Good morning! I have some backlog items from yesterday to look at - I will do my best to catch up.

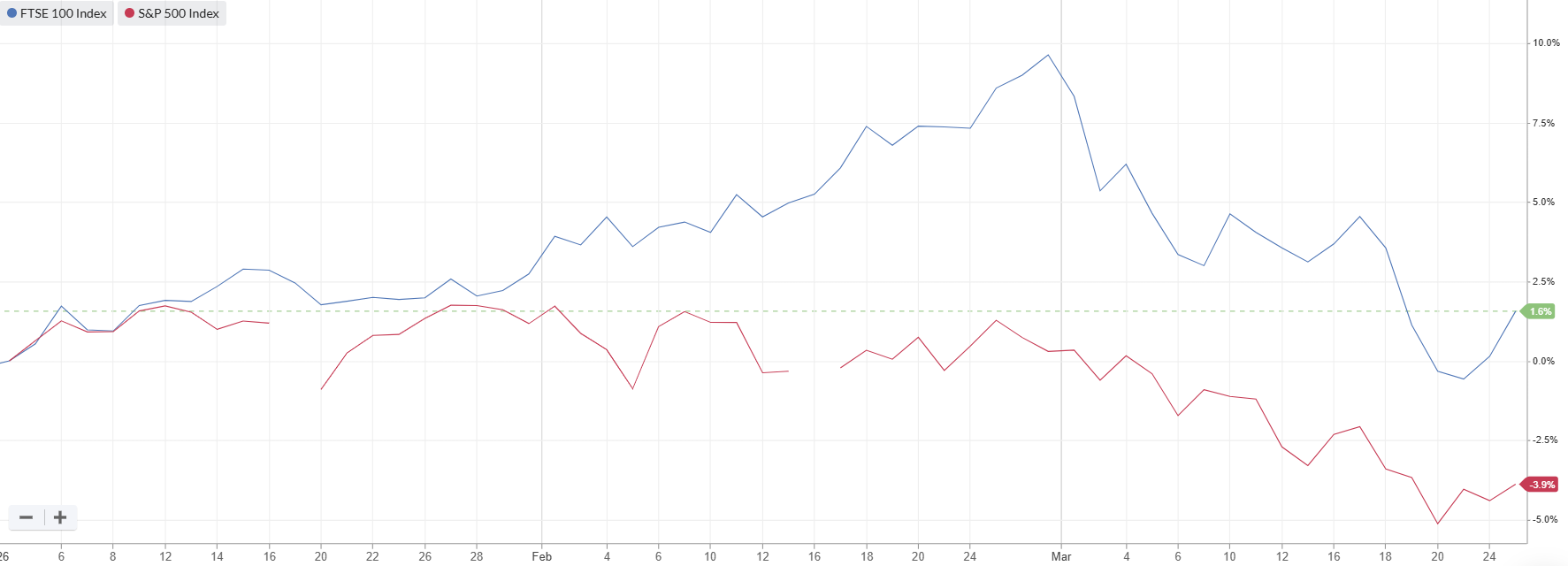

The topsy turvy action in the market continued on Wednesday, with a strong recovery day: the FTSE rose 1.4%, returning back above the 10,000 level.

As always, I will point out the experience of someone who doesn't read the news and who only cares about the year-to-date performance of the index. As far as that person is concerned, the FTSE is up 1.6% year-to-date and everything is fine.

The S&P 500 is a different story, admittedly, down nearly 4% year-to-date. The S&P had outperformed the FTSE long-term, but the last year or two have finally seen a reversal of this trend, with (in my view) the excessive valuation of US mega-caps finally catching up with them a little.

FTSE in Blue, S&P in Red,

The current situation with Iran can perhaps best be described as fluid. The US says that peace talks are ongoing, while Iran says that the US is "negotiating with itself".

Potential next steps could include the Strait of Hormuz reopening on the condition that ships pay Iran a toll. Some Indian and Chinese ships have passed through the Strait this month, with “transit fees” paid to Iran making this possible. From the point of view of the global economy, this might be one of the least worst options.

Another possibility is that the US takes control of the Strait. According to Bloomberg, 5,000 US troops - plus aircraft and amphibious landing vehicles - have been deployed to the region. This is obviously not enough for a major land-based operation, but it has been speculated that US naval escorts might be used to help ships to pass through the Strait.

Brent crude oil futures are currently trading at $99 (June delivery), up from $73 on the eve of the war.

US Natural Gas futures are at 131p, up from 78p on the eve of the war. They traded as high at 176p last week, before President Trump started talking about the prospects for peace.

Spreadsheet accompanying this report: link.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

3i (LON:III) (£28.6bn | SR57) | In FY25 Action generated net sales of €16,000m (up 16%) and operating EBITDA of €2,367m (up 14%). Period to the end of Week 12: LfL sales growth 4.0%. Performance ex-France is above expectations, with France slightly below. Guidance for 2026: LfL sales growth 4-5%. EBITDA margin maintained at 14.8%. | ||

Next (LON:NXT) (£14.6bn | SR69) | Sales +10.8%, PBT +14.5% to £1,158m. This is £8m ahead of guidance. EPS +17%. FY27 outlook: full price sales growth guidance is maintained at +4.5%. PBT guidance increased to £1,210m, up 4.5%. | GREEN ↑ (Graham - I hold)

