Good morning!

As many readers noticed, the Burford Capital (LON:BUR) share price collapsed 42% on Friday, after a US court ruling went against them regarding Argentina's takeover of the energy company YPF. Commiserations to anyone holding that one. We may do a writeup on it today - it's a complex situation.

Market open: the FTSE is set to open slightly lower at about 9950.

In the Middle East, the Iran war appeared to escalate over the weekend with the additional involvement of an Iran-aligned group in Yemen - the Houthis - who are capable of further disrupting shipping in the Middle East. 3,500 additional US troops have now arrived in the region. Brent crude (for June delivery) is up $2 this morning to $108.

All done for today, thanks everyone. Spreadsheet accompanying this report: link.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

GSK (LON:GSK) (£83bn | SR92) | Bepirovirsen accepted for review in China & Exdensur approved for severe asthma in China | Bepirovirsen (potential cure for Hepatitis B) submission supported by “clinically meaningful functional cure rates”in Phase III trials. | |

Greatland Resources (LON:GGP) (£3.4bn | SR92) | Telfar grows by 4.8Moz to 8.0Moz, with M&I Resource up 163% to 3.8Moz. Havieron unchanged. | ||

HICL Infrastructure (LON:HICL) (£2.24bn | SR77) | Additional 6.65% interest in Cross London Trains, takes HICL’s total interest to 13.13%. Expected to add >1.0p to NAVps on completion. | ||

Keller (LON:KLR) (£1.36bn | SR98) | Previously announced £100m buyback begins today and is expected to complete by 31 March 2027. | ||

CVS (LON:CVSG) (£794m | SR38) | CEO Richard Fairman is to retire for personal reasons. He will remain in post until a successor is appointed. | ||

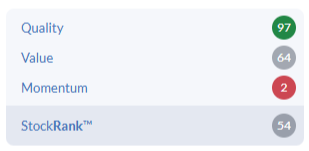

Burford Capital (LON:BUR) (£740m | SR20) | Statement re YPF Appeal Decision (27/3) & Further Statement on YPF | US Court of Appeal has reversed the lower court decision, ruling against Petersen and Eton Park [Burford]. Further legal options are being considered. Material write-down expected. Debt levels manageable but higher than “ideal”. | AMBER/RED (Graham) On balance, I’m moderately negative on this. It could offer some reasonable value here, but I think caution remains the most sensible approach for those without specific expertise. Stockopedia's categorisation of the stock as a "Value Trap" seems fair. |

Metals Exploration (LON:MTL) (£367m | SR94) | Construction at La India is ahead of schedule at 40% complete vs 35% scheduled. First gold from La India on track for Dec 26. | ||

Fuller Smith & Turner (LON:FSTA) (£345m | SR93) | Appointed Katie Horner (Head of Finance) to become new CFO Designate from 1 Sept 26. Will assume the role when the existing CFO retires in November. | ||

PayPoint (LON:PAY) (£342m | SR52) | FY26 results (y/e 31/3) expected to be “broadly in line with expectations”. Will reorganise business into four units. FY27 outlook: expect profits to exceed FY26 and be “within the range of market expectations”. | GREEN ↑ (Graham)

Given the value on offer, I’m fully positive on this one. I like the mix of old and new businesses contained within the group, including some with very strong competitive positioning, which combine to generate a very high level of profitability. I’m therefore going to upgrade this to GREEN (from AMBER/GREEN). It might be a little foolhardy, considering the recency of the profit warning, but it reflects my view. | |

Big Technologies (LON:BIG) (£246m | SR51) | ARR +12%, revenue +3%. Adj op profit up down 12.7% to £18.5m. Pro forma year-end cash of £61.9m. Continuing efforts to settle the litigation with the Founder. FY26 outlook: in line with expectations. | ||

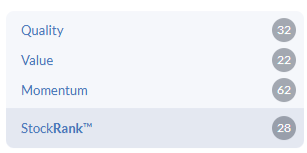

Boohoo (LON:DEBS) (£242m | SR28) | FY26 adj EBITDA of £53m, ahead of previous guidance of £50m. FY27 EBITDA guidance raised to “double-digit” growth. | AMBER/RED = (Roland) Boohoo has upgraded FY27 guidance for the second time this year and is now expected to report positive adjusted EPS for y/e Feb 27. Despite this, I’ve opted to remain cautious for several reasons. These include the forward P/E of 14 and the continuing fall in sales. I may be missing the start of a genuine comeback, but my personal view is that the company still needs to prove its evolving business model can deliver on its promise. I’m happy to align with the StockRanks and maintain a cautious view for a little longer. | |

