captures the full long-term opportunity ahead.

- The review will evaluate routes to maximise shareholder value, including, but not limited to, acquisitions to accelerate growth, IG's domicile and listing venues to unlock capital and enhance strategic flexibility, and potential combinations of parts of the Group with other industry participants.

- The outcome of the review will be announced at a Strategy Update in autumn 2026.

I’m quite ok with this news.

Breon Corcoran has been CEO since January 2024. He set out various strategic targets in July 2024, and says that the company has delivered against them (“stronger customer acquisition, a growing active customer base, organic revenue growth in line with our medium-term guidance, strong cash generation and surplus capital”).

That being the case, it’s the right time to decide what the next set of objectives might be. Or in the words of Corcoran: their track record “gives us the confidence and platform to set bolder ambitions.”

I’m open to the company making more acquisitions, changing its domicile and listing venues (a US move?), or combining with others in the financial/gambling industries. Not that I’ll assume any decisions they make are the correct ones - but I have an open mind. IG has a lot of potential, and it’s worth exploring what the right way forward might be.

It’s worth highlighting that Corcoran was at the heart of the merger between Paddy Power and Betfair (now known as Flutter Entertainment (LON:FLTR)). Flutter is now the world’s largest online betting company, and the merger is generally recognised as being a success for all involved - including the shareholders of the companies involved.

Corcoran may be hoping for another successful mega-deal, or perhaps a series of strategic developments that would amount to the same thing.

This strategic review does introduce some new risks… but I would argue that it also increases the potential for significantly higher upside over the long-term. IG is 17% of my single-stock portfolio, having already multi-bagged for me, so I’ll have to keep this position closely under review.

Let’s get back to today's report. From the CFO:

2025 marked a step change in IG's financial performance, with record revenue, materially stronger customer acquisition and strong margins. Since joining in December 2024, I have seen first-hand how the investments we are making in product, culture and efficiency are driving results. We remain focused on delivering our strategy, confident this will broaden our addressable market and drive sustained earnings growth.

Although he says that margins were strong, they didn’t improve on the prior year. An explanation of higher costs:

The increase reflects targeted investment in marketing to drive customer acquisition, and in strategic initiatives to position the Group for its next phase of growth.

On profit margins:

The Group continues to prioritise revenue growth over near-term margin expansion, reinvesting efficiency savings into product, technology and marketing.

Without wishing to be blasé about this, I think shareholders can afford to be relaxed about the lack of short-term progress on margins. The company is in a position of great strength when it comes to profitability:

Trading update for February 2026:

Trading in the period was encouraging, with accelerating customer acquisition, growing assets under administration and further progress broadening the product offering.

Organic revenue is flat, while net trading revenue grew 4% organically. I should have mentioned already that declining interest rates are a drag on revenue - as a financial business. IG reports most of its interest income within revenues. Year-on-year, net interest income has fallen 16% as interest rates have declined.

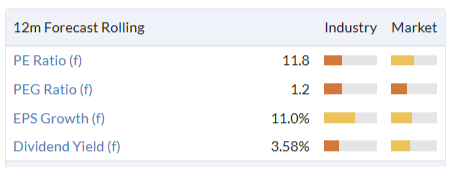

Graham’s view

I’d better wrap this up here, but clearly I remain a huge fan of this business.

I’ve been GREEN on it (e.g. in December) and the market cap has grown considerably even since then: from £4.0bn to £4.8bn.

At some point, I might have to adjust my stance lower on valuation grounds. But I’m not sure we are there yet:

I also note the StockRank of 91.

In general, we stay positive on companies that are performing well, even if their share prices have already risen considerably, unless perhaps if the overvaluation has become extreme. The trend is your friend, after all (until it ends).

So I’m leaving this on GREEN.

tinyBuild (LON:TBLD)

Up 7% to 6.7p (£26m) - FY 2025 results ahead of expectations - Graham - AMBER/RED ↑

tinyBuild (AIM:TBLD), a premium video games publisher and developer with global operations, is pleased to announce its audited results for the twelve months ended 31 December 2025.

tinybuild’s games may be “premium” but they are also considered “indie”, due to the size of the publisher.

This 2021 vintage IPO has been something of a financial car crash in recent years:

But let’s see if today’s results are as good as the RNS headline suggests.

Revenue +17% ($35.5m)

Adjusted EBITDA $5.6m (previous year: $6.1m loss)

Operating loss $2.8m (previous year: $20.1m loss).

We’ll have to investigate this gap between adjusted EBITDA and the operating loss.

Before then, the operational news:

Own-IP responsible for 86% of revenue (up from 77%), “primarily due to the success of Deadside release on console”.

