Good morning!

I was sorry to see that the comments section on Friday degenerated into hostility.

The FTSE is down by 7% over the past month, which never helps, and the news has been rather bleak at times. But despite all of that, I think that the atmosphere here has generally remained very positive. Let's keep it that way.

Cheers,

Graham

Monday market open: over the weekend, Trump threatened to blow up Iran's power plants if the Strait of Hormuz does not reopen tonight (by 7.44pm New York time, to be precise). Meanwhile, Iran has said that it will close the Strait "completely" if its power plants are attacked. The Speaker of Iran's Parliament has also threatened financial entities that buy US treasury bonds ("Purchase them, and you purchase a strike on your HQ and assets").

With this frightening rhetoric as backdrop, the FTSE is set to open lower by another 130 points, at 9780.

11.45: Goodwin gets the prize for the worst RNS of the day, issuing what amounts to a profit warning at 9.19am. The RNS even began with the phrase "It is encouraging that the Group's trading performance remains in line with expectations..." before delivering the bad news. Bad luck for anyone who was buying this at 9am!

2.30pm: wrapping this up now, thank you. Trump has said that both sides (US/Israel-Iran) are keen to make a deal, although the Iranians don't seem to agree. Either way, Trump's words had the effect of massively calming the market turmoil, and the FTSE is now up for the day - there has been a rapid 300-point reversal. A small win for the optimists!

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

GSK (LON:GSK) (£79bn | SR92) | B7-H3-targeted antibody-drug conjugate risvutatug rezetecan has been granted Orphan Drug designation for small-cell lung cancer in Japan. Supported by early clinical data showing “durable responses in certain types of” SCLC. | ||

| Goodwin (LON:GDWN) (£1.7bn | SR53) | Trading Update | SP -30% Goodwin reports disappointing outcomes from two “significant tenders” where it lost a €18m radar antenna bid and “unexpectedly lost” a >£45m tender with Sellafield. The company also advises that it has been asked to delay various shipments to the Middle East, which could affect revenue timing. | BLACK? (AMBER/RED ↓) (Roland) While Goodwin doesn’t provide forward profit guidance, the totality of today’s update suggests to me that profits are likely to be lower than might otherwise have been expected for FY27, if not for the current year (y/e 30 April). My estimate suggests the current valuation could still be quite demanding, so without any clarity on guidance I have decided to adopt a cautious view ahead of further news. |

Thungela Resources (LON:TGA) (£1.01bn | SR99) | Revenue down 2% to R4.0bn with net loss of R7.1bn. Export saleable production up 1% to 17,838kt. | ||

Spire Healthcare (LON:SPI) (£765m | SR42) | Discussions relating to a possible offer for the company with both Bridgepoint and Triton have now terminated. The Board remains in discussions with other parties in relation to a potential sale of the company and is continuing to actively evaluate “other appropriate actions” to drive shareholder value. | PINK (AMBER/RED =) (Roland) While macro conditions may not be helping, I speculate that one reason why Spire’s board may be struggling to find a buyer is that its valuation expectations are too high. As far as I can see, this business is highly leveraged, not very profitable and has poor visibility on revenue from its largest external customer (the NHS). | |

PPHE Hotel (LON:PPH) (£700m | SR47) | PPHE has secured a new £136.45m debt facility with an initial two year term to fund the acquisition of Park Plaza London Waterloo for £147.9m. The new facility has a floating interest rate that will be c.90% hedged. The cost of servicing this loan is expected to be lower than the previous lease liability on this hotel. | ||

Cohort (LON:CHRT) (£584m | SR31) | Cohort’s EM Solutions subsidiary has been awarded a contract valued at AU$21.7m from the Portuguese Navy for Cobra and King Cobra satellite communications terminals. Delivery will take place over the period to 2030. | ||

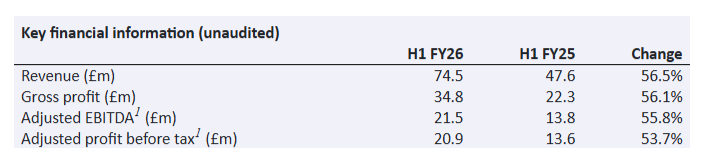

Applied Nutrition (LON:APN) (£553m | SR48) | Revenue up 56.5% to £74.5m, adjusted pre-tax profit up 53.7% to £20.9m, ahead of management expectations. Outlook: FY revenue of c.£140m, in line with previous guidance. Greater H1 revenue weighting than previous years. Expect some reduction of volumes into the Middle East due to current shipping disruption. | GREEN ↑ (Graham) Earnings per share growth from FY25 to FY26 is expected to come in strong (as high as 25%), but then maybe only 11-12% the following year. That takes the PEG ratio much higher (i.e. suggesting that the stock could be overvalued). But then, the PEG is not the only metric worth looking at. Higher-quality businesses deserve higher PEGs, in my view. Applied Nutrition is doing what I always hoped Science in Sport (SIS) would do for its investors. I’m taking this back to GREEN. | |