Capricorn Energy (LON:CNE) (£194m | SR97) | Egyptian govt has ratified agreement covering eight existing Western Desert concession agreements held jointly with Cheiron. | ||

Jadestone Energy (LON:JSE) (£152m | SR58) | Stag Field was closed down ahead of Cyclone Narelle. There were no hydrocarbon leaks but there was some storm damage to the facilities. This is currently being assessed. Insurance is in place to cover damage and loss of production income. | ||

Gaming Realms (LON:GMR) (£85m | SR45) | Revenue up 10%, pre-tax profit up 5% to £8.8m. £6m buyback announced, £18m net cash. Outlook: expects to continue growing in new and existing regulated markets. Confident of prospects for the current year. | ||

accesso Technology (LON:ACSO) (£80 million | SR69) | Revenue up 1.8%, pre-tax profit up 37.7% to $14.3m. Saw “pressure on our customers’ revenue streams”. CEO to retire. 2026 outlook in line with expectations. Has acquired Dexibit for $7.1m, an analytics and AI platform for the visitor attractions industry. | ||

Bioventix (LON:BVXP) (£72m | SR54) | Revenue down 8.5%, pre-tax profit down 4% to £4.85m. Tau/neuro royalties up 5x to £150k. FY26: trading in line with expectations. Cavendish forecasts unchanged: - FY26E adj EPS: 136p - FY26E dividend: 150p | AMBER ↑ (Roland - I hold) This niche biotech has reiterated full-year guidance today (for y/e 30 June) and reported continued progress with the development of antibodies for Alzheimer’s blood tests. Commercial adoption remains some time away and is not guaranteed, so investors need to form their own view on valuation and the company’s prospects. However, I think the results reported today justify removing my previous negative view and upgrading to neutral. | |

Robert Walters (LON:RWA) (£61m | SR41) | CFO to retire, replacement appointed with previous experience including SABMiller, C&C and Greencore. | ||

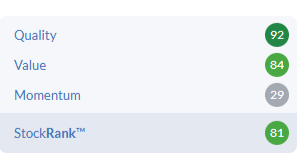

Spectra Systems (LON:SPSY) (£62m | SR81) | Revenue up 30.7%, adjusted EPS up 100% to 37.8c. Dividend of $0.136 per share. Confident in short and long-term opportunities. | AMBER/GREEN ↑ (Roland) As expected, 2025 results were exceptionally strong due to the lumpy recognition of revenue and earnings from the company’s big sensor contract. Earnings are expected to fall in 2026, but broker forecasts for this year have been upgraded today and Spectra’s balance sheet and cash flow remain of high quality, in my view. For investors who believe in the value of the growth and diversification opportunities highlighted by today’s commentary, I think the current valuation could be of interest. | |

Ten Lifestyle (LON:TENG) (£61m | SR74) | New multi-year contract with “an existing global client”. Expects to launch by 31 August 26, will be categorised as a Medium contract in FY27. Separately, also agreed new platform launch under existing Large contract in Japan. | ||

Touchstone Exploration (LON:TXP) (£41m | SR36) | The Carapal Ridge 3 ("CR-3") well was successfully tied into the Central block natural gas facility and brought onstream on March 28, 2026. Gross natural gas throughput (excluding Coho-1 volumes) has increased from approximately 16 MMcf/d to 19 MMcf/d. | ||

Aoti (LON:AOTI) (£35m | SR40) | Revenue +14% ($66.5m). Adjusted EBITDA -6.4% ($7.5m). Outlook: “...AOTI has adapted where needed to navigate market headwinds and is positioned for sustainable revenue and Adjusted EBITDA growth over the medium and longer term.” 2026 to be “a transitional year”. | ||

Clean Power Hydrogen (LON:CPH2) (£30m | SR9) | The first of the Company's 1MW MFE220 units has left the factory to complete the third and final stage of its Factory Acceptance Test. Various other operational developments. | ||

Emmerson (LON:EML) (£30m | SR19) | EML’s legal representatives, Boies Schiller Flexner LLP, have submitted its Memorial in accordance with the timetable set out by the arbitration panel. | ||

Artisanal Spirits (LON:ART) (£22m | SR18) | “...a mixed but resilient year-on-year performance”. Adjusted EBITDA loss £1.9m. Adjusted loss before tax £6.5m. FY26 guidance remaining unchanged. | AMBER/RED ↓ (Graham) I was previuosly neutral on this, noting the company's claim to have spirits on the balance sheet worth £100m. Today's results show the company's EBITDA loss deepening - and readers will remember that adjusted EBITDA losses are something I find it very difficult look past. The pre-tax loss of £7m has resulted in the net debt position expanding to £31.5m. While the company still points to the value of its stocks as a source of value, this is the type of "deep value" investment that I've learned to stop believing in, except where there is a clear catalyst for the value to be unlocked. While I do still think ART could be undervalued, the absence of a catalyst and the existance of EBITDA losses sees me taking a moderately negative stance for the time being. I don't think it has ever made a profit. | |