After raising guidance, Next are now buying back their shares below a new limit of £131, As I trust their capital allocation policy, I’m going to turn GREEN on this again, at least until the share price gets back over £131 (currently £127). This is a slightly aggressive stance from me, considering the above-average P/E multiple already attached to this retailer. However, I do view this as an exceptional business. If I’m ever going to be aggressively bullish on something, I’d like it to be a company like Next. | |

Intertek (LON:ITRK) (£5.73bn | SR40) | CFO becomes Executive VP Asia Pacific, based in Vietnam. He ceases to be an Executive Director. Regional CFO of EMEA is promoted to CFO. | ||

International Public Partnerships (LON:INPP) (£2.27bn | SR84) | NAV per share up 4.7% to 151.5p. Combined with dividends paid, NAV total return was 10.6%. | ||

Currys (LON:CURY) (£1.46bn | SR93) | After eight years, the CEO is leaving to take a new job. He will remain to ensure a smooth and orderly transition. The company has traded in line with expectations since the last update on 21st January. | GREEN = (Mark) The share price drop today doesn’t make a lot of sense to me. While I have some concerns over the falling share price Momentum, the fundamental Momentum still seems to be with the business, and it remains cheaply-rated. With trading confirmed as in line with recently upgraded expectations, I don’t think the planned exit of even a well-regarded CEO should change our positive stance here. | |

Playtech (LON:PTEC) (£1.11bn | SR57) | Revenue down 10%, adjusted PBT down 28% to £44.2m. Actual pre-tax loss £169.5m. “Excellent start to 2026… Group expects to deliver FY26 ahead of current consensus expectations, despite tax headwinds across several markets.” | ||

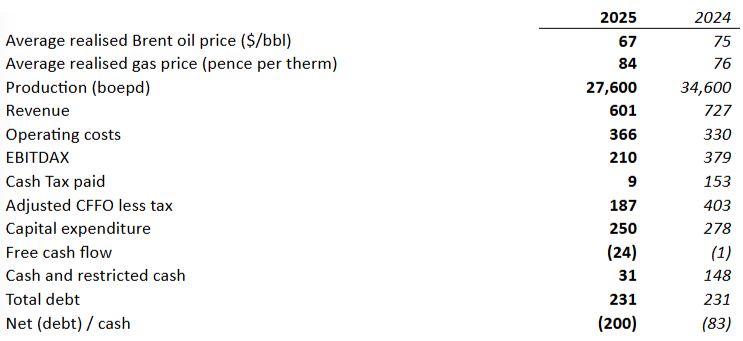

Serica Energy (LON:SQZ) (£991m | SR84) | Production 27,600 boepd (2024: 34,600), impacted by unscheduled downtime at the Triton FPSO. EBITDAX $210m (2024: $379m). Production year to date in 2026 of 38,600 boepd, following a production interruption for further maintenance work at the Triton FPSO. Unchanged guidance for 2026 production of significantly over 40,000 boepd. | AMBER/GREEN = (Mark) | |

Firstgroup (LON:FGP) (£972m | SR65) | First Bus and First Rail trading in line with expectations. The Group continues to anticipate modest growth in adjusted earnings per share in FY 2026. | ||

Oxford BioMedica (LON:OXB) (£733m | SR29) | FY 2025 revenues at upper end of guidance. ”OXB enters 2026 well positioned to deliver on our near and medium-term guidance…” FY 2026 guidance: revenues of £220 - 240 million with Operating EBITDA margin c.10%. | ||

Ceres Power Holdings (LON:CWR) (£602m | SR25) | Final results & Ceres and Centrica sign a strategic partnership | 2025 revenue down 37% (“primarily reflects the timing of revenues recognised in 2024”). Adjusted EBITDA loss widens to £32.5m (2024: £22.3m). Although we are conscious of the uncertainties arising from the war in Iran and its impact on global energy markets, we start 2026 with strong operational momentum. We have generated our first royalty revenues and are seeing growing demand across commercial and industrial power markets - particularly in the rapidly expanding data centre sector. | |

Cohort (LON:CHRT) (£582m | SR27) | Contract with a value of €42.3M to deliver Integrated Communication Systems (ICS) and Networks to the Portuguese Navy. Delivery will take place over the period to 2029. “...further underpins our order book and enhances the visibility of future revenues.” | ||

THG (LON:THG) (£534m | SR50) | Revenue +2.3%. Adjusted EBITDA £76.6m, ahead of guidance (£74m). Operating profit £8.1m. FY 2026 expectations remain unchanged and in line with the company consensus range. Net debt is anticipated to reduce to between c.£110m - £130m before disposals. | ||

Guardian Metal Resources (LON:GMET) (£481m | SR30) | FD becomes NED. New CFO appointed, a US national based in Utah. Was VP Business Development at Ceibo, a Chilean copper sulfide leaching company, and spent 12 years at Rio Tinto. | ||

Pollen Street (LON:POLN) (£441m | SR81) | Fee Paying AUM up 32% to £5.2 billion. Profit after tax +14% to £56.6m. “We enter 2026 with exciting momentum and a robust pipeline for both deployment and fundraising… Despite our strong performance and favourable fundamentals, the share price has not fully reflected the progress made…” | GREEN = (Mark) The share price drop today doesn’t make a lot of sense to me. While I have some concerns over the falling share price Momentum, the fundamental Momentum still seems to be with the business, and it remains cheaply-rated. With trading confirmed as in line with recently upgraded expectations, I don’t think the planned exit of even a well-regarded CEO should change our positive stance here. | |