ME International (LON:MEGP) (£516m | SR n/a)(currently suspended) | Revenue up 3% to £315.4m, pre-tax profit up 7.1% to £78.2m. Adj EPS up 5% to 14.91p, in line with consensus. Dividend up 10% to 8.64p + £18m buyback. Outlook: year-to-date performance is in line with expectations. Mgt expects to apply for share suspension to be lifted shortly. | AMBER/GREEN ↑ (Roland) Today’s results show a strong performance with excellent profitability, but also disclose a rather disappointing accounting error that appears to date back two years. The shares remain suspended due to the late delivery of these accounts, but this aside, my view is that today’s numbers show a good, cheap business. With the caveat that the valuation could change suddenly when the stock returns from suspension, I am tentatively moving my view up by one notch today. | |

Caledonia Mining (LON:CMCL) (£310m | SR91) | Blanket gold production down 0.6% to 76,213oz, within guidance range. Bilboes gold production of 1,683oz (FY24: 1,645oz). Avg realised gold price up 55% to $4,057/oz. Pre-tax profit up 87.5% to $14.1m. 2026 outlook: expect Blanket gold production of 72-76.5koz. | ||

Public Policy Holding (LON:PPHC) (£275m | SR39) | Agreed to acquire PR firm Westminster Policy Partners Limited. WPI generated net revenue of £2.45m over the year to Jan 26. WPI will become part of Pagefield Group. | ||

Sylvania Platinum (LON:SLP) (£225m | SR96) | Launching $2m share buyback, as per guidance in recent results. | ||

Optima Health (LON:OPT) (£161m | SR66) | The existing CFO is leaving in July 2026. An interim CFO is named. | ||

Savannah Resources (LON:SAV) (£121m | SR33) | DFS and RECAPE (environment licence compliance process) are now expected to be completed in July 2026 (previously H1 2026). Expects to receive final environmental licence in Q3 2026 and reach FID before the year end. 2028 production guidance reiterated. | ||

Jubilee Metals (LON:JLP) (£100m | SR22) | Proposal to reduce share premium account to increase the amount of distributable reserves available. The company also plans to release phase 1 drill results for the Molefe Mine on Tuesday 24 March 2026. | ||

Distribution Finance Capital Holdings (LON:DFCH) (£95m | SR59) | SP -2% Loan book +27%. Revenue +19%. Net interest margin 8% (2024: 7.9%). Adjusted PBT +26% (£18.1m). The Group reaffirms its confidence in the previously announced medium-term strategic outlook. | GREEN = (Graham) [no section below] We already covered DFCH's full-year trading update here. Today's results confirm very strong growth rates across the majority of metrics, and I note in particular the improvement in adjusted return on tangible equity, from 9.9% to 11.9%. Tangible NAV per share rose by an impressive 12.1p to 75.9p, with the current share price being a 27% discount to that figure. A note from PanLib today says that DFCH beat its adjusted pre-tax profit estimate (£18.1m vs. £17.5m forecast) and argues that profits can more than double by 2030. Their unchanged estimates include underlying EPS of 8.6p this year and 10.6p next year. I continue to find this one very intriguing given the modest earnings multiple, discount to tangible book and growth prospects. The usual disclaimers apply when considering any small lender: it can be difficult to understand the risks from the outside | |

Naked Wines (LON:WINE) (£45m | SR85) | £1m buyback “reflects the Board's view that shares will be purchased at prices well below their intrinsic value, thereby increasing intrinsic value per share for all remaining shareholders”. | ||

Zenith Energy (LON:ZEN) (£38m | SR43) | Construction of ZEN’s 7 MWp solar plants in the Puglia region now scheduled to commence in early July 2026. With grid connectivity fully secured and construction financing now in place, Zenith has successfully de-risked the development phase of the project and is positioned to rapidly advance into construction. | ||

Quadrise (LON:QED) (£30m | SR5) | H1 FY26 loss after tax of £2m (H1 2025: £1.7m). Cash balance £4m as of Dec 2025. “The progress made during the period leaves Quadrise better positioned for commercialisation.” | ||

Predator Oil & Gas Holdings (LON:PRD) (£27m | SR16) | Cumulative gross oil sales for February US$337,071. Forecast March oil sales price expected to be 25 to 35% higher. Aggressive back-to-back drilling programme being evaluated to increase production coinciding with oil price spike. | ||