Team (LON:TEAM) (£19m | SR13) | Acquires eight investment mandates with £157m AUM for £1m. Acquires a Guernsey-based financial planning business for £880k. Both to be paid for with new TEAM shares. | ||

Abingdon Health (LON:ABDX) (£18m | SR23) | Series of significant contracts with a USA-based customer to develop, and scale up to manufacture several multiplex quantitative lateral flow assay systems. £4.8m value to be delivered over c. 27-month period. Cavendish note: no change to revenue forecasts. | ||

Fusion Antibodies (LON:FAB) (£16m | SR5) | Agreement to transfer the ownership of certain IP owned by Fusion to a client, Finn Therapeutics. The IP Transfer Agreement covers a novel rabbit antibody. One-off payment £250k. | ||

Genedrive (LON:GDR) (£16m | SR13) | Revenue £0.57m. Operating loss £2.6m. Raised £4.6m in March 2026. Outlook: well funded to build on the progress achieved during the period. | ||

RTC (LON:RTC) (£14m | SR99) | Subsidiary Ganymede has been awarded new and extended contracts with major UK infrastructure and energy clients (framework contracts with no minimum volumes or guarantee of revenue). | ||

Jangada Mines (LON:JAN) (£12m | SR24) | 13 holes drilled for a total of 2,076 metres primarily targeting the high-grade Molly 1 & 2 targets. Highly encouraging indications. | ||

Directa Plus (LON:DCTA) (£9m | SR35) | In advanced discussions with an institutional investor for the provision of up to £2.5m to extend the Company's cash runway. |

Graham's Section

PayPoint (LON:PAY)

Up 1% 567p (£346m) - FY26 Update, Business Reorganisation and FY27 Outlook - Graham - GREEN ↑

We last checked this one at the Q3 update in January. We now have the full-year update.

Let’s summarise:

FY March 26 broadly in line (typically code for “slightly below”)

Buyback ongoing: share count reduced by 15%, on track to reduce it by 30% by FY March 28

Business reorganisation: this is welcome news, as it’s often tricky to explain what PayPoint actually does. Hopefully this will help. The new structure is:

Network Services

Digital Payments & Open Banking

Love2shop

Merchant Services

This new structure will create “a more accountable operating culture” - great.

Network Services (revenue £91m) - community services provided via 30,000 convenience stores. Cash bill payments, parcel collect and drop off, cash banking, gift cards, etc.

Digital Payments & Open Banking (revenue £13m) - includes various services enabling secure payments for major organisations, providing confirmation of payee/verification of payee, and performing real -time credit credit checking.

Love2shop (revenue £53m) - gift cards.

Merchant Services - in-store and online card payments. Includes PayPoint (10,000 retailers) and Handepay (20,000). This division will see “a fundamental reset of the strategy”.

An example of the new strategy:

…we will stop targeting low value, high-churn merchants in a market segment that has become increasingly competitive and purely price focused… Execution of this strategy will deliver a higher quality merchant acquiring estate, a focus on net revenue, improved profitability and a merchant estate managed for value rather than a focus on merchant estate growth.

This all sounds positive to me.

FY27 outlook

The new strategy “will drive significant change” in FY27 and beyond. But the company is still expecting a result within the range of expectations:

In terms of trading, our outlook for the year ahead is balanced between the continued growth across the Group, further cost efficiency initiatives and recent trends in certain of our business units, in particular our parcels business. Overall, this indicates the business is likely to exceed the underlying profits delivered in FY26 and within the range of market expectations.

Capital allocation remains generous to shareholders:

In FY26, in total through a combination of share buybacks, ordinary and special dividends, the Group will have returned more than £90 million in value to shareholders in the year. The business remains on course to reduce its issued share capital by circa 30% in the three years to FY28 while continuing to grow the ordinary dividend, with share capital already reduced by c.15% in the current year.

Graham’s view

This warned on profits in November, causing a fairly serious share price reaction:

The hit to EPS forecasts was real and they have not rebounded:

The FY27 EPS forecast is now 83p, vs. 97p before the profit warning.

In that context, it’s difficult (not impossible!) for me to be outright positive on the stock. Our methodology tends to take profit warnings very seriously, and I do try to stay consistent with that.

