Good morning! This is the final report until Tuesday 7th.

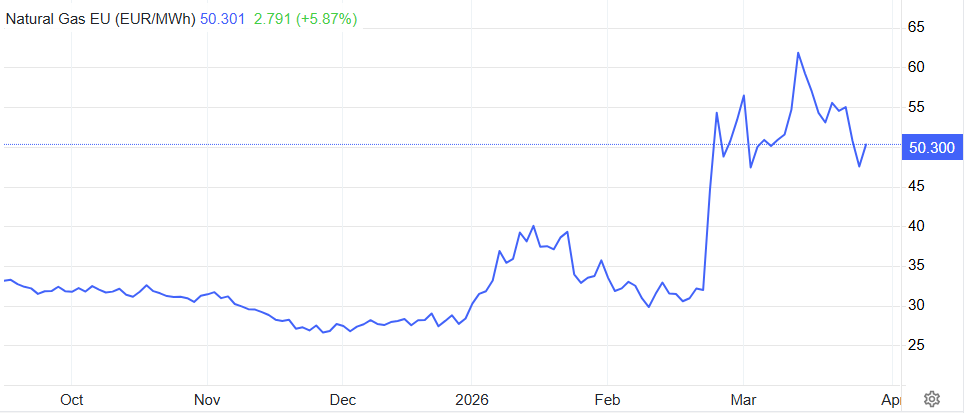

In the latest overnight moves, Brent Crude is up over $6 at $107, due to some aggressive rhetoric from Trump on Iran ("over the next two to three weeks, we’re going to bring them back to the stone ages where they belong.”).

EU natural gas prices are spiking 8% higher as a result, but are still some distance off the highs reached in March:

As for stocks, the FTSE is set to open lower by less than 1%, giving back yesterday's gains at 10,270, while other indices are faring worse: the German DAX is lower by nearly 2%, and the S&P is lower by 1.4%.

We are done, enjoy the break!

Spreadsheet accompanying this report: link.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

AstraZeneca (LON:AZN) (£233bn | SR71) | “…statistically significant and clinically meaningful improvement in the primary endpoint of progression-free survival…for patients with unresectable hepatocellular carcinoma eligible for embolisation.” | ||

Lloyds Banking (LON:LLOY) (£57.3bn | SR73) | Does not believe any change to the provision for this issue is required. | ||

Atalaya Mining Copper SA (LON:ATYM) (£1.15bn | SR94) | Has acquired 4,500,000 shares of Lara Exploration Ltd. for C$13.5m. | ||

Rockhopper Exploration (LON:RKH) (£668m | SR30) | An updated independent technical report on the Sea Lion field shows that overall gross resource volumes are consistent with the Company's previous independent resource evaluation. | ||

Halo Minerals (LON:HALO) (£443m | SR N/A) | Has contracted specialised environmental consultancy firm MSTECK SpA. They will conduct a comprehensive bio-accessibility and human health risk assessment study at Halo's Playa Verde Project site in Chañaral, Chile. | ||

McBride (LON:MCB) (£237m | SR85) | Has made a binding offer for the acquisition of Eurotab, for EUR 40 million. Eurotab is a “specialist in the design and manufacture of solid-format cleaning and hygiene solutions, primarily serving private label and certain contract manufacturing markets”. Trading update: elevated input costs in April, has informed all customers about temporary price adjustments, or surcharges to current pricing. | ||

B.P. Marsh & Partners (LON:BPM) (£236m | SR87) | Has acquired an additional 2% equity stake in Pantheon, based on an equity valuation of £275m. Shares purchased from the company’s founders. | GREEN = (Graham - I hold)) [no section below] The major downside of this investment is that it maintains BPM’s fairly limited portfolio diversification. That is a major negative, but I’ve never expected BPM to behave like a mutual fund. It’s a specialist investor and it’s entitled to focus on its best ideas. Sometimes, as with stock market investments, the best ideas are the ones we already own. | |

Sovereign Metals (LON:SVML) (£231m | SR19) | Second year of rehabilitation trials at the Kasiya Rutile-Graphite Project is nearing completion during the upcoming harvest season in Malawi. | ||