Great Southern Copper (LON:GSCU) (£18m | SR3) | High-grade Ag-Cu+Pb-Zn intersected in all RC holes with silver grades up to 105 g/t Ag. “These important scout RC drill results have been highly successful in demonstrating that high-grade silver-base metal mineralisation extends at least 1.5 kilometres south of the Mostaza mine…” | ||

Metals One (LON:MET1) (£18m | SR5) | Metals One is to secure 30% ownership of Lions Bay Resources PTY Ltd (LBR) through conversion of US$1.8m convertible loan notes. LBR's plan to acquire the assets of Vantage Goldfields from Business Rescue has been agreed by the Business Rescue practitioner. Vantage holds mining leases in the Barberton region with a historical resource inventory of 4.5 million ounces of gold. | ||

RTC (LON:RTC) (£13m | SR98) | Revenue £95.5m (2024: £96.8m). Profit from operations maintained at £2.5m. MAV per share 65p. Despite these challenging market conditions, 2026 has started positively and the underlying drivers of demand, especially across our infrastructure focused business, remain strong. | ||

Quantum Helium (LON:QHE) (£12m | SR20) | Total gross oil production of 11,769 barrels in 2025. Ongoing oil sales generating revenue to support helium exploration and development. “Now positioned to enter a highly active period with the planned extended production test at Sagebrush-1.” | ||

Orcadian Energy (LON:ORCA) (£12m | SR14) | Three-year extension to the Second Term of the Pilot Licence. Cash position £320k. Funding via CLN investors. In-principle agreement to issue royalties in return for cash. | ||

Cordel (LON:CRDL) (£11m | SR16) | Major V3 upgrade of its flagship "Cordel Connect" platform. | ||

Blackbird (LON:BIRD) (£10m | SR3) | Revenues down 14% to £1.38m. Adjusted EBITDA loss reduced to £1.67m (£2024: loss of £2.14m). Blackbird continues to operate in line with expectations and, via an OEM, was successfully used at the recent winter games in Cortina. The Company expects the division to again be profitable in 2026 through a focus on customer success and retention. | ||

Pennant International (LON:PEN) (£10m | SR19) | 2025 was a “reset year”. Revenues fell to £9.7m (2024: £13.8m). Adjusted EBITDA loss £0.4m. Net debt of £0.5m. "Supported by the structural savings delivered through the FY24-FY25 restructuring programme, we anticipate a return to a break‑even adjusted PBT in FY26 and have confidence in delivering on market expectations for the year." | ||

Tandem (LON:TND) (£9m | SR93) | Revenue +6%. Underlying PBT £692k (FY25: £510k). Reinstatement of dividend (3p). Net debt reduced to £1.9m. Notwithstanding continued market volatility, trading momentum entering 2026 has been positive, with early sales performance tracking in line with the Board's expectations and providing a constructive start to the new financial year. | AMBER/GREEN = (Graham)

I’m sorely tempted to upgrade this Birmingham-based bikes and toys group back to GREEN. The Tandem balance sheet has never been as strong as it is today. With net assets of £20m+, including freehold property, I personally struggle to see how the company could be undervalued at the current level. However, there are some reasons why this is foolish. Tandem has been consistently inconsistent, with periods of good performance almost inevitably followed by disappointment. Bad weather, fickle consumer tastes, Chinese logistics/shipping issues, and a wide variety of other unpredictable factors can ruin the party. I’m therefore going to leave this on AMBER/GREEN. It really ought to be GREEN, but based on my experience I just can’t quite bring myself to give it an upgrade. |

Graham's Section

Tandem (LON:TND)

Up 6% to 176.9p (£10m) - Final Results - Graham - AMBER/GREEN =

The Board of Tandem Group plc (AIM: TND), designers, developers, distributors and retailers of sports, leisure and mobility equipment, announces its audited results for the year ended 31 December 2025 ("FY25").

On a day when most shares are down, this Birmingham-based business is doing very well.

We already had a trading update from the company last month, which indicated there would be 6.2% revenue growth and adjusted PBT “slightly ahead of market expectations”. I looked at it here.

Even after today’s gains, the share price is lower now than it was after that February trading update - which says to me that the attitude of investors here remains fairly cautious. Of course, at this sort of market cap, only one determined buyer or seller is needed to change things!

Let’s figure out the key messages from these results. Some highlights:

Bike revenue growth 37.5% to £10.2m (notoriously volatile demand here)

Toys, Sports & Leisure revenue down 17.5% to £10.2m, “reflecting softer demand across certain discretionary categories, changes in retailer purchasing patterns and the timing of product ranging and promotional activity”.

There was good growth in the two smaller categories: Golf (+8.6%), and Home & Leisure (+30.1%), with “record heatwaves that boosted demand across key sales periods”.

Gross margin: up by over 100 basis points to 31.1%.

Underlying PBT: £692k (previous year: £510k).