However, I personally am very bullish on PayPoint - I’ve been a long-term fan of this company, and I’m now excited to see how much the share count is reducing via buybacks.

These buybacks is on top of generous dividends, and the company has declared an intention to increase its dividend while simultaneously reducing the share count (of course dividends become more affordable when there are fewer shares).

Net debt was last seen at £84m (September 2025). This might seem high, but operating profit is expected to come in at close to £80 million for FY26, and then exceed £80 million in FY27. At this level of profitability, I personally don’t view this debt as a worry.

Buyback efforts: PayPoint were previously targeting a share count reduction of “at least 20%”, but are now aiming for 30% over a multi-year period. This will depend to some extent on the shares remaining cheap. But the intention is there. With the shares still trading at around 7x earnings, I think it makes sense to continue aggressively buying their own shares..

In summary, given the value on offer, I’m fully positive on this one. I like the mix of old and new businesses contained within the group, including some with very strong competitive positioning, which combine to generate a very high level of profitability.

I’m therefore going to upgrade this to GREEN (from AMBER/GREEN). This might be a little foolhardy, considering the recency of the profit warning, but it reflects my view.

Burford Capital (LON:BUR)

Down 6% at 319.6p (£683m / c. $900m) - Graham - AMBER/RED

Burford was trading at 583p last week, until the bombshell announcement that the YPF case was going against it.

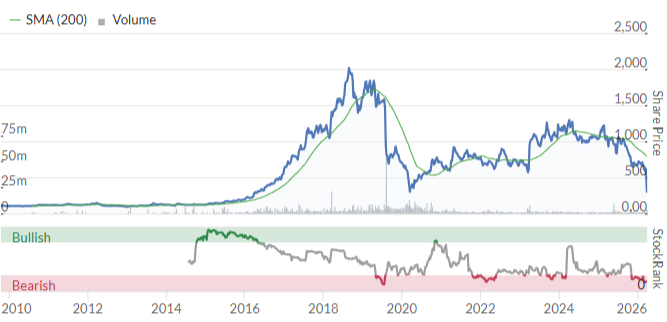

This is a share that we used to discuss a lot here. It had a tremendous run up in value (see below). Astonishingly, it has now given back most of those gains.

The company is a pioneer in litigation finance: investing in large legal cases and taking a cut of the eventual settlements.

We did eventually stop covering it, partly due to its size and partly due to the complexity involved. When it comes to a business like Burford, it’s difficult for mere mortals and non-legal experts to assess what is going on under the hood.

The risks involved are fundamentally difficult to predict - how can anyone predict the outcome of the legal case between Argentina and former shareholders of YPF, the energy company it nationalised? This is a landmark case financed by Burford.

The only way to manage this risk sensibly is through diversification. However, given the share price reaction in recent days, it’s pretty clear that the level of diversification achieved by Burford in 2026 was not sufficient to protect it.

Let’s dig into the announcements.

Friday: Burford Capital Statement Re YPF Matter

Burford acknowledges the ruling of the US Court of Appeals for the Second Circuit (not ideal to have this out at 3.32pm in the afternoon, but it was unavoidable).

Monday (today): Burford Capital Statement Re YPF Appeal Decision and Burford Capital Further Statement on YPF

Let’s outline some of the key facts.

While the Court appears to have agreed with those seeking compensation from Argentina on many of the facts of the case, it still reversed the prior decision of the District Court:

“...the majority proceeded to hold that Argentina's commitment to make a tender offer was not enforceable by the shareholders who relied on it, in a remarkable abdication of the Second Circuit's role as a guardian of the rights of NYSE investors. In essence, the majority held that promises like these - central to the operation of the US capital markets - cannot necessarily be enforced.

The majority also held that… [the claims of the plaintiffs] should have been brought in the Argentine expropriation compensation process, a process uniquely poorly designed to give US investors the benefit of the bargain promised in the Bylaws.

Next steps: the plaintiffs are likely to seek a rehearing and if that is not granted, will consider steps such as taking it to the Supreme Court. There is also the potential to seek investment treaty arbitration, away from the US courts.

Impact on Burford: there could be an immediate impact on the company’s financial flexibility.

Given the substantial carrying value of the YPF matter on Burford's balance sheet, a material write-down could reduce Burford's balance sheet equity value below the level required under the indentures governing our senior notes to incur additional debt…which would limit Burford's ability to issue new debt. Our ability to make restricted payments or permitted investments based on our debt to equity ratio also could be limited.