Filtronic (LON:FTC) (£405m | SR62) | $8.0m (£6.0m) contract with US company to develop, manufacture and qualify a range of high-performance system level products. | ||

Ecora Royalties (LON:ECOR) (£324m | SR51) | $57.0m portfolio contribution for 2025 (2024: $63.2m) with significant increase in contribution from base metals royalties largely offsetting reduction in Kestrel steelmaking coal contribution. Profit after tax of $22.2m. Ecora's key commodity exposures performed strongly in early 2026. | ||

Mears (LON:MER) (£290m | SR90) | Revenue +0%, adjusted operating profit +2% (£64.8m). “The Board anticipates that the profit reduction from the disposal of the Facilities Management activities will be fully offset in the current year by an outperformance in the Core business… adjusted operating margins will be maintained within the range of 5-6%.” | ||

Capita (LON:CPI) (£289m | SR20) | Agreed to sell its private sector contact centre business to Inspirit Capital for £1, contingent consideration payable to Capita up to a cap of £61.5m. Expected transaction, transitional restructuring and separation costs in 2026 of approximately £20m.Expects 200bps improvement in adjusted operating margin by 2027. | ||

Social Housing REIT (LON:SOHO) (£275m | SR63) | Net rental income +12% to £40.0m, Adj. EPS +21% to 6.53p. Portfolio valued at £606.3m (2024 £626.4m) reflecting a Net Initial Yield of 6.42% (2024: 6.22%). | ||

Capricorn Energy (LON:CNE) (£187m | SR81) | WI Egypt production of 20,024 boepd at the upper end of guidance of 17,000-21,000 boepd, comprising 40% liquids; net entitlement sales volumes 9,701 boepd. Revenue $134m @$68.4/bbl & $3.1/mscf, Net cash inflows of $81m from Egypt operations post-capex, Profit of $19m; profit from continuing operations of $16m.Group net cash of $103m. | ||

Arbuthnot Banking (LON:ARBB) (£142m | SR58) | Operating Income - 6% to £169.5m, PBT -31% to £24.2m, EPS - 28% to 109.1p, NAV PS +3.5% 1694p. CET1 13.3% (FY24: 13.2%). | ||

Strategic Minerals (LON:SML) (£138m | SR38) | Redmoor - 2026 MRE & Updated Economic Sensitivity Analysis | JORC Inferred Mineral Resource Estimate +49% to 17.4 Mt @ 0.65% WO3. After tax NPV(8%) of US$1.54B and 40% IRR. | |

Tribal (LON:TRB) (£127m | SR87) | Revenue +4% to £92.5m, ARR +11% to £63.3m, Adj. EBITDA +8% to £17.5m, Net cash £11.4m (FY24: £3.2m net debt). “...continued sales momentum in FY26 and the delivery of a financial performance in line with the Board's current expectations.” | ||

Hostelworld (LON:HSW) (£124m | SR20) | Net revenue +2% to €93.8m, Full-year adjusted EBITDA -9% to €19.9m, in line with consensus. EPS -15% to 11.9c, Net Debt €1.6m (2024: net cash €2.0m). Q1 trading +12% revenue y-o-y. ME impact: “...seeing some softness in bookings to Asia and Oceania, offset by stronger demand in Europe and North America, supported in part by the timing of Easter this year. To date there has been no material effect on revenues. Our current outlook assumes no material impact on bookings and is subject to there being no further escalation in the region which would further disrupt air travel.” | GREEN = (Graham) | |

Treatt (LON:TET) (£116m | SR53) | “Trading in the year-to-date has progressed as anticipated, with a quiet first quarter, consistent with prior years, followed by increasing momentum in the second quarter.…expects to deliver a full year performance in line with management expectations with a greater weighting to the second half for FY26 than in FY25.” | AMBER = (Mark) | |

Gemfields (LON:GEM) (£84.5m | SR38) | Revenue -32% to $135.1m. LPS 1.3c (FY24: 1.8c loss), net debt $39.3m (FY24: $80.4m net debt), after sale of Faberge Limited for $50m. “The situation in the Middle East has already increased costs, particularly fuel, and any further escalation could materially impact cost and market conditions. It remains too early to determine the extent of the impact on the year ahead.” | ||

Solid State (LON:SOLI) (£80.8m | SR48) | Interim CEO, John Macmichael, appointed to the post of Chief Executive Officer on a permanent basis with immediate effect. | ||

Orosur Mining (LON:OMI) (£74m | SR14) | Published technical report in support of the Company's 100%-owned Anza Project in Colombia including its maiden Mineral Resource Estimate for the Pepas deposit. | ||

Helix Exploration (LON:HEX) (£70.4m | SR16) | LBT £1.86m (FY24: £2.17m LBT), cash £2.73m (FY2: £4.96m) after £9.5m equity raise in period. Further £2.2m raise post-period. | ||

Helium One Global (LON:HE1) (£68.1m | SR24) | H1 LBT £1.67m (24H1: £1.93m LBT), Net Cash £5.12m (30 Jun: £3.15m), after £11.93m equity raise in period. Proposal to raise an additional £3.5m +£1.0m retail offer at 0.6p, a 17.6% discount to last night’s close. | ||

Andrada Mining (LON:ATM) (£65.1m | SR33) | FY ore processed +8% to 1.04mt, tin concentrate produced +15% to 1,740t. | ||