Reported PBT: £568k (previous year: £30k) - a nice clean conversion from underlying to actual PBT.

Dividend: 3p proposed. This is the first dividend since 2023 and I’d say it’s a pretty big statement of confidence.

The dividend proposal is “in light of the Company's improved financial performance and strengthened cash flow position”.

Outlook

Notwithstanding continued market volatility, trading momentum entering 2026 has been positive, with early sales performance tracking in line with the Board's expectations and providing a constructive start to the new financial year.

In Toys, Sports & Leisure, 2026 will see them producing goods branded with Toy Story, Dora (the Explorer?) and Marvel Avengers. Sounds good. They’ll even have a “K-Pop Demon Hunters” wheeled product - I hope I can keep it out of my house.

Existing intellectual properties they use include Disney's Stitch, Bluey and Hot Wheels.

It’s impressive stuff and should be very profitable - but the shareholder returns never quite seem to match the promise.

Graham’s view

My view is pretty clear: I feel this business should have achieved more for shareholders over the years. For a business that has been publicly listed for over 30 years, a £10m market cap is a verdict in itself on what has been achieved.

I personally owned this one for a long time, before eventually moving on.

Having said that, I do think this latest set of results is pretty decent.

I’m very impressed by the lack of exceptional costs: only £87k in 2025 (previous year: over £400k).

And while I do feel that the company has failed to “compound” profits like it should have over the years, it has at least managed to convert its intermittent profitability into a gradually improving balance sheet.

Today’s balance sheet has been boosted by the “revaluation of property plant and equipment” (an irregular item that shows up on the statement of comprehensive income, not the P&L).

The result is the balance sheet equity has increased year-on-year from £24m to £26m.

Tangible net assets are £20.6m, or twice the current market cap.

Net debt is £1.9m but with this sort of asset backing, it shouldn’t be a concern.

The real difficulty is unlocking the £20m+ value for shareholders. If this value sits inside a mediocre business long-term, what’s it really worth?

On the other hand, the return of dividends suggests that value will start making its way back to shareholders now.

Indeed, there was a 12-year period when this company never missed a dividend payment. Culturally, under previous management, Tandem always thought the dividend was important.

I’m sorely tempted to upgrade this back to GREEN. The Tandem balance sheet has never been as strong as it is today. With net assets of £20m+, including freehold property, I personally struggle to see how the company could be undervalued at the current level.

However, there are some reasons why this is foolish:

Tandem has been consistently inconsistent, with periods of good performance almost inevitably followed by disappointment. Bad weather, fickle consumer tastes, Chinese logistics/shipping issues, and a wide variety of other unpredictable factors can ruin the party.

In general, a £10m market cap is a risk factor, due to the potential for a delisting.

The company in general hasn’t allocated capital well, and hasn’t earned attractive ROCE or ROE.

I’m therefore going to leave this on AMBER/GREEN. It really ought to be GREEN, but based on my experience I just can’t quite bring myself to give it an upgrade.

10-year chart:

The StockRank is 93; it’s a Super Stock.

Applied Nutrition (LON:APN)

Down 8% to 203.5p (£509m) - Interim Results - Graham - GREEN ↑

Applied Nutrition plc (LSE: APN), a leading sports nutrition, health and wellness brand, today announces its interim results for the half year ended 31 January 2026 ("H1 FY26").

This is a very unusual thing: a recent and successful IPO. FY26 have been officially raised twice (in Dec 2025, and then again in Feb 2026).

The company makes all the gear loved by gymgoers and fitness fanatics: protein powders and shakes, creatine, etc.

Mark downgraded our stance on this from GREEN to AMBER/GREEN last month, at the H1 trading update, despite that update being “ahead”.

It was a contrarian call and it has proven prescient, with the market cap rapidly falling from £600m to £500m since then.

But these are some excellent results:

Adjusted EBIT converts cleanly to adjusted PBT, and there are zero adjustments.

Net cash finished H1 at £26m.

Operations/strategy - everything you’d expect here with the brand expanding in UK high street retailers etc. There was also an “out-licensing” agreement with Morrisons.

Current trading and outlook

Full year guidance is unchanged despite expectations of disruption in the Middle East.

As announced as part of the Group's trading update on 17 February, the Board anticipates full‑year revenue of approximately £140 million

As previously disclosed, due to a better than expected peak trading period and accelerated demand for a number of H1 FY26 product launches, this is expected to result in a more H1‑weighted revenue profile than in prior years

I usually give out about expected H2 weightings, as the common precursors to profit warnings.

So in this case I’m not going to give out about an expected H1 weighting; maybe H2 will surprise positively?