Turning to the second RNS issued this morning, here’s a CEO comment:

Although the outcome was disappointing, we have always treated YPF as separate and apart from Burford's core business. Burford is run on a cash basis, and does not rely, or count on, cash from the YPF case to operate the business; YPF has always been additional to the core business, and we have repeatedly described it that way.

Our core business is based on a portfolio of many hundreds of valuable cases ― a portfolio we expect to produce more than $5 billion in cash proceeds over time and that produced more than $1.2 billion in cash in just the last two years.

He says that the carrying value of the YPF asset will be written down, but this “will have no cash impact”. This is obviously a very narrow way of looking at it - the YPF asset was expected to generate a large amount of cash in future years, and that is now seriously in doubt.

In terms of Burford’s debt levels, he says:

We are sensitive that we now have more debt than the level we previously suggested was ideal. That said, we believe we are still not highly leveraged, we have carefully laddered our debt maturities to stretch out over the next eight years, and managing our debt load will be front of mind as we proceed.

The company has “more than $700 million in cash, cash equivalents and marketable securities on hand”.

And some reassuring words on the nature of the debt outstanding:

Our 144a debt is all unsecured and does not have financial covenants that we are obliged to maintain; we are not, for example, subject to a maximum debt/equity ratio or any such concept. Rather, our debt only has "incurrence covenants" that restrict our ability to incur additional debt or take certain other actions….

Graham’s view

Checking the company’s most recent 10-K, for December 2025, I see that Burford had third-party indebtedness of some $2.1 billion.

And they did express an intention to issue more debt (maybe):

Going forward, we expect to continue to be an opportunistic issuer of debt securities and may issue new debt securities from time to time to fund our growth or refinance future debt maturities, among other things…

So if covenants will now prevent them from doing that, that is at least one way in which the YPF matter will now immediately restrict their ability to operate as they would have liked.

The December 2025 balance sheet shows shareholder equity of $2.5 billion.

Elsewhere in the report, I find an entry for “YPF-related assets” worth $1.7 billion.

This is probably too simplistic and could be totally mistaken, but what if I just assume that YPF-related assets are worthless - can I get a rough new estimate for balance sheet equity of $0.8 billion?

That would make some sense in relation to Burford’s current market cap, which is equivalent to c. $900m.

However, would I be willing to value Burford at that level? Probably not.

Let’s review some pros and cons.

Reasons to be positive:

The remaining Burford portfolio of legal cases is likely much better diversified.

There is still the potential for a win at a rehearing, the Supreme Court or arbitration.

The covenants on existing borrowings do not seem fatal for shareholder value.

Reasons to be cautious:

The amount of leverage involved now, relative to the company’s worth, is no longer comfortable (e.g. borrowings could be worth double the company’s equity now).

The value of the remaining portfolio is still not something I’d have total confidence in - legal investments strike me as far more exotic than business investments.

Tripping over covenants is always a red flag, even if it’s not fatal.

On balance, I’m inclined to put this on AMBER/RED. It could offer some reasonable value here, but I think caution remains the most sensible approach for those without specific expertise.

Stockopedia's categorisation of the stock as a "Value Trap" seems fair:

Roland's Section

Bioventix (LON:BVXP)

Up 9% at 1,492p (£78m) - Interim Results - Roland - AMBER ↑

(At the time of writing, Roland has a long position in BVXP.)

We are increasingly confident that our progress in the development of SMAs for use in assays for the diagnosis of Alzheimer's disease and other neurological conditions will materialise in tangible commercial success.

Bioventix develops antibodies used in clinical blood tests, selling these to In Vitro Diagnostics (IVD) specialists such as Roche and Siemens for use in their blood testing machines. Today’s results appear to have provided some relief to investors who were concerned about the risk of an unstoppable decline in profits at this quirky biotech.

Full-year results for the year-ending 30 June are expected to be in line with expectations and there’s further evidence of momentum in the company’s pursuit of a role in future clinical tests for Alzheimer’s Disease.

HY26 results summary

The fall in sales and profits reported today provides a tangible reminder of the importance of the Alzheimer’s antibodies to Bioventix. The company’s core portfolio of commercial antibodies is largely mature and is also facing a significant increase in competition and pricing pressure in China, a major market.

Sales of our vitamin D antibody and other core antibodies were all broadly in line with last year's sales reflecting the mature nature of the diagnostic products that our core antibodies support. As we have reported previously the challenging market conditions in China have led to the loss of some limited revenue streams.

Our sales relating to troponin antibodies were steady.

The commercial success of the company’s Alzheimer-related antibody portfolio probaby presents the only near-term opportunity for a return to growth.