Town Centre Securities (LON:TOWN) (£48.9m | SR44) | EPRA NTAV -3% to 253p. EPRA EPS -33% to 2.8p. LTV 54.8% (FY25: 53.1%), Interim Dividend 2.5p. | ||

Marks Electrical (LON:MRK) (£48.8m | SR48) | 26H2 revenue +4.7% means FY26 revenue £108.5m (FY25: £117.2m). FY26 adjusted EBITDA is now expected to be comfortably ahead of consensus and in excess of £2m. Cash is expected to close in and around £3.5m-£4.0m reflecting strong working capital management particularly within inventory. Tom Pallatt will be joining the Board as permanent Chief Financial Officer on 1 April 2026. | ||

Metals One (LON:MET1) (£18.2m | SR5) | Creditor meeting to approve plan by Lions Bay Resources to acquire the South African assets of the Vantage Goldfields Group. | ||

Aptamer (LON:APTA) (£16.9m | SR21) | 83.3m shares offered at 0.6p/share to raise £0.5m before costs. Also receive 1 for 3 warrants at 0.9p. | ||

Ground Rents Income Fund (LON:GRIO) (£16.3m | SR9) | Exchanged contracts to sell its freehold interest in the property formerly known as The Portland Hotel in Hull, for £1.45 million + £125k in legal costs and £250k to gaining vacant possession from the previous tenant. Proceeds to repay debt. | ||

Checkit (LON:CKT) (£15.4m | SR28) | [After] a review of the various strategic options available to the Group and has determined that it would be appropriate to investigate a sale of the Company. Six unsolicited expressions of interest in an asset sale over the last 9 months, but no active discussions. | ||

Altona Rare Earths (LON:REE) (£11.9m | SR16) | H1 LBT £376k (24H1: £512k LBT), Cash £348k (24H1: £109k) after £1.7m fund raise in period. Cash post-period end £1.0m from share issue and warrant exercise. |

Graham's Section

Next (LON:NXT)

Up 5% at £126.75 (£15.3bn) - Results for the Year Ending January 2026 - Graham - GREEN ↑

(At the time of writing, Graham has a long position in NXT.)

This is a top holding and a multi-bagger for me, currently worth 9% of my single-stock portfolio.

Results are ahead of expectations, and guidance is raised - which is normal for Next, thanks to their conservative planning assumptions.

The headlines for FY January 2026:

Sales +10.8%

PBT +14.5% to £1158m

Earnings per share +17% to 744.2p

At the January trading update, PBT guidance was raised by £15m to £1,150m.

As you can see above, the actual result is another £8m better than that, due to “better than expected full price sales in January, along with improved clearance rates in our end-of-season Sale.”

Guidance for FY January 2027 (emphasis added by me):

Guidance for full price sales growth in the year ahead maintained at +4.5%.

NEXT Group pre-tax profit guidance increased to £1,210m, up +4.5%. This is £8m higher than the guidance given in January due to the increase in the base profit mentioned above.

We anticipate returning £500m of cash to shareholders through share buybacks, special dividends or capital return.

£500m of cash for shareholders will be an increase on the £421m returned in FY27.

As usual, forward guidance is very clear. With the conflict in the Middle East, Next is assuming £15m of additional costs (fuel, freight, etc.), on the basis of a duration of three months. They say “the costs are offset by savings, and so do not affect guidance” - they must have found some discretionary spending to cut elsewhere.

If the conflict lasts longer than three months, only then will they pass price rises onto customers and potentially suppress sales.

If you have the time, I recommend reading Next’s “The Big Picture”. It’s a lesson in business as much as it is an overview of the company itself.

For example, in a section called “Simple, but not easy”:

Improve our product offer, grow overseas, develop our platforms, control costs, make margin, and follow the money. It sounds simple, and it is, but it’s not easy. A good plan is only 10% of the battle, the rest is execution. And great execution cannot be willed from on high, it requires people capable of thinking and acting for themselves at every level, and that is what NEXT aims to be: an organisation that can move fast, take decisions, and get things done.

We do not always achieve that ambition, but our aim is clear: at NEXT, whatever your role or level, you should be making decisions; if you are not, the chances are you are not doing it right.

Of course, words are cheap - but Next has proven its worth over many years of terrific execution. So I think its words are worth listening to.

I also appreciate this pushback on the need for an AI function:

We are not developing a central AI function. The benefits AI can bring to software development, range development, customer service and warehouse operations are so varied, and their challenges so different, that generic advice from a central function would be little more use than a central Spreadsheet Department.

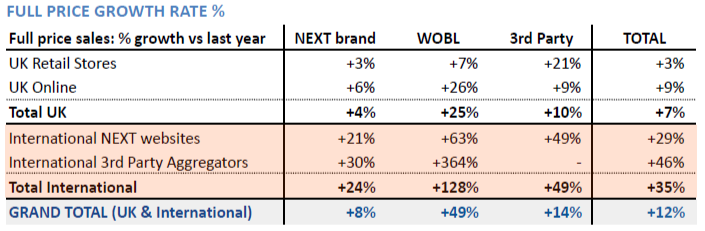

International growth: an important theme here recently has been fast international growth, so I want to check in on how that’s doing.

Fast international growth is visible in the table below:

In pound terms, the company is quick to point out that UK growth was not far behind: £254m of UK sales growth, vs. £297m of international growth. That’s due to the still much bigger size of UK operations: 78% of Next’s full price sales is from the UK, vs. 22% internationally.