Cornish Metals (LON:TIN) (£147m | SR N/A) | “2026 will be a pivotal year as we progress project financing and a final investment decision. With strong stakeholder support, robust economics and clear development momentum, we are well positioned to advance South Crofty towards production and deliver a secure domestic supply of this critical mineral.” Going concern warning as more funding is needed to advance the project. | ||

Activeops (LON:AOM) (£133m | SR44) | Sale of the WorkiQ trademarks to Microsoft for $10m. No impact on the ActiveOps Decision Intelligence software suite of products, and the WorkiQ product will be rebranded in due course. | ||

Scancell Holdings (LON:SCLP) (£117m | SR23) | Current CFO Sath Nirmalananthan to leave on April 24 to pursue other professional opportunities. David Schilansky to serve as a financial advisor and shall become interim Chief Financial Officer. Launched a global recruitment process for a permanent CFO. | ||

Speedy Hire (LON:SDY) (£102m | SR61) | Customer led delays, affecting hire and service revenues now expected to impact the near term. Now expects FY2026 EBITDA to be c.£90m. Net debt £159m. Panmure Liberum: “We reduce our FY 26 and FY 27 EBITDA by 15% and 12%, and expect a small loss before tax in FY 26” Cannacord: “ we cut our FY26E EBITDA estimate by 16% and raise net bank debt by 10%....reduce FY27E/28E EBITDA by 5%/3%” | BLACK (AMBER/RED ↓) (Mark) This company may well look cheap if they hit forward forecasts. However, I have some significant doubts about their ability to do this given today’s profits warning. There is some asset backing at these levels which is probably why the drop today is relatively light compared to EPS forecasts that are now for a loss in FY26 and have been almost halved for FY27. The value of those assets are subject to the depreciation policy being correct, while the large debt levels are not open to judgement. So in keeping with the Stockopedia research that suggests negative news tends to be followed by a further drift downwards in share price, I am reducing our view by one notch. | |

Tracsis (LON:TRCS) (£91.5m | SR62) | Vesputi, a German digital ticketing technology provider acquired for €5.8m (c.£5.1m) with additional consideration of up to €2.4m (c.£2.1m). No profitability given but expected to be earnings enhancing. | AMBER = (Mark) Some investors will appreciate the continued desire to acquire complimentary businesses, as this has been the key growth driver of the company over the years. However, others will be concerned with the multiple paid, which looks like it may be significantly higher than Tracsis shares currently trade on. Overall, this is a relatively small bolt-on that doesn’t move the dial (or our previously neutral view) either way. | |

Christie (LON:CTG) (£35.2m | SR86) | Reached agreement with all scheme members to cease active membership effective from 6th April 2026, and transfer to DC pension arrangements. | ||

Satsuma Technology (LON:SATS) (£22m | SR0) | Cost reduction strategy expected to reduce opex from £6.7m to £2.7m. One off costs £1.35m. Acquired 25.65 BTC. | RED = (Mark) | |

Cadence Minerals (LON:KDNC) (£19.3m | SR50) | No additional archaeological field studies are required in the previously impacted areas. Project remains in execution readiness…subject to receipt of the required permits | ||

Sundae Bar (LON:SBAR) (£18.9m | SR N/A) | Successfully delivered multiple enterprise AI agents, with circa US$10,000 of revenue recognised from these deployments | ||

Eden Research (LON:EDEN) (£17.8m | SR30) | Company's partner, Véto-pharma, has received regulatory approval from the US Environmental Protection Agency ("EPA") for Thymolflex® for use in integrated Varroa management. | ||

Tanfield (LON:TAN) (£11.2m | SR72) | LBT £1.67m (FY24: £0.27m LBT), Cash & S/T Deposits £2.06m (FY24: £3.21m). |

Backlog sections: DUKE, JDG, SFR.