With that said, today’s numbers are

Revenue down 8.5% to £6.16m

Pre-tax profit down 4% to £4.85m

Net cash up 4% to £5.3m

Interim dividend unchanged at 70p per share

Tau/neuro royalties increased five-fold to £150k

Trading remains in line with expectations for the year ending 30 June 2026

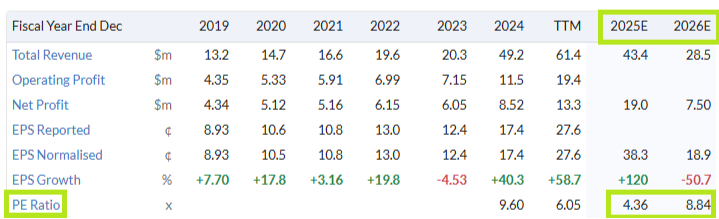

Bioventix’s QualityRank of 97 provides us with a clue about the high quality of its financials. These results show an operating margin of 77.6% and free cash flow of £3.7m prior to working capital movements, giving 100% conversion from net profit of £3.6m.

The only slight weakness is that dividend cover is still not quite restored – the interim dividend of 70p is marginally ahead of half-year earnings of 69.4p per share. I don’t see any need to quibble over this, given the improved net cash position.

Management statement: CEO (and 5.8% shareholder) Peter Harrison devoted the vast majority of his statement to the Alzheimer’s-related portfolio.

Bioventix is already generating royalties from some of these antibodies that are in use by researchers developing new blood tests. I should emphasise that this usage is research only – there are no currently approved commercial tests.

Alzheimer’s-related royalties in H1 were double those earned during the whole of last year:

H1 25: £30k

FY 25: £75k

H1 26: £150k

While there’s no certainty Bioventix antibodies will be chosen for future commercial blood tests, this rapid growth in royalty revenue does seem to suggest growing interest from the IVD testing industry – royalties are earned each time the antibody is used in a test.

The company backs up the figures today with more details of how its antibodies are in use in assay (test) designs. The “current leading blood-based biomarker assay for amyloid build-up” (a key part of Alzheimer’s pathology) is B-D pT217. Harrison says that three of the “leading IVD companies” and three “rearch-oriented platform companies” are using “at least one” Bioventix antibody in their B-D pT217 assay designs – six companies in total.

At the end of last year the company reported three active commercial partners for B-D pT217. So assuming the categorisation of partners is consistent, the number of companies using Bioventix antibodies to develop this particular test design has doubled in six months.

Similarly, for “brain-derived Tau” Bioventix mentions eight companies using Bioventix antibodies today, compared to five “active commercial partners” at the end of June 2025.

Outlook

We remain confident in the outlook for the year to 30 June 2026 and believe there are many reasons to be positive with the opportunities in the diagnosis of Alzheimer's and other neurological diseases.

Full-year guidance is unchanged and this is confirmed in an updated note from house broker Cavendish today – many thanks.

FY26E adj EPS: 136.0p

FY26E dividend per share: 150p

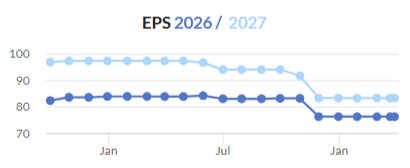

Unchanged forecasts are encouraging, but it’s worth noting the deteriorating trend in earnings. Cavendish also has not yet provided any forecasts for FY27, despite the new year starting in just over three months’ time.

Roland’s view

Uncertainty over Bioventix’s future earnings potential remains, but today’s results are in line with previous guidance and show continued progress with the company’s Alzheimer’s-related portfolio.

The share price has also fallen significantly since the company’s FY25 results were reported in October:

As a result, Bioventix shares now trade on a forward P/E of 10 with a 10% dividend yield. This is an unusual combination that’s reflected in the stock’s Contrarian styling and StockRank:

Broadly speaking, my valuation estimates suggest the stock is trading at fair value or slightly below, as long as the current level of profits (and dividends) remains stable.

Given the company’s exceptional profitability, I think any sustainable growth from this level could result in a significant re-rating of the stock. However, there’s no guarantee profits will stabilise or return to growth. Commercial Alzheimer’s antibodies may be unsuccessful or delayed. Competition in China could continue to erode high-margin royalties. I think it’s entirely possible that profits could fall further, with no guarantee of a return to historic levels.

To reflect today’s in line guidance and the mix of potential outcomes I’ve outlined above, I’m upgrading my view from AMBER/RED to AMBER, or neutral, today. Investors need to form their own view on outlook and valuation before investing in this rather illiquid stock.

Personally, I remain a holder and am more likely to top up than to sell, based on today’s results.