Graham’s view

I continue to view Next as best-in-class, organisationally, both from the point of view of the retail sector and indeed among listed companies more generally.

This is one of the few instances where I think investors can get something out of reading an annual report even if they have zero interest in the company’s shares. They demonstrate what investor communications should look like, in my view.

As for my current stance on the shares? I take my cue from the company itself, and its rational approach to share buybacks: it will do them when they earn at least 8% pre-tax on the investment.

Recent share price weakness has enabled them to start buying back again:

The latest update:

In our previous guidance, issued in January, we had assumed no share buybacks, because the share price had consistently remained above our buyback price limit in recent months. Since February, we have been able to spend £196m on share buybacks at an average share price of £126.52. Based on our latest profit guidance, our price limit for share buybacks has increased from £128 to £131.

As I trust their capital allocation policy, I’m going to turn GREEN on Next again, at least until the share price gets back over £131 (currently £127).

This is a slightly aggressive stance from me, considering the above-average P/E multiple already attached to this retailer:

However, I do view this as an exceptional business. If I’m ever going to be aggressively bullish on something, I’d like it to be a company like Next.

Hostelworld (LON:HSW)

Up 2% to 102p (£126m) - Preliminary Results for the year ended 31 Dec 2025 - Graham - GREEN =

(At the time of writing, Graham has a long position in HSW.)

There’s a pleasing headline from this online platform with a niche in budget accommodation.

H2 2025 revenue acceleration continuing into 2026; FY 2025 adjusted EBITDA in line with consensus

The “acceleration” consists of 7% revenue growth in H2, resulting in 2% full-year growth.

However, it must be noted that the overall performance in 2026 wasn’t great:

Adjusted EBITDA down 9% year-on-year to €19.9m

Adjusted profit after tax down 14% to €15m

Net debt finished the year €1.6m, vs. net cash of €2m a year earlier. During the year they spent $12m on an acquisition, which I fear may have been overpriced.

However, this is still a much healthier financial position than they enjoyed previously, and they are paying dividends again. The total dividend for the year is 2.4 cents per share.

They are also nearly finished with a £5m buyback - that’s a meaningful reduction in the share count at this market cap, and all repurchased shares are being cancelled.

Progress?

Hostelworld has been working hard building its own “social network” - a way for hostel travellers, who are often travelling alone, to connect with each other.

The improved H2 performance - when marketing costs fell as a % of revenue - is seen as a reflection of “the growing benefit of our social network”.

This network continues to grow:

Social community reached 3.4m members with member messaging growing 81% YoY, social members book approximately twice as frequently as non-members.

I’m a shareholder here partly because of the large upside potential I see if the hopes for this social community materialise. It seems to me that this would be a pretty valuable asset (compared to a sub-£150m market cap currently).

But even without this somewhat speculative opportunity, if we look purely at the numbers, there is potential value:

Besides the social network, there have been some other pretty important developments:

“Elevate” - generating additional commissions by giving hostels greater visibility on the site.

Budget accommodation - they have expanded beyond hostels, “via a third party inventory supplier”. I don’t think this will dilute the Hostelworld brand too much, if they are sticking to properties that are clear alternatives to hostels.

Outlook sounds fine:

The Group enters 2026 with an expanded platform, a resilient balance sheet, and encouraging early momentum. Q1 trading has been positive, with the Group on track to deliver ~3% bookings growth and >12% revenue growth for the quarter, versus Q1 2025, supported by a commission rate of 17.7% and direct marketing costs of less than 50% of revenue, all consistent with our CMD guidance ranges.

As for the difficulties in the Middle East, they are unaffected so far:

While it is too early to draw firm conclusions from these early trends, to date there has been no material effect on revenues. Our current outlook assumes no material impact on bookings and is subject to there being no further escalation in the region which would further disrupt air travel.

Graham’s view

This is a very small position for me (1%), but it’s one I’m quite excited about - and where I’m open to the possibility of buying more.

The acquisition of “OccasionGenius” last year rocked my confidence, as I couldn’t understand how it could be worth spending $12m on such a small startup business with only a few employees. 2026 is the year when Hostelworld can prove the wisdom of the deal, by integrating useful event data for travellers into the site. They say that this is going to happen in Q2.

This is a stock where my view diverges widely from the StockReport. Indeed, Stockopedia classifies it as a “Sucker Stock”. While I only very reluctantly disagree with the algorithms, in this particular case I do think the risk:reward looks very attractive. Hostelworld does compete against much larger companies, but it's succeeding within its niche. I’m staying GREEN.

Earnings forecasts have been stable since last summer:

And the profit margins and return metrics are already quite decent even with the company at this (hopefully very early) stage of its development

Mark's Section

Serica Energy (LON:SQZ)

Up 5% at 266p - 2025 full-year results - Mark - AMBER/GREEN

If you just looked at the headlines here, you’d say this was a terrible year:

Production problems, lower oil prices and increasing costs lead to cash outflow and ballooning debt. If you’d told investors that this would be the outcome for 2025, they would have expected the share price to halve, not deliver a phenomenal return:

The reality is that markets are forward-looking. During the year, the company has delivered a number of strategic deals. As the CEO says today:

Successful acquisitions mean that Serica will have an increasingly resilient and diversified portfolio, with production set to reach over 65,000 boepd by the end of 2026 as they all complete.