Backlog

Duke Capital (LON:DUKE)

Down 1.5% today at 25.9p (£132m) - Trading and Operational Update - Graham - AMBER

Let’s catch up on this update from Tuesday:

Duke Capital Limited (AIM: DUKE), a leading provider of hybrid capital solutions for SME business owners in Europe and North America, is pleased to provide guidance on its trading for the fourth quarter of the financial year ending 31 March 2026…

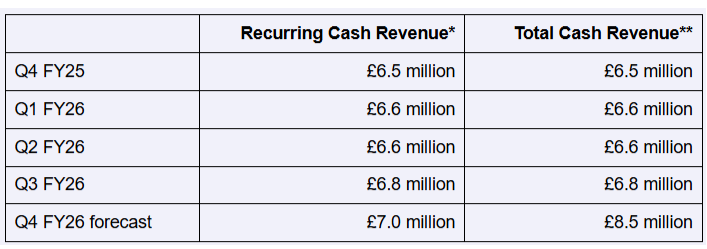

This investor in “royalties” continues to make solid progress, with recurring cash revenue ticking up to £7m in Q4:

“Total cash revenue” includes not just regular royalty income, but also proceeds from disposals.

Total cash revenue this quarter includes defcon received from the sale of street lighting company Fabrikat.

On a £6.2m investment (in 2021), Duke earned £3.2m in royalties and then £11.4m in disposal proceeds (including deferred consideration).

These figures help to remind us of the very high rates charged by Duke: they were only invested in Fabrikat for 3 years - from Feb 2021 to Feb 2024 - and yet they received more than 50% of their money back in royalties during that time.

A snippet from the comment by Duke’s CEO:

"We are delighted to report another record quarter of recurring cash revenue for Q4 FY26, rounding off a strong finish to the financial year. This performance reflects the resilience of our business model in navigating a challenging macroeconomic environment. Whilst the Bank of England's decision to hold rates in March reflects the ongoing uncertainty in global markets, including the situation in the Middle East, our business model has demonstrated its ability to perform across market cycles.

Graham’s view

I’ve highlighted the reference to interest rates as they are key to the story here: Duke’s share price has never recovered since rates began rising at the BOE.

However, the company hasn’t really put a foot wrong. Its investments have been remarkably resilient, with no major blowups and even the occasional profitable exit.

That being said, I do view some of the company’s investments as being inherently very risky - and Mark has noted (here) that a recent follow-on investment seemed to be required to shore up an investee’s finances. So the high returns earned by Duke do reflect what is probably quite high risk.

But it has paid out a stable and attractive dividend stream to investors: 2.8p per share for the last several years.

I don’t personally invest for income. For those who do, I continue to think that this has some merit. I’ll leave our AMBER positioning unchanged to reflect the risks.

Judges Scientific (LON:JDG)

Unch. today at £43 (£286m) - Unaudited Preliminary Results - Graham - AMBER/RED =

Judges Scientific plc (AIM:JDG), a group focused on acquiring and developing companies in the scientific instrument sector, announces its final results for the year ended 31 December 2025.

This also came out on Tuesday.

Judges didn’t try to hide the bad news with their headline:

Disappointing FY25, fundamentals intact, 10% dividend increase

Some financial highlights:

Revenue +9.1%, up 6% organically (or up 2% organically if you exclude the lumpy revenue at subsidiary Geotek).

Order intake down 10% organically (down 6% organically if you exclude Geotek).

The order book falls from 18.7 weeks to 15.7 weeks, using the company’s definition of “organically” (i.e. their businesses acquired prior to 2024).

In other words: while 2025 revenue was not bad, the forward-looking order book has weakened substantially.

This is another area where Trump’s administration has significant influence, due to the Federal Government's scientific research funding. Many of JDG’s companies sell into this research.

Comment by the Deputy Chair of Judges:

"2025 was another difficult year. Despite starting with a solid order book and delivering a Geotek coring expedition in the first quarter, the Group subsequently experienced a stark reduction in order intake in the USA, its largest market, as a result of uncertainties around federal funding for scientific research. Additionally, despite general resilience in industrial-focussed markets, H2 saw reduced investments in offshore wind which previously had been a strong growth driver.

That’s just a recap of what we already knew. And to an extent, so is what follows below, but it would have been nice to hear of some green shoots:

As announced in January, the Group started 2026 with a lower than hoped for order book, continued uncertainty around the timing of a recovery in the US, and no expectation of a coring expedition until early 2027. Notwithstanding this turbulence, the fundamentals of the Group, including resilient profitability and strong cash generation, remain intact.