Spectra Systems (LON:SPSY)

Up 7% at 135p (£66m) - Audited results for the year ended 31 Dec 25 - Roland - AMBER/GREEN ↑

Today’s results from this banknote authentication and brand protection specialist read very bullishly, with revenue up 31% and earnings doubled from 2024 levels. Brokers covering the stock have also upgraded their 2026 forecasts today.

However, Graham and Mark have both been neutral on this business since November (here, here & here), despite the seemingly affordable valuation. I’m interested to see if we can justify taking a more positive view following this update.

2025 results summary

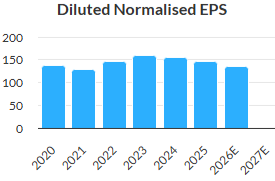

Today’s headline figures certainly show a remarkable improvement in financial performance. However, while revenue appears to be comfortably ahead of previous Zeus forecasts of $55m, profits are in line with expectations:

Revenue up 30.7% to $64.3m

Adjusted pre-tax profit up 109.4% to $25.2m

Adjusted earnings up 100% to 37.8 cents per share

Net cash up 29% to $11.6m

Annual dividend of $0.136 per share (2024: $0.116), to be paid in July

Trading commentary: Spectra is understandably coy about the identity of its customers, many of whom are central banks. Today’s results mention HMRC, Royal Mail and Brazilian bank note printers Casa de Moeda, but most other customers go nameless.

What we are told is that last year’s strong growth was “primarily driven by sensor production revenue recognition”, reflecting the “partial completion of the sensor order for our long-standing customer”. This generated revenue recognition of $22m and hardware sales of $7.3m, together with a $5.7m cash payment last year. The contract is scheduled for completion in 2026.

Spectra also reports that it agreed a sensor maintenance contract “with our customer” that should be worth $6.7m from 2026-2030. I assume it’s the same customer.

Other highlights from the year included:

$4m four-year hybrid stamp contract in the UK.

House note with Fusion substrate and covert machine readability in Brazil.

Successful print trials of our smartphone authentication technology with the “Police Office of a major middle eastern country”.

Gaming software security business “produced record revenues and profitability”.

The accounts highlight the attractive quality metrics of this business, as hinted at by the StockRank:

Profitability was excellent:

Operating margin: 37.8% (2024: 23.3%)

Return on capital employed: 42.2% (2024: 24.4%)

Return on equity: 39.4% (2024: 25.3%)

Cash flow was held back by working capital outflows into inventory and receivables totalling nearly $11m. However, adjusting for these flows – which seem logical given last year’s increase in revenue – my sums show the group’s free cash flow was almost a perfect match for its net profit – another quality signal.

Outlook

September’s profit warning was caused by delays to key contracts and today’s outlook commentary makes further mention of slow sales cycles:

Despite delays which are part of the sales cycle with government customers, we have and will continue to navigate through the opportunities with unstoppable determination to achieve growth through sales of our Fusion Substrate and smartphone technology in the near future.

Even so, CEO Nabil Lawandy is confident in the company’s “short-term opportunities”. These include:

The completion of the sensor contract (and related increase in unrestricted cash).

Qualification of the company’s polymer substrate (for bank notes) with another central bank.

Expansion of the “higher margin hybrid stamp sales to two additional postal authorities”.

Adoption of our smartphone technology and sale of our materials for several billion tax stamps per annum.

On a longer view, Lawandy points to “increase of covert authentication material sales”, plus revenue stamps for spirits and vape sales.

Broker forecasts: with thanks to both Zeus and Allenby Capital for publishing on Research Tree, we have upgraded estimates for FY26 today.

The two brokers’ estimates are fairly consistent, but they confirm the existing consensus view that a significant reduction in revenue and earnings is likely in 2026:

Allenby: FY26E revenue / adj EPS: $38.2m / 16.6c

Allenby FY26 previously: $28.0m / 14.8c

Zeus: FY26E revenue / adj EPS: $37.2m / 16.9c

Zeus FY26 previously: $29.1m / 14.9c

Roland’s view

It looks like 2025 results were boosted by a significant one-off recognition of revenue and profits from the company’s sensor contract. This may partly explain why the stock was valued as it was prior to today:

Progress is expected to be more muted in 2026, but the business does appear to have plenty of medium-term opportunities for further growth and diversification.

The share price has now fallen back to the level it was at prior to the big sensor contract win (I think). I would speculate that this could be an attractive entry point for investors who are confident in the medium/long-term growth opportunity here:

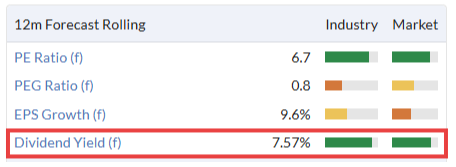

Another possible indicator of value is the 7.5% dividend yield, which is comfortably covered by earnings forecasts for 2026.