CEO comment:

"Our vision to become the world's most trusted and innovative sports nutrition, health, and wellness brand remains at the heart of our ambition. This six-month period has further highlighted both the breadth of opportunity before us and our proven ability to realise it. The performance and momentum across the business reflects a consumer environment that continues to shift decisively towards health, fitness and wellbeing…

Since our IPO, we have seen an uplift in our profile, awareness, trust and credibility - exactly as we had envisaged, but even more impactful than we could have anticipated. This has enabled us to move faster and think bigger, with an innovation engine that is stronger than ever, allowing us to bring new products to market at pace, deepen customer relationships and adapt quickly to evolving consumer needs as we continue to build the business for the long term."

Estimates

Cavendish have published on this today (thanks to them for that). They’ve reiterated forecasts.

These forecasts include:

FY July 2026 Revenue £140.3m, adj. PBT £38.5m

FY July 2027 Revenue £155.7m, adj. PBT £42.6m

FY July 2028 Revenue £172.9m, adj. PBT £47.8m

Graham’s view

Hopefully the timing of Mark’s and my respective coverage of this stock is going to work out perfectly, with Mark’s more conservative positioning (at a £600m market cap) dovetailing nicely with my optimism (at £500m).

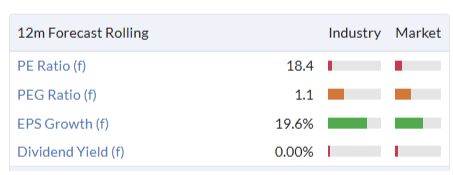

The PEG ratio (Price/Earnings to Growth ratio), for example, is only 1.1x today, according to the StockReport. A reading of 1x typically indicates a stock that is fairly valued:

But it really matters which year you choose, when calculating the PEG.

Earnings per share growth from FY25 to FY26 is expected to come in strong (as high as 25%), but then, as Mark identified, maybe only 11% the following year. That takes the PEG ratio much higher (i.e. suggesting that the stock is overvalued).

But then, the PEG is not the only metric worth looking at. Higher-quality businesses deserve higher PEGs, in my view. And Applied Nutrition strikes me as a high-quality business.

It’s not just about these metrics:

It’s also the strength of the brand: Applied Nutrition is a highly reputable name in an ever-growing industry.

Applied Nutrition is doing what I always hoped Science in Sport (SIS) would do for its investors.

I’m going to take this back to GREEN.

Roland's Section

Spire Healthcare (LON:SPI)

Down 20% at 156p (£626m) - Update on Strategic Review - Roland - AMBER/RED =

Private healthcare group Spire is the biggest faller in the FTSE 350 this morning, following news that takeover talks with private equity groups Bridgepoint and Triton Investments have both failed.

Newswire reports last week had suggested that Bridgepoint might be preparing a $1.3bn+ bid for Spire, while Triton was also said to be considering a bid. Both Triton and Bridgepoint subsequently issued statements on Friday confirming they do not intend to make an offer for Spire.

Bridgepoint noted that it was “grateful for the efforts of the Spire Healthcare Board” but said it had been unable to find a “transaction structure that would work for all stakeholders at this time”.

Update on Strategic Review: main points

Today’s update from Spire suggests the strategic review process remains ongoing, with a number of options still being considered:

The Board of Spire Healthcare remains in discussions with other parties in relation to a potential sale of the Company. There can be no certainty that any offer will be made for the Company nor as to the terms of any offer, if made.

The Board and Management are also continuing to actively evaluate other appropriate actions to drive long-term, sustainable shareholder value.

Roland’s view

In fairness, the current geopolitical environment may be making it harder for Spire to find a buyer for its business. But I can’t help feeling that the problem here might be related to the Board’s expectations on valuation, given the company's poor profitability and uncertain trading outlook.

As I’ve discussed previously, Spire’s board has complained that the value of the business is not being recognised by the market – in essence, that the share price is too low.

Property: one leg of the company’s argument is that the value of its freehold property estate is not being recognised by investors. Perhaps.

But Spire’s FY25 accounts showed debt and lease liabilities of £1,316m accounting for over 75% of the £1,692m reported value of the group’s property, plant and equipment. That may not leave much room for further leverage, although a buyer might be able to refinance at lower cost and perhaps revalue some older freeholds.

Operating business - uncertain outlook: it’s not clear to me that the group’s operating business deserves a high valuation, either. As I’ve commented previously, the evidence from recent years is that Spire’s healthcare business isn’t very profitable:

While the StockReport suggests a low price/free cash flow multiple, my sums suggest 2025 free cash flow to equity was just c.£23m, much lower than the value implied by the normalised figure calculated by Stockopedia’s data supplier. That’s equivalent to a price/free cash flow ratio of around 26x.