Back catalogue stable at 88% of revenues.

New titles launched: “The King is Watching, FEROCIOUS, Kill it with Fire 2 plus additions to catalogue titles such as version 1.0 of Drill Core, the console launch of Deadside, and physical Switch editions for Graveyard Keeper and the Hello Neighbor published by Atari.”

New games announced: “Hozy, Restory, The Lift, SpeedRunnners 2 and Trainfort, plus SAND for console, and numerous playtests, demos and prototype 2 for Hello Neighbor 3.”

Outlook: “on track to deliver results at least in line with expectations”.

Commentary strikes me as a little cautious:

2025 saw a strong EBITDA performance, but uncertainty remains in a crowded market (c. 20,000 games were released in 2025, 8% more than in 2024).

The pipeline includes a number of high-potential games; the strong 2025 gives management greater flexibility both in terms of development budget and release schedule to achieve the full potential for each title.

CEO comment:

"tinyBuild bounced back strong in 2025 creating new franchises, relaunching catalogue titles to new highs and doubling down on the strength of our pipeline: we now have 7 titles on the Steam Top200 Wishlist chart, a new record. I really need to thank our people, in all geographies, for these amazing results achieved in a challenging environment."

"The industry backdrop is slowly improving and we start to see the fruits of our strategy to invest cautiously in own-IP with a diversified approach of higher and lower budget titles. More to come in 2026 and beyond."

Mr. Nichiporchik is a 58% shareholder here, which is the main reason for my interest in the company: with such a high level of alignment between the CEO and other shareholders, I’m intrigued to see if he can help to steer it to success.

CFO Grant: last month, the company granted options over 6.3m shares to its CFO. This a former equity research analyst who became Head of M&A at tinyBuild in 2021. It’s a pretty valuable award ($0.6m) considering the size of the company, and the lack of profitability.

Analysis of losses: in the bridge from positive adjusted EBITDA of $5.6m to the loss from continuing operations of $3.4m, there are two main items: amortisation ($3.1m) and impairments ($7.2m).

I think I can get behind some of these adjustments, but I can’t get behind this item:

During 2025, the Group recorded impairment losses of $3,927,000 (2024: $13,663,000) against the carrying value of software development costs.

This impairment arose from the company spending on software development, and then realising it wasn’t going to make the expected return on this spending. I don’t see why this should be adjusted out, as it’s just ordinary development spending that hasn’t generated a return.

The other items are more of a judgement call, with better arguments for adjusting them out.

So in my world, the “real” adjusted EBITDA number is probably still positive, but not by much.

Cash at the end of the year was $4.6m (prior year-end: $3.1m). The cash inflow from operating activities was $12.7m ($6.3m in 2024), while software development costs decreased to only $11.8m ($19.3m in 2024).

Looking ahead, the cash balance “is anticipated to reduce towards the spring as the Company continues to invest in a disciplined manner in upcoming game releases”.

Estimates from Zeus (many thanks).

These are unchanged:

2026 revenue £40.7m, adj. EBITDA £4.3m

2027 revenue £44.6m, adj. EBITDA £7m.

Note that adj. EBITDA is expected to reduce in the current year, before rising again.

Graham’s view

I think this is worth an upgrade to AMBER/RED. It’s still a stock that I’m worried about (but intrigued by).

Overall, the performance in 2025 was much improved on 2024. It looks like it has the potential, maybe, to generate some cash. Probably not in the current year, given where EBITDA forecasts are sitting. But maybe in the year after? The worst might just be behind it.

From a balance sheet point of view, there is still zero tangible asset backing.

Overall, I’m still very cool on this one. But I think RED would be overly negative, given that it should not suffer financial distress in the immediate future, and given how much better 2025 was compared to the prior year.

2-year chart:

Focusrite (LON:TUNE)

Down 1% to 195.5p (£116m) - Trading Update: Trading in-line with expectations - Graham - BLACK (AMBER/RED ↓)

Focusrite plc (AIM: TUNE), the global music and audio products group supplying hardware and software used by professional and amateur musicians and the entertainment industry, provides the following update on trading ahead of its results for the 18 month period ended 28 February 2026.

Another change in year-end situation here.

Focusrite has two divisions: Content Creation (music-making equipment direct to consumer) and Audio Reproduction (music delivery equipment for businesses).

The company helpfully provides us with 12-month analysis:

Revenue for the 12 months to Feb 2026 “slightly ahead” of the prior year at c. £164m.

Gross margins “strong and slightly ahead of the prior 12 months”.

Operating margins “also expected to remain stable”.