Despite the difficult short-term outlook, the JDG share price did rise by 4% on Tuesday, when this was released. The Deputy Chair reiterated their conviction that the long-term growth drivers were still intact for the business, and that they would carry on with their existing business model.

The “Retired Chief Executive”, David Cicurel, wrote a very nice letter to his “sometimes patient” shareholders, thanking them for helping to raise the company from an initial market cap of £2m, and praising the Judges culture of “respect, integrity, discipline, frugality, patience, and courage”:

This is tested when the environment is turbulent, but I have every confidence that it will again deliver exceptional growth in the capable hands of the new management team.

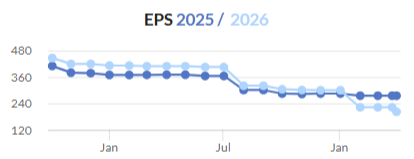

Graham’s view

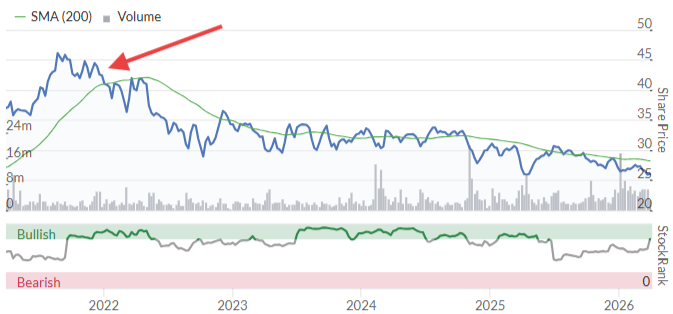

I have plenty of admiration for Judges, and don’t really want to be negative. But we turned AMBER/RED on it recently - at the January profit warning - and not much has changed since then.

EPS forecasts are trending downwards:

And the stock is still trading expensively against these forecasts:

If it was already cheap against forward earnings, I’d be inclined to take our stance back to neutral at the earliest opportunity. But that’s not the case.

There has been a sense of unpredictability around Judges’ results ever since Geotek was acquired, and that unpredictability has been compounded by the Trump presidency and by one or two other more minor issues (e.g. wind farm demand).

There’s a price at which I’d be positive on this stock, and I wish new management every success - but I think caution remains justified.

Severfield (LON:SFR)

Up 3% at 25p on 31st March - Full Year Trading Update - Mark - AMBER

Given the market backdrop this is good news:

FY26 underlying profit before tax expected to be in line with current market expectations of £10.2m

Panmure Liberum worked this out as 2.9p EPS, in line with their previous estimates. However, this doesn’t mean that the company escapes the knife of current market conditions They say:

Accordingly, the Board is adopting a cautious view of the year ahead and now expects FY27 underlying profit before tax to be in the range of £12m-£15m, reflecting increased geopolitical uncertainty, together with broader macroeconomic conditions, the impact of later project start dates, and a continued tight pricing environment.

Which leads PL to cut FY27 forecast EPS is by 27% to 3.6p and FY28 by 22% to 4.7p. So this is a profits warning, although perhaps not an unexpected one. At 24p, the forward P/E is 6.7 for the year just begun, and 5.1x for the year after. If these are achievable this would put the company on a very modest multiple of earnings.

While EPS forecasts are under pressure, there is better news on the debt front which as sizeable for a company with their market cap and EBITDA:

Disciplined cash management during the period providing good liquidity headroom with net debt expected to be ~£28m, lower than current market expectations (Company compiled market consensus: £48.5m), providing year end facility headroom of c.£39m

Liberum forecast this to be partially due to stretching working capital. So I do wonder if this net debt level represents a true position during the year. However, it suggests there is still enough headroom for them to trade as a going concern, which is important in any recovery stock.

Another positive is that they continue to receive insurance payouts for bridge remedial work:

The bridge remedial works programme continues to progress well, with several programmes now complete. Since the half year, the Group has received a further insurance payment of £7.5m, bringing the total amount received to £27.5m. The Group continues to pursue further insurance recoveries and contributions to our costs by third parties. Net costs incurred are expected to be broadly similar to that previously reported.

However, it is worth remembering that the reason they ended up with these payments is that they did work where the steel fabrication did not meet the agreed technical specifications, particularly regarding weld strength and quality, leading to structural integrity concerns. They certainly haven’t covered themselves in glory here, even if they were ultimately insured against these mistakes.