NHS changes? A further concern for me is that 30% of the group’s hospital revenue comes from NHS commissioning. This statement from the FY25 results makes it clear that there is a significant uncertainty about the outlook for this source of activity:

At the time of the Company's Trading Update released on 3 December 2025 (the "December Trading Update"), we indicated NHS volumes to be a material uncertainty across the sector as a result of Integrated Care Board budgetary restrictions and a resultant slowdown in commissioning activity with the independent sector. Since then, there has been increased cessation of NHS activity at some of our sites through the imposition of Activity Management Plans to the end of March 2026. As a result, we expect Q1 NHS revenue to decline c.(25)% y/y.

While April marks the start of a new financial year for the NHS, Spire doesn’t yet have any visibility on the level of funded activity it will receive:

Demand for NHS treatments through the Electronic Referral System remains high but committed funded activity is yet to be discussed or agreed with the NHS; and there remains material uncertainty as to when plans may be finalised and the terms they will be agreed on.

As far as I can see, Spire is highly geared, not very profitable and has limited visibility on revenues from its largest external customers. I would speculate that this combination is likely to limit the value placed on the business by potential acquirers.

I don’t see any reason to change my previous AMBER/RED view following today’s news.

ME International (LON:MEGP)

Shares suspended - 2025 Annual Results - Roland - AMBER/GREEN ↑

After two delays due to requests from its auditor for additional time, instant-service equipment specialist ME Group has finally published its 2025 accounts today for the year ended 31 October 2025. That’s nearly five months after the year end, which I think is very poor for a FTSE 250 company.

ME shares were suspended on 2 March due to the company failing to meet the four-month reporting timeframe for FTSE 250 companies. They remain suspended at the time of writing, but management expects to apply for the suspension to be lifted following the publication of the annual report later today.

There could be some volatility when the shares resume trading – although perhaps not so much. Today’s results are in line with expectations and show incremental growth from FY24, with a similar and in line outlook for 2026.

Let’s take a look at today’s numbers, which appear to include details of one possible reason for this year’s audit delays (hat tip to Tortoise Investor for flagging this up in the comments!).

2025 results summary

ME Group warned on profits in November, so it’s good to see that today’s results are in line with expectations:

Revenue up 2.4% to £315.4m

EBITDA up 5.4% to £120.4m

Pre-tax profit up 6.5% to £78.2m

Adjusted earnings per share up 4.5% to 14.91p

Net cash down 10.2% to £26.5m

Dividend up 9.5% to 8.64p per share

Launch of £18m share buyback

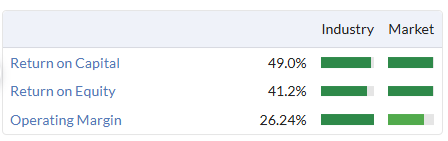

These figures are certainly not bad. CEO and Deputy Chairman Serge Crasnianski reports “another year of record profitability” and the group’s quality metrics remained impressively strong last year:

Operating margin: 24.8% (FY24: 24.2%)

Return on capital employed: 31.5% (FY24: 32.7%)

Divisional trading

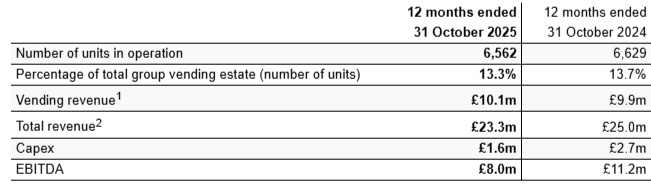

Trading headlines from the group’s key operational divisions are robust, with continued strong growth in unattended laundry services and laundrettes:

WASH.ME revenue up 17.3% to £112.4m, with laundry EBITDA up 18.1% to £55.5m (49% EBITDA margin).

A record 1,326 machines installed, taking the total in operation to 7,607 (+17.7% YoY)

Laundry EBITDA now accounts for 46.1% of group EBITDA

Average revenue per machine fell by 5.8% to £14,329, “partly due to unusually warm weather in the summer months across Europe”.

Plans to install a further c.1,300 machines in FY26.

The mature but core photobooth business also performed reasonably well, albeit revenue fell slightly last year:

PHOTO.ME revenue down 3.7% to £168.6m, with EBITDA down 3.7% to £59.3m

Number of units in operation broadly unchanged at 30,520.

“Robust” trading in France, Belgium and Netherlands.

A regulatory change requiring passport photos to be taken by certified photographers hit revenue in Germany.

Vending revenue in the UK and Ireland fell by 21.8%, mainly due to the end of a contract (previously announced).

Average revenue per photo machine fell by 3.7% to £5,437

The other business that’s broken out individually is Print.ME. This offers “high-quality digital printing services” – presumably mainly for photos:

Revenue down 8.3% to £11.1m.

EBITDA up 26.5% to £6.2m, giving a 56% EBITDA margin.

Upgraded machines drove higher EBITDA margins.