Thanks to the above, adj. EBITDA for the 12 months is expected “in-line with current market expectations”.

These expectations, as provided by Focusrite, are for adj. EBITDA of £23.7 to £25.3m.

Six-month analysis: the six months to Feb 2026, which is now an H2 period of sorts, saw revenue fall 5%, reflecting “a particularly strong comparator for the Content Creation division” (tariff-related: demand pulled forward in 2025 ahead of tariff increases).

Net debt: falls from £10.8m (August 2025) to £9m (Feb 2026).

CEO comment:

"While geopolitical developments in the Middle East and macroeconomic uncertainty continue to create volatility in global markets, the Group has not experienced any material impact to date. The situation continues to be monitored closely…”

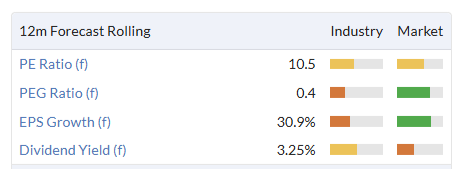

Estimates: thanks to Cavendish for posting on this today.

Although adj. EBITDA is in line for FY26, revenue has missed by 1%.

This feeds through to a lower revenue assumption for FY27 (reduced by 1% £170.6), and in turn a 5% reduction in the adj. PBT forecast for FY27 (to £15.8m).

Graham’s view

I don’t think this is a bad business, and AMBER/RED might be a little harsh, but it seems that the profit outlook probably has deteriorated a little bit, even if this is not explicitly stated in the RNS.

It’s worth mentioning that Cavendish are not listed as a broker to the company, but they do publish on it and I do respect their forecasts on the stock.

Therefore, I’m putting this temporarily on AMBER/RED, as we should in general downgrade stocks where the outlook has deteriorated or forecasts have been missed.

The change in year-end has also bothered me a little (see comments here).

Perhaps it could offer some value for the patient, who are willing to look past these small objections:

Mark's Section

Gulf Keystone Petroleum (LON:GKP)

Up 6% at 226p - Full Year Results - Mark - AMBER/RED ↓

The production figures were already known, following the Operational Update on 22 January:

Gross average production of 41,560 bopd, up 2% relative to the prior year (2024: 40,689 bopd) and towards the top end of tightened 40,000 – 42,000 bopd guidance range

At the time, they said:

Production expected to ramp up towards 44,000 bopd following the recent restart of a well post jet pump replacement and the completion of ongoing well workovers

But they then said that they had “temporarily shut-in production operations and has taken measures to protect staff in light of the developing regional security environment” on 2 March. Today, it is confirmed that operations remain shut in and that they are reviewing their previous 2026 production guidance.

They say, “The Company is ready to restart production and exports quickly with an improvement in the security environment”, and the good news is that sales go to local oil refineries in Iraq and to the recently reopened pipeline into Turkey. They are not reliant on the Straits of Hormuz for export.

While a direct strike on the Sheikan field seems unlikely, the idea is perhaps less far-fetched than it was a few months ago. The Independent reported on Wednesday that:

Drones targeted oil fields in Iraq’s semi-autonomous northern Kurdish region Wednesday, the latest in a series of attacks in recent days that have put several oil facilities out of commission.

DNO’s Tawke field saw storage tanks hit. Sheikan’s neighbour, the Baadre field operated by Hunt Oil, was set ablaze. Perhaps most worrying is that no one has claimed responsibility for these attacks, which could well continue even if the war with Iran ends.

Even without a direct hit to Sheikan’s oil infrastructure, there remain two huge unknowns:

When will the security situation be suitable to restart production?

Will the Kurdistan/Iraqi government be in a position to pay them on any restart?

They will presumably still be paid cash on delivery for local sales, but the payment they receive here seems to be unlinked to global oil prices. So it is a bit of a mystery to me why the share price has been so strong recently. It seems to me that investors have bought into the sector, but missed the key point that they are unable to take advantage of that strong commodity pricing because they are not producing. If the Iran situation is resolved to the point that the company can restart production, oil prices will be much lower. If they resume exports, the political challenges of how they get paid and by whom could be exacerbated by the increased regional unrest. There are reports of increasing tensions between the Iraqi and Kurdistan governments.

One factor that is helping is that the company maintain a brave face is that they have significant cash balances:

2025 year-end cash balance of $78.2 million (31 December 2024: $102.3 million) and no debt. Cash balance as at 18 March 2026 of $89.1 million reflecting consistent payments for exports sales in the year to date.

