Good morning! And welcome back after the very long weekend.

The FTSE is opening little changed this morning, around 10,450. Brent Crude appears to have stabilised around $108.

Anecdotally, I had to fill my diesel engine this weekend, for Easter travel, and the rising fuel prices hit home. I think I'm now paying the US equivalent of $8 per gallon. When Americans complain about $4 gas, I must admit to feeling a little jealous.

Trump's threats against Iranian power infrastructure (and bridges) continue, but it looks like the financial markets have at this stage become immune to them.

Wrapping up the report there as it's a light day for news. See you tomorrow!

Spreadsheet accompanying this report: link.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

JTC (LON:JTC) (£2.3bn | SR39) | Revenue +25.1%, driven by net organic growth 8.5% and M&A. Underlying operating profit +22%. In January, shareholders approved the takeover of JTC at £13.40 per share. | PINK (takeover by Permira) | |

Volex (LON:VLX) (£887m | SR84) | Launch of £40 million share buyback programme & Update on Move to the Main Market | £40m share buyback to reduce share capital: all shares repurchased will be cancelled. Confirms intention to move to LSE’s Main Market. | |

Hunting (LON:HTG) (£753m | SR89) | Orders totalling $63.5 million for HTG’s titanium stress joint product line, for a new offshore development in Guyana. Will be delivered through May 2028. “...Contributes to our guided subsea product group revenue and EBITDA through to 2028.” (GN: shouldn’t change expectations.) | AMBER = (Graham) [no section below] Thanks to Zeus for publishing on Hunting today, but the main takeaway is that today’s announcement makes zero change to Hunting’s forecasts. Zeus note that Hunting’s order book fell from $509m (Dec 2024) to $358m (Dec 2025), and yet forecasts suggest higher revenues in 2026 vs. 2025. Hitting forecasts will therefore require additional contract awards over the coming months - and so Roland’s comments last month on the risk of a shortfall remain relevant. Additionally, the valuation of 15x forward earnings is punchy against both oil services companies and the wider market. | |

Caledonia Mining (LON:CMCL) (£349m | SR79) | 10,311.9 metres of deep level drilling completed between March and December 2025. CEO comment: "The latest results from our deep drilling programme reinforce the geological strength of Blanket Mine and demonstrate the continuity of mineralisation at depth across multiple orebodies.” | ||

Beeks Financial Cloud (LON:BKS) (£107m | SR18) | Proximity Cloud contract with a large foreign exchange broker. £2.1m value. | AMBER/RED = (Graham) [no section below] I’m always a little cynical when it comes to announcements like this. The £2.1m contract announced today is to be delivered over five years, i.e. £400k/year. Beeks is generating annual revenues of £40m+. So the contract is worth 1% of forecast revenues (if even that). I can see that it demonstrates an existing customer who is satisfied with the service and is happy to expand their relationship with Beeks, but it just doesn’t strike me as material. Roland covered the company’s interim results in detail last month; I’ll leave our moderately negative stance unchanged for now. | |

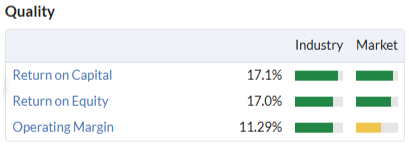

MTI Wireless Edge (LON:MWE) (£50m | SR98) | Multiple orders totaling c. US$6m. CEO: “...the volume of orders significantly enhances our order book for FY 26 and FY 27…" | AMBER/GREEN = (Roland) This update sounds positive, but these orders are due for delivery over two years and there is no change to broker forecasts today. While this defence-focused Israeli business is undoubtedly enjoying tailwinds from the current geopolitical situation, my feeling is that these orders are largely priced into existing forecasts. That said, my view of this business remains favourable and I don’t see any reason to change our previous broadly-positive view today. | |

Victoria (LON:VCP) (£47m | SR26) | Agreed the sale to a property investor for a gross consideration of €34.4m, in line with the company’s expectations. This compares to a net book value of €5.6m as of Jan 26. Tax losses will be used to mitigate capital gains. | RED = (Graham) I think it’s correct for the market to price these shares as options - they could multibag from here if the company finds the escape hatch, but if it doesn’t then they are worthless. Accordingly I remain RED on Victoria. | |