Mark’s view

There still looks to be potential for a recovery here, with cyclically weak market conditions undoubtedly impacting the business. However, that recovery is now forecast to take longer than previously expected. When we last looked at this in December, Roland upgraded this to a neutral view of AMBER on the back of a lack of broker downgrades. With these arriving this week it is tempting to knock this back down again. While nothing is certain at this stage given the impact of higher energy prices and inflation, I feel like the bottom may now be in for forward consensus, and there is a level of conservatism built into these going forwards. If this is true, they trade on a modest forward multiple. Net debt is better than expected which means that they have greater financial flexibility, which means I am willing to take a risk on keeping a neutral stance despite future EPS downgrades this week.

Graham's Section

B.P. Marsh & Partners (LON:BPM)

Unch. at 656p (£236m) - Follow-on equity purchase in Pantheon - Graham - GREEN =

(At the time of writing, Graham has a long position in BPM.)

B.P. Marsh and Partners Plc (AIM: BPM), the specialist private equity investor focused on early-stage financial services businesses, is pleased to announce that it has acquired an additional 2% equity stake in Pantheon, based on an equity valuation of £275m.

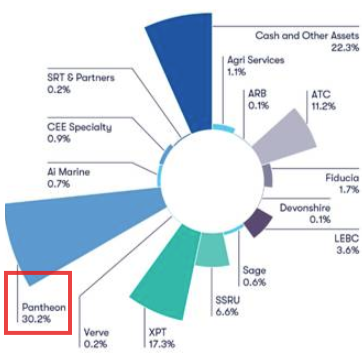

This doesn’t do anything for BPM’s diversification, seeing as Pantheon is already by some distance their largest investment.

As of July 2025, it was 30% of their portfolio (apologies for the fuzzy graphic).

Also worthy of note is that this isn’t growth capital: it’s a purchase from Pantheon’s founders.

If you’re interested to learn more about Pantheon, here’s their website. They are a wholesale broker specialising in complex policies for a range of industries.

Today’s announcement from BPM summarises the achievements at Pantheon since it was launched in 2023, and provides some financial highlights:

Revenue growth from c. £23.8m (FY25) to “approaching £30m” for FY26.

PBT “budgeted to be in excess of £15m” in FY26.

BPM’s initial 25% stake has been increased over time and is now 41%.

Graham’s view

The major downside of this investment is that it maintains BPM’s fairly limited portfolio diversification.

That is a major negative, but I’ve never expected BPM to behave like a mutual fund. It’s a specialist investor and it’s entitled to focus on its best ideas. Sometimes, as with stock market investments, the best ideas are the ones we already own.

Also, BPM has significant cash reserves. As a general principle, I’d rather see the money being put to work rather than sitting idle.

So on balance, I’m comfortable with this news.

Mark's Section

Satsuma Technology (LON:SATS)

Up 5% at 0.2p - Cost Reduction Programme and Bitcoin Purchase - Mark - RED =

This company announces a huge cost cutting program:

…its revised cost reduction strategy that is expected to reduce the Group's annualised operating expenditure from approximately £6.7m to approximately £2.7m, with further reductions expected.

It is not entirely clear what these costs were, or why they were needed (and now not needed). The company reported £2.1m of admin expenses for the 6 month period to 31st August 2025, but no further breakdown was given. This leads me to guess that these costs were mainly salaries to conduct the company's operations.

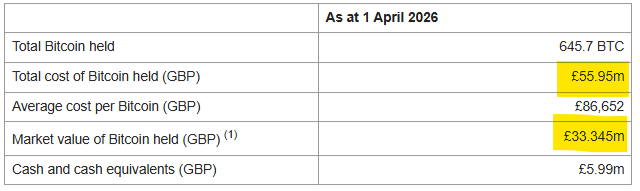

These operations, as far as I can tell, are buying Bitcoin, and we get the announcement today that they have spent another £1.38m buying more from cash reserves.

However, the highly remunerated team appear to be bad at their main endeavour, as a 40% loss of value on their average purchase price shows:

The (only?) interesting part here is that with a market cap of £26.7m, this company now trades at a 32% discount to the £39.3m value of the cash and bitcoin the company holds, which is what piqued my interest.