The big risk with this business has always been seen as the expected decline in banknote usage globally. However, perhaps this view is a little too parochial and narrow – while cash usage is declining in some countries, it remains very substantial globally and I suspect will remain so for the foreseeable future. Spectra also continues to develop other growth opportunities with the potential for good longevity.

While the outlook beyond the current year remains uncertain (there are no 2027 forecasts as yet), I think the value and quality on offer here are sufficient to revert our view to AMBER/GREEN, in line with our view prior to last year’s profit warning.

Boohoo (LON:DEBS)

Up 1% at 17.6p (£282m) - Trading Statement - Roland - AMBER/RED =

Today’s update from this fast-fashion group leads with some impressive–sounding statements:

FY26 adjusted EBITDA of £53m “comfortably ahead of previous guidance”.

“76% increase in H2 adjusted EBITDA”

Net debt under 2x adjusted EBITDA at the end of February, now expected to fall to under 1x EBITDA by the end of February 2027

As a result of this progress, FY27 guidance has been upgraded to reflect the increase in expected FY26 results.

The big takeaway is that Boohoo is now expected to return to profit in FY27.

The only fly in the ointment that I can see today is that sales have continued to fall. Gross Merchandise Value (sales prior to returns) was 5% below prior year levels at the end of February. Even so, the improvement in profitability here seems positive.

Outlook & Estimates: what has changed?

Today’s RNS seemed to be written in a slightly haphazard style in my view, with lots of details about cost savings, leases and capex – but no clear guidance on revised expectations.

Contrary to the best practice followed by a growing number of companies, Boohoo’s management hasn’t seen fit to include details of current consensus forecasts as a reference point. The end result is that investors without access to broker notes are left without much clarity.

Here’s a summary of the changes to FY26 and FY27 forecasts, with thanks to Panmure Liberum and Zeus for publishing updated forecasts today. Note that revenue forecasts haven’t been upgraded – today’s profit upgrades are due to improved profitability rather than higher sales.

FY26 (y/e 28 Feb 26):

FY26 adjusted EBITDA: £53m (+6% versus £50m previously)

Panmure Liberum FY26E adj EPS: -1.0p (prev. -1.6p)

Zeus FY26 adj EPS: -1.0p (prev. -1.1p)

FY27:

Panmure Liberum FY27E adj EBITDA: £59.2m (+3.5% vs £57.2m previously)

Panmure Liberum FY27E adj EPS: 1.6p (previously -0.1p)

Zeus FY27E adj EBITDA: £58.3m (+5.2% vs £55.4m previously)

Zeus FY27E adj EPS: 0.9p (previously -0.1p)

Roland’s view

Today’s upgrade to FY27 guidance is the second so far this year:

This fashion retailer has cut debt successfully and is now expected to be profitable this year. Averaging the two forecasts I have access to today gives me a FY27 adj EPS estimate of 1.25p. That’s equivalent to a forward P/E of 14 at the current share price.

One positive here that I think is worth emphasising is the pace of the improvement in profitability as costs fall. According to PanLib, Boohoo’s EBIT margin is now expected to be 5% in FY27, from 2.1% previously.

If the company can pair this with a return to sales growth, then the group’s earnings could rise quickly. The caveat to this is that there’s no evidence of sales growth just yet. In fact, PanLib has cut its revenue forecasts for FY27 today, suggesting only a modest return to revenue growth in FY28.

We’ve been AMBER/RED on Boohoo for a while due to its loss-making operations and valuation, which Graham has suggested was already pricing in a recovery.

My decision today is whether to upgrade our view to neutral to reflect the company’s upgraded guidance, falling leverage and returning profitability.

It’s a close-run decision as I can see arguments both ways. The StockRanks are broadly negative, with Momentum Trap styling warning that momentum has not been supported by evidence of quality or value.

On balance, I’m also going to remain cautious and leave our AMBER/RED view unchanged for a little longer. There are a few reasons for this:

The stock still doesn’t look especially cheap to me for a retailer that’s reported a loss for each year since 2022.

Sales are still falling.

The conflict in the Middle East could potentially result in cost inflation for Boohoo, while UK consumers are also facing higher energy costs, potentially crimping demand.

I accept that I could be missing the start of a strong recovery, but I think Boohoo still needs to prove that its evolving business model can drive sales growth and sustainable profitability.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.