And hence have decided to keep paying a dividend:

The Board has carefully considered these factors, the current security outlook, the Company’s debt-free balance sheet and ability to reduce capex and costs. Consequently, it has decided to declare an interim dividend of $12.5 million, equivalent to $0.0575 per Common Share

This indicates a certain amount of confidence from the board that this disruption will be short-lived. However, it is worth noting that the dividend payment is half of the $25m they paid in both September and April last year.

Mark’s view

We have been consistently AMBER here, recognising the strong cash flow and the willingness to return it to shareholders, while balancing this against the inherent risks. Those risks are underlined by recent events, which mean that the company is not producing oil amid exceptionally high global oil prices. With neighbouring oil fields being hit by multiple drone strikes without any parties claiming responsibility, it is not clear to me that there will be any swift return to production even if the initial conflict is resolved.

In situations like this, I often say the market hates uncertainty and has overreacted to risky events. However, in this case, the market seems to have under-reacted. Shareholders appear to have focused on a dividend payment that won’t be continued in the short term unless production restarts soon. They seem to have missed that the company is unable to produce oil to take advantage of recent high prices, and we have no idea when they may be able to again.

I get that many will want commodity exposure in current markets, but if investors want commodity upside, there are plenty of current producers unaffected by recent events, yet the market is pricing them as if oil will be back below $70 by the end of the month. In contrast, I can’t help feeling that Gulf Keystone has the worst of both worlds - no production while the oil price is high, and a return to normality, only if the oil price is low again. Hence, I am reducing our view to AMBER/RED.

Synthomer (LON:SYNT)

Up 44% to 26p (£43m) - Trading & Refinancing Risk - Mark - RED

The share price has soared this morning on the news that they currently do not intend to issue new equity. Their previous statement on 22 Feb saying that they were considering a capital raise to support debt refinancing due next year, caused a 50% drop in share price. So a partial recovery is perhaps understandable.

However, the scale of the debt to EBITDA ratio, shows things are far from ok.

As we highlighted on the DSMR in December, their largest shareholder had to step in with additional off-balance sheet receivables financing to make sure they were compliant with their covenants, and this is not included in these debt figures.So there is still the risk that lenders demand a debt-for-equity swap as part of the refinancing and take control, whether the company intends it or not.

The best outcome here is probably that they manage to divest more businesses to pay down debt and satisfy their lenders in order to refinance without dilution. This will be a key aspect to watch going forward. However, this is one area which may be impacted by negative market sentiment following the Iran War.

Overall, one line in an RNS doesn’t change our view that this is a high risk investment that may pay off if lenders keep the faith and the company recovers, but investors should be prepared to lose everything. Our negative rating reflects this continuing risk.

Eurocell (LON:ECEL)

Flat 111p - PRELIMINARY RESULTS - Mark - AMBER/GREEN =

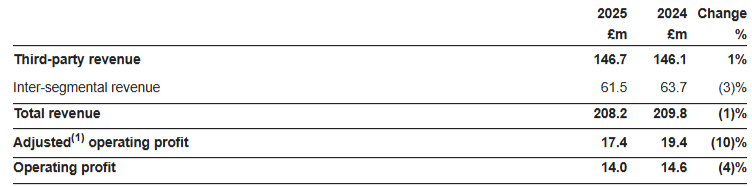

Revenue is up 13%, but that's entirely due to the Alunet acquisition. Organic sales are flat on volumes down 2%. That acquisition hasn’t led to improving profitability either:

Segmental Reporting:

Looking at their divisions, they effectively bought in £4.8m of Operating Profit from acquiring Alunet, but this was more than offset by declines in their other divisions. Profiles had an ok year, given market conditions, with adjusted operating profit only down 10%:

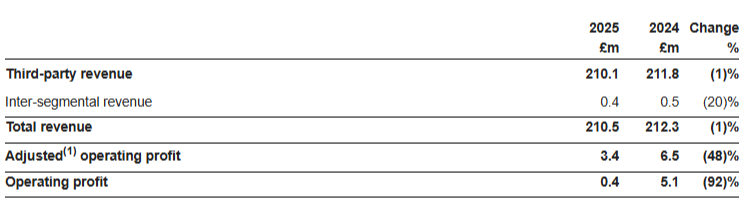

However, profitability in their Branch Network declined significantly:

Adjustments:

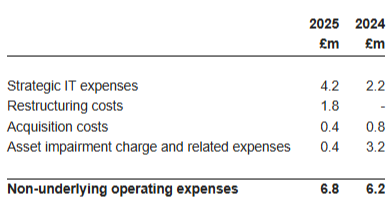

Both divisions saw significant adjustments, attributed to strategic IT projects and restructuring costs.