The problem is that there are no signs of the company liquidating those assets and returning the cash to shareholders. Indeed, they appear to be doubling down on their losing bet and buying more Bitcoin. In this context, the company should trade at a discount to net assets, and that cash balance gives them about 2 years of runway (up from less than 1 year) before they have to start selling assets to fund the corporate structure (or perhaps more realistically, raising money from the market!)

Mark’s view

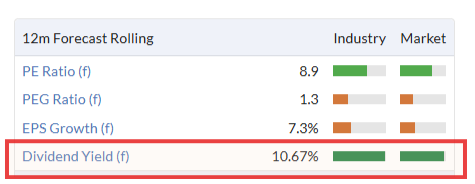

Despite a purported 32% discount to net assets, it will perhaps come as little surprise that I’m negative on a company spending (even a much reduced) £2.7m a year buying Bitcoin. This seems to me like an activity that a man and a laptop could do effectively, spending about 10 mins a year. Not only is this an activity that doesn’t require the corporate overheads of a listed company, but the company appears to be bad at their main activity, having lost an average of 40% on their historical purchases! We’ve been negative here since the middle of last year, and since then, shareholders have lost 98% of the value of their holding. With a StockRank of zero, I remain negative. RED

Tracsis (LON:TRCS)

Flat at 307p - Acquisition - Mark - AMBER =

This acquisition is described as:

Bolt-on acquisition that expands Tracsis' digital ticketing capability and establishes a small operational foothold in the German public transport market

The core product acquired is Mobilitybox, a B2B standardized API platform that acts as a bridge between public transport operators and third-party companies. It allows businesses to integrate live transit data and ticket booking directly into their own applications and websites. For example, it would allow airlines or event organizers to sell "last mile" transit tickets alongside their primary offerings.

While this may be a good strategic fit and expand Tracsis geographically into a large German market, it is not necessarily been a cheap bolt-on. They are paying €5m + up to €2.4m earnout. Tracsis does not give any financial figures for the acquisition. Third party estimates suggest that Vesputi delivered around €1m in revenue in 2025. This appears to be a very significant premium to Tracsis 1.1x price-to-sales ratio. It is hard to estimate profitability, but again this is likely to represent a high multiple paid, especially if the earnouts are triggered.

The acquisition is said to be “Immediately earnings enhancing” which is good to hear, but doesn’t necessarily mean a lot when the acquisition is paid for in cash, which earned an average of 2.8% interest last year. This means that anything less than a 35x earnings multiple paid could be described as earnings enhancing.

The initial consideration paid is less than 5% of the Tracsis market cap so overall this will have a relatively minor impact on the financials. I can’t see any updated broker coverage today, which again suggests minimal financial impact in the forecast window.

Mark’s view

The company has a long history as an acquirer, and for a number of years, shareholders liked the growth story that this brought. However, by 2022 it had struggled with some of the integration efforts and paused acquisitions while it engaged in restructuring. Some have questioned the ability for the company to grow organically and whether they have generated adequate returns on past acquisitions due to the multiples they paid.

Today’s deal is described as a strategic acquisition rather than a bargain purchase. However, it is only a small percentage of the overall market cap of the company, meaning it doesn’t shift the dial much either way. Some will be encouraged by the continued return to acquiring bolt-ons. However, the apparent multiple paid doesn't do much to assuage the concerns of those who think they may have pursued growth at any cost. Overall, I don’t think there is enough in today’s acquisition to change our previously neutral view either way, so I’ll stick with AMBER.

Speedy Hire (LON:SDY)

Down 13% at 19.2p - Trading Update - Mark - BLACK (AMBER/RED ↓)

The tone here reads like a profits warning, even if the company don’t explicitly say this:

At our interim results on 26 November 2025 we anticipated a continuation of subdued market conditions for the remainder of FY2026. Market conditions have worsened through Q4 with uncertainty around the UK Budget in November and the recent geopolitical events in the Middle East. The Group has also seen certain customer led delays, affecting hire and service revenues, which are now expected to impact positively in the near term. As a result the Board now expects FY2026 EBITDA to be c.£90m.