Some caution is perhaps required. The reality is that if they are buying assets, they will have outbid other buyers in a competitive process. While the pool of North Sea acquirers may be limited, no one is looking to sell assets below their perceived economic value. For example, when Serica announced a possible deal to acquire BP's 32% non-operated stake in the Culzean gas condensate field, NEO NEXT exercised its pre-emption rights, meaning the acquisition of the Culzean stake did not proceed. Several similar deals have gone through, and today they separately announced that…

….the acquisition of a 40% operated interest in the Greater Laggan Area ('GLA') and associated infrastructure, and operated licence interests in four near field exploration blocks, from TotalEnergies, has now completed.

They effectively received $56m to do this deal, which sounds amazing, but Total aren't doing this from the kindness of their hearts; Serica will be taking on the eventual decommissioning costs of these fields. So they get the prodigious cash flow now but bear the costs later.

These may well still be an excellent deal, not least because the war in Iran has pushed up short-term energy prices significantly. Serica received 84p/therm average in 2025, up from 76p in 2024. The spot price today is close to 140p/therm. However, it would be naive to take the current 50kboepd Triton production for 2026 and the 65kboepd potential for 2027 and price this all at 140p/therm.

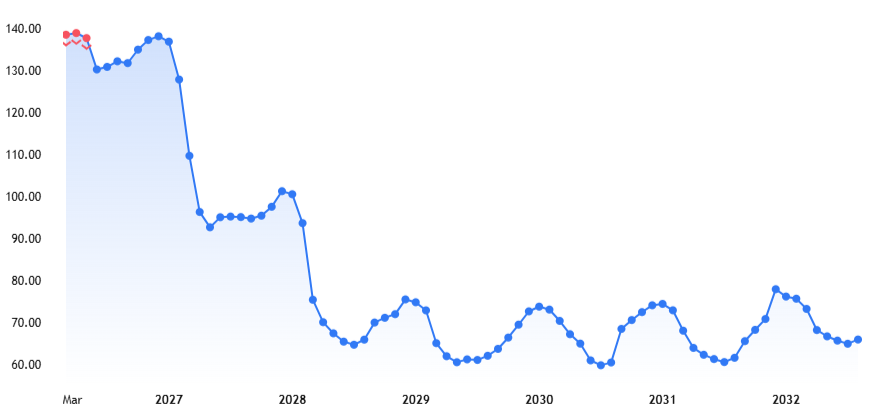

For a more accurate estimate of the impact of energy prices, we need to take the forward curves. Here is the UK NBP Natural Gas Futures from Trading View:

So there is good news and bad news. The good news is that prices are expected to be above 130p/therm for the whole of 2026. The bad news is that they are expected to be at or below 2024 levels from 2028 onwards.

Brent oil is similar. While the spot price is approaching $110/bbl, this is back down to $75/bbl for contracts at the start of 2028. We can’t use a P/E ratio to value a business such as this, we need a discounted cash flow model.

Forecasts:

Investors could build their own models based on these forward energy curves and production assumptions. However, it is much easier to let the brokers handle it for us. Auctus Advisors calculates the following forward FCF numbers:

| Year | FCF $m |

|---|---|

2026 | 469 |

2027 | 370 |

2028 | 274 |

2029 | 184 |

2030 | 84 |

These seem amazing, at least in the short-term. However, in later years, the decommissioning costs start to kick in, and when I calculate an NPV10 based on these figures, I get around £800m, versus a £1.2bn Enterprise Value.

This doesn’t mean that the company is overvalued. Auctus calculates a £3.35/share price, representing a 26% upside from the current price. However, this will be based on production into the 2030’s, not just a high near-term free cash flow figure.

Mark’s view

We have been consistently positive on this company in the past, as we liked their deal-making and high yield. This has paid off, with the shares rising strongly over the last year. However, these results show that we have been largely lucky with this call.

Their deal-making has indeed been strong, but they are buying short-life fields with ageing infrastructure. If these are non-core for existing owners, they may well have been under-invested over a number of years. As both Bruce and Triton have shown, once issues are found they are often more extensive (and expensive) than first thought.

The real increase in value has come from much higher short-term energy prices. Something a purchaser of short-life fields will particularly benefit from. A fairly conservative set of estimates from one of their brokers suggests that the company is still undervalued. However, we should be wary about pricing the stock based on expected FY26/27 numbers, which will be elevated.

At the end of the day, this company is probably still undervalued based on the current forward energy curves, and gives a useful hedge against other holdings which are negatively impacted by high energy prices. However, there are likely to be other oil & gas companies that are more undervalued, and have higher upside exposure to energy prices if that’s what investors want.

They say it is better to be lucky than good, so in the spirit of that, I keep our AMBER/GREEN view.

Treatt (LON:TET)

Up 3% at 202p - AGM Trading Update - Mark - AMBER =

Here’s the key parts of their divisional breakdown:

Heritage (citrus, herbs, spices, florals, and synthetic aromas):

…citrus market headwinds experienced in FY25 have begun to show initial signs of easing, providing confidence that volumes will see some positive momentum into H2, although we continue to expect that a full recovery will take some time to come through.

Premium (Tea & Coffee Extracts, wellness, sugar reduction, fruit & vegatable extracts):

…challenging market conditions impacting end consumer demand continue, particularly in the US.

They mention a “healthy pipeline”, but it seems that this is some way off being seen in orders and sales.