Number of units in operation was broadly unchanged at 4,515.

Average revenue per machine rose by 1.5% to £2,389.

Other vending businesses: these are collectively cateogorised as ancillary and include Feed.ME (freshly-squeezed orange juice), Amuse.ME (children’s rides) and Copy.ME (photocopiers).

As we can see from the summary below, they made a small and diminishing contribution last year, but could potentially provide avenues for future long-term growth:

Balance sheet & cash flow: capital expenditure rose by 20% to £65.6m last year, primarily because of £31.8m of investment in the fast-growing laundry business (FY24: £25.4m). This appears to be delivering results, though, as I highlight below.

As a result of this increase in spending, my sums show FY25 free cash flow of £26.5m (FY24: £32.4m).

This represents a relatively poor 50% conversion from net profit of £54.9m, but there’s a good explanation for this.

ME Group is currently in an expansionary phase where capital expenditure on new equipment (£65.6m) is running ahead of depreciation on existing equipment (£32.4m). Depreciation is deducted from profits whereas capital expenditure is not, so this naturally leads to a situation where free cash conversion from profit is relatively poor.

This situation is likely to reverse at some point in the future. With net cash of £26.5m, I don’t see any problem with the current situation as long as future spending is managed to maintain attractive returns on capital.

ME has a good track record of capital allocation, in my view. My calculations show capital employed has risen from £140m to £248m over the last 10 years.

Over the same period, the group’s operating profit has risen from £40m to £78m.

Comparing the increase in operating profit (£38m) to the increase in capital employed (£108m) suggests the additional capital deployed has generated a return of 35.2%, in line with the group’s overall profitability.

The ability to deploy additional capital at high rates of return is one of the hallmarks of a quality business – it supports long-term organic growth and shareholder returns.

Interestingly, ME’s share price today (pre-suspension) is lower than it was 10 years ago. I wonder if this could be represent a value opportunity, assuming past performance remains sustainable:

Cash reporting error: it’s unfortunate that ME Group appears to have made a surprising accounting error for a company whose business model is based around operating vending machines.

Details of this are tucked away at the very end of today’s RNS – almost as if the company was hoping investors would not find it (my bold):

The opening balance of cash and cash equivalents at 1 November 2024 has been restated by a reduction of £8,689,000 to correct an error in the prior year financial statements. The adjustment is to correct an error in the calculation of the value of cash in transit held in the Group's vending machines at the reporting date.

I am not sure if this refers to the entire cash held in the company’s vending machines or just a part of it.

The net effect is that FY24 year-end net cash has been restated to £29.5m today, from £38.2m in the FY24 results.

If I’ve understood today’s commentary correctly, this error may have been introduced during the FY23 financial year, as the opening figures for FY24 have also been restated.

The reduction in reported cash is offset by a corresponding reduction to payables, so there is no overall impact on net assets or earnings. Even so, I think this is a disappointing error.

FY26 Outlook

The company reiterates the guidance provided previously today:

In respect of the year ending 31 October 2026, the Company confirms that the year-to-date performance is in line with expectations.

Consensus forecasts on Stockopedia prior to today suggested earnings per share could rise by around 4% to 15.6p per share this year, putting ME Group on a (pre-suspension) P/E of 8.8x.

The forecast dividend of 8.55p implies a potential yield of 6.3%, assuming no major share price movements when trading resumes.

Roland’s view

I am disappointed to see that a vending machine specialist failed to account correctly for the cash in its vending machines.

Leaving aside this surprising error, I don’t see much to worry about in today’s figures. This business remains highly profitable and cash-generative and appears to be generating decent returns from its capital expenditure.

While regulatory risks relating to ID photographs will always be a concern for the photo business, ME Group has worked around these issues successfully for many years. Perhaps they’ll continue to be manageable.

Meanwhile, the growth of the laundry business remains encouraging, with a similar level of new machine deployments expected in FY26.

Arguably, I could justify leaving my previous neutral view unchanged on the basis of:

November’s profit warning;

The accounting error reported today;

The delay to these results and share suspension.

However, ME Group has a long track record of mostly good performance and today’s results appear to show a business that is good and cheap. Based on the last-known share price prior to the suspension, I would normally take a positive view of this business.

On balance, I’m going to follow this framework today and move our view up by one notch to AMBER/GREEN, with the caveat that the valuation might change dramatically when the stock returns from suspension.

Goodwin (LON:GDWN)

Down 35% at 15,000p (£1.13bn) - Trading Update - Roland - BLACK? (AMBER/RED ↓)

Commiserations to shareholders at industrial group Goodwin this morning.

This company – which famously prefers not to provide any forward financial guidance – has issued a trading update flagging up several disappointing pieces of news.