Restructuring should be a one-off, but a quick look back at prior results shows that they adjusted out £2.7m in FY23 and £1.6m in FY22 for this. It seems we really should be viewing the zero restructuring charge in FY24 as the one-off!

I also disagree with their continued expectation that we ignore IT spend just because they describe it as “strategic”. I’m pretty sure they are not going to adjust out any benefits they claim from new IT systems as “exceptional”.

Forecasts:

Mere mortals can’t see the research on this company, so we are flying slightly blind. On the surface, revenue comes in line, but EPS is a slight miss versus the 15.1p consensus in the StockReport. However, this appears to have been upgraded recently, while FY26 was downgraded, so I wouldn’t read too much into this:

Cash flow

Things are better on a cash basis with net cash generated from operating activities of £48.4m, up 10% vs 2024. £3.7m of this came from working capital. However, this excludes lease payments of £19.3m split across principal and finance costs.

Net debt excluding leases increased by £19m, partly due to £20.6m spent on Alunet. Overall, this means that free cash flow only just covered the £6.2m dividend plus £5m buyback during the year.

Their current buybacks finished in February, and they say they “Intend to continue share buybacks, assuming no prolonged impact from the situation in the Middle East and subject to maintaining a strong financial position.” However, there is no firm commitment in these results.

Better news on the dividend: it is increased by 5%, which means they yield around 6%.

Outlook

This reads as pretty downbeat to me:

Demand in the RMI market remains sluggish, and we are therefore continuing to focus on operational improvements and cost control. The potential impact of the evolving situation in the Middle East is difficult to assess at this time, but the medium and long-term prospects for the UK construction market remain attractive and we are well positioned to drive sustainable growth in shareholder value.

I agree that, long-term, the UK housing market should see growth again. However, it is clear that higher inflation and rates have the power to delay this out further into the future than we would have expected at the start of this year.

Valuation

If we believe the current forecasts and accept the adjustments, then this looks very cheap:

However, both of these have challenges. I think their adjustments are a little aggressive, and the outlook has materially worsened over the past few weeks.

We have to remember that even if forward earnings are not quite as good as they first appear, these will be closer to a cyclical low than a cyclical high. This sort of rating also has some significant leeway in it.

Mark’s view

It is clear that the sector is a tricky place to be at the moment, and the outlook has worsened given the fallout from the Iran War. These results are a bit meh, but then we should expect them to be at this point in the cycle. Given all this uncertainty, I can understand why many will want to step aside for now and wait for signs of green shoots. However, for those with a longer mindset, the valuation still looks very cheap, even if one takes a more conservative view on adjustments and forecasts. Investors get a 6% yield to wait for any recovery that may arrive. Overall, I struggle to be too negative on a stock on this rating at this point in the cycle, so I will keep our broadly positive view of AMBER/GREEN.

ECO Animal Health (LON:EAH)

Up 6% at 102p - Full Year Trading Update - Mark - AMBER/GREEN ↑

When Graham reviewed their H1 results, he was a little confused. They said H1 was “ahead of guidance", but the full-year outlook was line, implying either that they are being conservative or that the outlook for H2 FY2026 isn't overly strong.

It turns out that they were being conservative:

The combined effect of the stronger revenue and margins is expected to result in a material increase in adjusted EBITDA over the prior year (2025: £7.3m) with adjusted EBITDA also materially ahead of market expectations.

Revenue growth was slightly ahead of guidance at +8%, so margins have done the heavy lifting, driven primarily by improved product pricing and cost of goods. It’s not clear how repeatable this will be.

Forecasts

Their broker, Cavendish, put some numbers to this, raising revenue forecasts by 4.1% and adjusted. EBITDA by 13.7%. I may be nitpicking here, but normally “materially ahead” means 20% or more, whereas I have noticed a trend toward companies being much more aggressive with their language recently. (Perhaps they have been reading Ed’s research into “The Drift”!)

The good news is that this momentum is viewed as more than a one-off, and Cavendish raises FY27 EBITDA by 9.4% and FY28 by 2.8%. The bad news is that the net result is they only have single-digit EPS growth forecast and are trading at a P/E of over 20. They may just be being conservative again, though.

Things look better on an EV basis, with their forward EV/EBIT around 8. However, it is worth noting that a significant portion of their cash is in China and may be difficult to access at the corporate level.

Mark’s view

I still have a few concerns about the accessibility of cash in China and whether they are over-egging the pudding with the language used in this update. However, there is no doubt that this is good news, and the company has positive momentum in both its share price and trading. The valuation is modest, at least on an EV basis, and there is some blue-sky potential in the vaccines they have been developing over the last few years.

With a StockRank of 97, I feel we should be taking a more positive view of AMBER/GREEN.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.