Overall:

Trading in the year-to-date has progressed as anticipated, with a quiet first quarter, consistent with prior years, followed by increasing momentum in the second quarter.…Supported by a combination of ongoing market recovery within citrus, continued customer engagement and a robust order pipeline, the Board expects to deliver a full year performance in line with management expectations with a greater weighting to the second half for FY26 than in FY25.

Ultimately, this is an in line update. However, the market never likes an H2-weighting as it often is a forerunner to a full-year warning. So it is perhaps surprising that this update hasn’t been viewed in a worse light by the market.

Margins:

The company doesn’t disclose exact percentage margins for each specific sub-segment, but consistently categorises the Premium unit as a "higher margin" business compared to the Heritage unit. For example, a decline in NA Premium sales in early 2025 was the main driver for the group's overall gross margin falling from 27.8% to 24.9%. Continued weakness in this segment could have an outsized impact on the bottom line.

I also think recent increases in energy and fertilizer costs may have a delayed impact on raw ingredient prices, which may put paid to the anticipated improvement in H2. Citrus prices, especially orange oil, can have a significant impact on Treatt, as they increase input costs while also incentivising beverage customers to reformulate products with cheaper alternatives, directly reducing Treatt's volumes.

Mark’s view

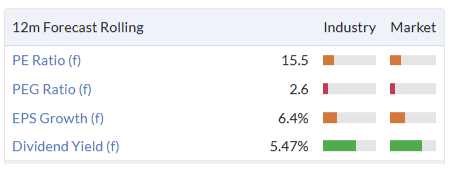

I view this update as slightly negative. The risk associated with an H2 weighting, together with potential margin pressure from lower Premium volumes and higher input costs, could lead to a miss. Even if they hit forecasts, it isn’t obviously cheap on a mid-double-digits forward P/E. Plus, its algorithmic ingredients lead to a rather blandly-flavoured Stock Rank:

However, at the back of my mind remains the fact that several industry players thought this company was worth much more than the current price last year. So while this will only interest investors taking a longer-term perspective, it isn’t without its attractions. Hence I keep our previously neutral view.

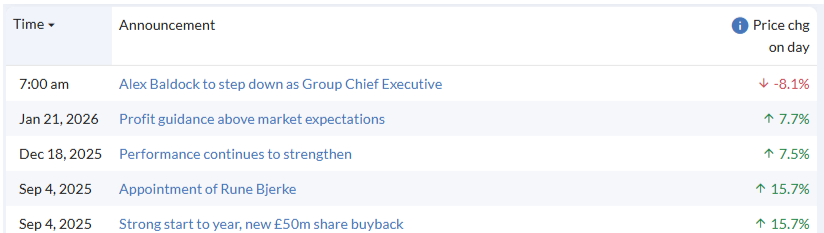

Currys (LON:CURY)

Down 8% at 121p - Alex Baldock to step down as Group Chief Executive - Mark - GREEN =

This seems quite a strong share price reaction to what appears to be a planned exit for the CEO:

The Board of Currys plc announces that Alex Baldock has informed it of his intention to step down after eight years as Group Chief Executive, to take a new external position.

The Board will commence a formal and thorough recruitment process for Alex's successor, considering both internal and external candidates, and will provide an update in due course. During this time, Alex will remain in role, continuing to drive business performance and ensuring a smooth and orderly transition, supported by his leadership team.

Of course, the market is viewing this in the context of a share price that trebled in two years under his stewardship:

However, zooming out, the share price was 190p or so, when he joined in February 2018, and is 121p today:

So if we are to give him a large part of the credit for the recovery, are we also to judge him harshly due to the decline during the first six years of his reign?

Perhaps the market is suggesting that if there was further significant progress in Curry’s business in the short term, he would have stayed. But equally, after 8 years, he may just fancy a change.

The other factor that may be impacting the price is that there is a trading statement included in the RNS:

Since the Peak trading update on the 21 January 2026, the Group has traded in-line with expectations and continues to expect Group adjusted profit before tax of £180-190m, +11-17% YoY. For the year-end 2 May 2026 we expect net cash to be above the £100m target.

I guess some may be disappointed that there has been no further upgrade to expectations, given recent trends:

However, when the January trading update was released, this caused a jump in the share price, and trading is still in line with this:

With this trading update presumably being added to assuage any shareholder concerns around the CEO resignation, there is also the chance that the more detailed full-year trading update due to be released on 19 May 2026, will continue this momentum.

Although this drop seems an overreaction to me, there are a few things that give me pause for thought:

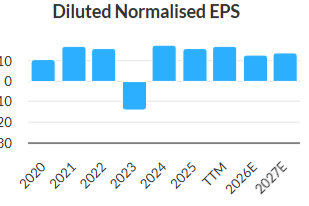

EPS drop: Although the FY26 and FY27 estimates have been continually upgraded, they are still behind the figures delivered in recent years:

Technicals: The share price has recently dropped below its 200-day Moving Average, which may indicate further weakness to come. I am consistently surprised how many institutional investors seem to simply be Momentum traders rather than fundamental analysts. However, the 50-Day MA remains at 140p, so there is no sign of an imminent “death cross”