Here’s a summary of the key points:

The good news is that FY26 trading is said to remain in line with expectations, as outlined in the October 2025 trading update:

The Board is pleased to report that it expects, with a high degree of confidence, the trading profit before tax for the financial year ending 30th April 2026 will be in excess of £71 million, representing a 100% increase compared with the prior year (April 2025 £35.5 million).

Unfortunately, the outlook for FY27 appears to be far more uncertain and potentially somewhat weaker.

Order book decline: Goodwin’s “firm fixed orderbook” stood at £288m at the end of February, down from £365m on 27 October.

Management says this reflects typical procurement cycles for the markets it serves, but I note that one year ago in March 2025, the company reported “a new record” order book of £300m – an increase from the prior H1 figure.

Tender losses: the Mechanical Engineering division has “been disappointed by the outcome of two significant tenders” in recent months:

The Easat business lost a tender for 20 7.5m coastal radar antenna and transceivers with a value of c.€18m.

Goodwin International “unexpectedly lost a tender with Sellafield” with a bid value of more than £45m.

I am not an expert on the different elements of this business, but the Sellafield tender loss looks like a particularly nasty surprise to me. The nuclear power station is an existing customer and my non-expert impression was that Goodwin was very strongly positioned in this market..

Delayed deliveries: the company says that as of the time of writing, none of the “many valves” on order for LNG facilities in the Middle East or USA have been cancelled or placed on manufacturing hold.

However, “on certain large Middle East contracts, the group has been requested to delay the dispatch of values”. Goodwin says that while “these requests have not resulted in cancellations, they may affect the timing of revenues”.

With the year end approaching on 30 April, I guess there’s a chance that some remaining orders scheduled for this year could end up slipping back into FY27, even if no cancellations eventually result.

Duvelco: this subsidiary produces “specialist polyimide polymers” for applications such as aerospace and automotive. Unfortunately, “no commercial sales have been made to date”.

Market engagement is now expected to see Duvelco make “initial contributions” to revenue in FY27, although any contribution is not expected to be substantial in the early years. This is due to the approval and adoption hurdles faced by products of this type.

Refractory Engineering: trading conditions are broadly unchanged, but management note that high gold and silver prices are weighing on confidence in the jewellery casting markets, while consumer spending also continues to show a “lack of confidence”.

Dividend guidance: in its results last year, Goodwin announced an alteration of its dividend policy to increase the payout ratio:

[…] the Board is confident that the alteration of the dividend policy from 38% to 58% of post-tax profits plus depreciation and amortisation is a safe and viable change for now and the foreseeable future.

Unfortunately it looks like a rapid u-turn could be on the cards. Today’s statement notes:

[…] the Board is considering whether to revert to its previous dividend policy, under which distributions were limited to 38% of post‑tax profit plus depreciation and amortisation, or to a lower level should this be considered appropriate given the escalating Gulf situation and the broader economic environment.

Outlook: what can we deduce?

Goodwin doesn’t provide forward profit guidance. One notable exception to this was in October 2025, when the Board guided for pre-tax profit to double to £71m this year.

My rough estimate suggests this might equate to earnings of c.7.25p per share. This would mean that prior to this morning’s fall, the shares were trading on a forward earnings multiple of >30x.

If my earnings guess is right, Goodwin might be trading on a more reasonable FY26E P/E of c.19 after this morning’s drop.

I think there’s a risk pre-tax profit may now fall slightly below the company’s previous guidance of >£71m, but for me, the bigger concern is the outlook for FY27:

The February order book of £288m reported today is in line with the £287m figure reported on 30 July 2025.

This suggests to me that the group’s profits won’t necessarily collapse next year, but could be lower as a result of background cost growth and capex for which demand may not be lower than expected.

The company’s decision to reverse its dividend policy after less than a year also worries me. It seems to suggest that management may be expecting a material reduction in profits in FY27, if not before.

Roland’s view

To put this morning’s share price drop in context, I think it’s worth remembering that Goodwin’s share price is still up by >100% over the last 12 months, despite this morning’s fall:

The stock is not necessarily cheap. It’s possible that the shares could fall further to unwind the exceptional gains of the last year before resuming a more positive trend. When a High Flyer loses momentum, the resulting decline can be long and painful for shareholders.

Graham was AMBER/GREEN on Goodwin in December, noting the high valuation, strong outlook and impressive track record. That picture has now changed, at least temporarily.

My decision today is whether to be neutral or to adopt a more cautious (negative) view.

What investors need to decide is whether this is a short-term blip or the start of a longer period of weaker trading.

I don’t have the information needed to form a judgment on this, but given the brutal market reaction to today’s news, I am inclined to be cautious. I would certainly be reluctant to buy the shares before learning more about the trading outlook.

For these reasons I am going to drop down to AMBER/RED ahead of further updates.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.