A quick check of the brokers notes confirms this:

Panmure Liberum: We reduce our FY 26 and FY 27 EBITDA by 15% and 12%, and expect a small loss before tax in FY 26

Canaccord: …we cut our FY26E EBITDA estimate by 16% and raise net bank debt by 10%....reduce FY27E/28E EBITDA by 5%/3%.

Both brokers cut FY26 adjusted EPS forecasts to show a loss. This perhaps should not be a surprise as H1 was loss-making and said that H2 trading conditions would be challenging.

Canaccord reduce FY27 EPS from 5.3p to 4.2p. Panmure are more pessimistic, dropping their number from 5.7p to 3.1p. With the share price only down 13% so far, his looks potentially light versus the scale of these EPS revisions. Although, it could be argued that the market was/is already sceptical about these figures. A scepticism I share. Recent events in the Middle East have the potential to lead to continued construction market weakness beyond the financial year just ended.

ProService:

One of the major reasons for this optimism cited by both the company and brokers is the recent Proservice deal. This was a complex deal that involved HSS being rebranded as pro-service and focusing on its digital platform connecting customers with equipment, materials and training. HSS’s physical hire business was sold for a £1 to private equity, and Speedy became preferred supplier for equipment to the ProService marketplace for an initial five-year term in return for a £35m equity injection into the ProService group.

The part I find difficult is that both HSS and Speedy described this deal as a good one for them. It is possible that they were both winners and the Private Equity Group that bought all the HSS hire equipment business for £1 was the loser, but this seems a little far-fetched. Anyway, Speedy are now significantly underwater on their £35m equity investment with the ProService share price following the market down.

Balance sheet:

Yet, this is one of the main reasons Speedy say their net debt has jumped:

Net debt at 31 March 2026 is expected to be c.£159m, including the £35m invested in ProService. The Group expects to see meaningful deleverage in FY2027 as a result of strong operating cash flow.

One of the benefits of this type of company is that in weaker markets, they can simply not buy any new equipment and run the business for cash. So the question is, why haven’t they been doing this in current market conditions?

Brokers still see net debt being high going forward, with Panmure only seeing this figure (which also excludes lease liabilities) dropping to £152m next year. This is still high compared to their earnings and market cap, making this look particularly high risk at the moment.

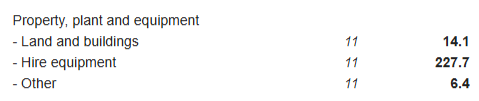

The other side of this equation is the assets. At the half-year, they had £227m of owned hire assets:

So this potentially covers more than the net debt, and is perhaps why the banks appear relatively sanguine. As anyone who has hired equipment will know, depreciation is a real charge here, and the company can only hold off buying new equipment for so long.

And presumably, it's this net asset backing that means the share haven’t fallen further this morning:

However, I have to question how realistic this figure is. It obviously relies on the depreciation policy being correct. Previously, non-itemised assets were depreciated over 15 years. This was reduced to 7 years which seems more realistic. However, there was an issue where these had to be written down in 2023, when roughly 40% of these items were found to be missing. Itemised Hire Assets are typically depreciated over their expected useful lives on a straight-line basis. However, this may overstate the value of recently purchased items, especially if they have high usage.

The company also invested in hydrogen-electric powered access platforms in 2023 and formed a 50-50 JV with AFC Energy for power generators. While we may applaud Speedy for their forward-looking moves, it is not clear to me if this equipment is particularly practical, as the availability of commercial hydrogen is quite limited.

Mark’s view

Given today’s news, there are only two real positives for the company. The first is that they trade at a discount to tangible book value, and the second is the forecast rapid recovery in FY27. They may well look cheap if they hit (much-reduced) forward forecasts. However, I have some significant doubts about both of these.

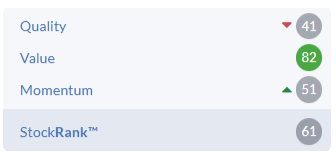

The StockRank isn’t exactly inspiring and will likely look much worse once the FY26 results have been released and incorporated into the StockReport:

So in keeping with the Stockopedia research that suggests negative news tends to be followed by a further drift downwards in share price for some time, I am reducing our view by one notch to AMBER/RED.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.