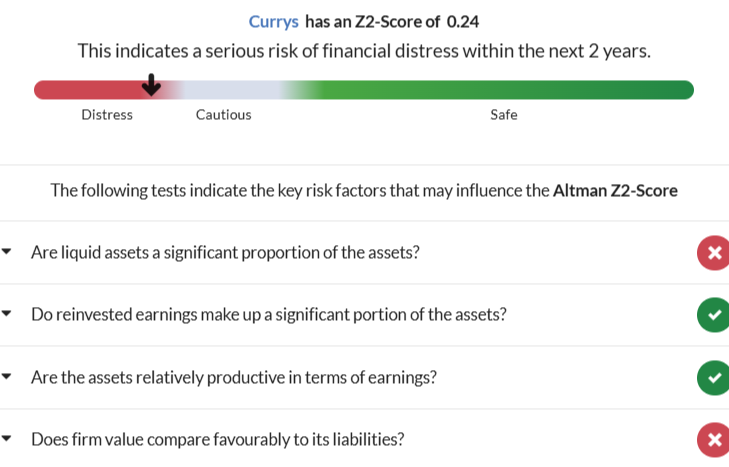

Balance sheet risk: In this update, the company reports net cash above £100m, they have the typical working capital profile of a retailer; getting aid upfront before they pay suppliers. This would leave them vulnerable if there was a significant downturn in sales, as the Z–Score highlights:

Mark’s view

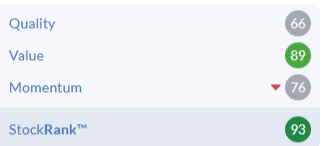

The share price drop today doesn’t make a lot of sense to me. While I have some concerns over the falling share price Momentum, the fundamental Momentum still seems to be with the business, and it remains cheaply-rated:

With trading confirmed as in line with recently upgraded expectations, I don’t think the planned exit of even a well-regarded CEO should change our positive view here. GREEN

Pollen Street (LON:POLN)

Up 8% at 800p - Full Year 2025 Trading Update - Mark - GREEN =

The market had been climbing a wall of worry here since we last reviewed this Private Credit and Private Equity fund manager:

The words Private Credit have become marred in investors minds due to rising default fears, concerns over high exposure to software firms vulnerable to AI disruption, and the need for liquidity, forcing major funds like Blackstone and Blue Owl to cap redemptions.

Today’s update shows this worry to be largely unfounded for Pollen Street, at least in the short-term:

When Graham reviewed their Q3 update they reported AUM +9.9% in the quarter to £6.7 billion and fee-paying third-party AUM +9.7% in the quarter to £5.1 billion. So the actual increases in Q4 are not that impressive at +2% fee-paying AUM. They are still benefiting from a very strong H1.

Costs are rising faster than Fund Management Income meaning Fund Management EBITDA only rises 17%. However, EPS comes in at 93.7p which is a sizeable beat on the 80.2p in the Stock Report, and puts them on an 8.5x P/E , even after today’s rise.

Like many asset managers, this business is asset-light, and they pay out a good proportion of their earnings as dividends. In this case, 58p for the full year also exceeds the forecast number in the Stock Report and is a 7.3% yield.

I can't see any forecasts but I’d imagine these will be upgraded today, as they say:

We enter 2026 with exciting momentum and a robust pipeline for both deployment and fundraising. Our strategic priorities remain clear: to continue deploying capital across our flagship funds, prepare for the next generation of investment strategies, and deliver sustainable value for our investors and shareholders.

Perhaps the most important part is that their funds are closed-end structures, so they don’ suffer form some of the issues Blue Owl and Blackstone are seeing. Plus there doesn't seem to be any short-term impact on demand, as they say:

· Significant fundraising outperformance achieved across both strategies

· Final close of Private Equity Fund V at €1.5 billion in July 2025

· Private Credit Fund IV now at £1.8 billion with further capital commitments expected ahead of an imminent final close

· £0.8 billion dry powder in Private Credit as at end December 2025, which will convert to fee-paying AUM once deployed

· Fundraising momentum and expanded investor base underpin £10 billion medium term AUM target

£10bn would be a roughly doubling of fee-paying AUM and would presumably see close to double the fund management income. Continued sector upheaval has the potential to reduce or delay this, but on the current valuation, this looks to be more like reducing the potential upside rather than being downside risk.

They directly address some of these concerns in the narrative:

Most notable is the market reaction to the potential impact of GenAI on wider society and especially the impact on the longevity of business models in certain sectors. Our assessment across the portfolio sees more opportunity than threat. Many of our portfolio companies stand to deliver impactful automation initiatives to drive margin improvements and some are seeing product enhancements driving increased sales. On the risk side, our approach to subsector diversification means we have limited overall exposure to software, and we are protected from correlation risks. Within our software investments, we have been focused on product categories which are "systems of record" which enables them to be closer to proprietary datasets such as customer records, delivering mission-critical services and operating in categories where accuracy and precision are critical success factors.

I’d put that down as cautiously optimistic.

Mark’s view

It seems that Pollen Street have little exposure to the events that have given Private Credit a bad name. This doesn’t mean that they will be immune from sentiment towards this asset class as they admit “This has resulted in investors become increasingly nervous about the credit quality of loans being written, borrower friendly structures and looser documentation.” However, the signs are that this hasn’t impacted their ability to raise AUM across both of their strategies. As such they look like they will continue to grow AUM and generate higher management fees, the majority of which wil be paid out as dividends.

Today’s beat on expectations shows that momentum is still with the business, although the big change in fee-earning AUM occurred in H1 rather than H2.

The Stock Rank still high, and likely to take a further step upwards once today’s figures are digested by the algorithms:

With the performance better and the share price lower than when Graham viewed this GREEN in November, I don’t see any need to change our positive stance.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.