One Health (LON:OHGR) (£34m | SR73) | Renewed contract with Sheffield Teaching Hospital for three years, rather than renewing annually as previously. Together with two previous five-year renewals in 2024, this contract now covers c.80% of One Health’s activity. | ||

Lords Trading (LON:LORD) (£29m | SR51) | Has refinanced the group’s existing £75m lending facilities. These have been replaced with new 3yr £65m facilities, consisting of an RCF and receivables financing facility, as previously. Expected to result in “material interest cost savings” for the Group. | ||

Haydale (LON:HAYD) (£22m | SR3) | Has expanded its SaveMoneyCutCarbon platform partnership with Wave Utilities. The expanded agreement is expected to generate “at least £1.0m of recurring programme-based revenue annually” with a pipeline of further opportunities. | ||

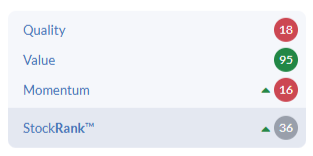

Facilities by ADF (LON:ADF) (£12m | SR36) | Entered into new 3yr £5m RCF with HSBC to replace existing £1m overdraft. Has also raised £650k through a 60-month asset financing facility secured against certain existing assets within the ADF fleet. Finally, ADF has extended a number of existing finance leases for a further 24 months for an annualised cash flow benefit of c.£800k. | AMBER/RED = (Roland) The refinancing activities reported today may improve ADF’s near-term ability to meet its financial obligations, but I would guess this will come at a cost to future profitability. The StockRanks see this as a Value Trap and without any evidence of improved revenue or margin performance, I am inclined to agree. I’ve left our AMBER/RED view unchanged ahead of the group’s full-year results, which I expect in May. | |

Hydrogen Utopia International (LON:HUI) (£11m | SR13) | Received a proposed letter of intent from a Polish energy company regarding “potential cooperation for the roll out of waste plastic to hydrogen facilities in Poland”. Has requested a licence from Powerhouse Energy (LON:PHE) to promote its DMG technology in selected European markets. | ||

Zinc Media (LON:ZIN) (£10m | SR31) | Recommissioned by BBC for a second series of quiz show The Celebrity Inner Circle (8x45’ episodes). | AMBER/RED = (Graham) [no section below] It has been a long time - well over a decade - since this company generated meaningful profits. Management are currently targeting £5m of EBITDA on £50m of revenues over the medium-term - but the track record of converting EBITDA into real profits is patchy, so I’m not even sure what £5m of EBITDA would be worth. The interim results last year showed £0.9m of adjusted EBITDA converting to adjusted PBT of around breakeven, and there was a statutory loss. Also, the net cash balance remained thin at <£1m. Today’s contract announcement is for 8 episodes of a BBC quiz show, up from 6 episodes in the first series, which will hopefully translate into slightly higher revenues, but I’m inclined to leave our moderately negative stance unchanged for the time being | |

Medpal AI (LON:MPAL) (£10m | SR1) | Prescriptions dispensed have risen from zero in October ‘25 to 41.6k in March (+27.5% vs Feb). Now exceed £5m in annualised turnover, based on March volumes. Gross margin exceeded 34% in March. Continued strong demand for GLP-1 weight-loss treatments. |

Graham's Section

Victoria (LON:VCP)

Up 2% at 41.73p (£48m) - Sale and Leaseback of Belgian Distribution Centre - Graham - RED =

I’ve been calling this one “a probable zero” due to the horrendous balance sheet situation.

The company has today announced the sale and lease back of a distribution centre, which will remain in use by Balta Rugs.

Amount raised: €34.4m

Net book value of the properties: €5.6m, implying hefty capital gains

Existing losses to be used to mitigate CGT.

However, the amount raised isn’t large enough to make any huge change to Victoria’s overall financial situation, and it’s not really designed to. It’s more about offsetting some exceptional costs as Balta Rugs relocates its manufacturing operations to Turkey.

Exec Chairman Geoff Wilding:

The net cash proceeds will initially be retained on the Company balance sheet. Alongside two additional surplus property disposals, the proceeds are expected to fully fund the exceptional costs and capital expenditure associated with the transfer of manufacturing to Turkey.

Graham’s view

Moving some manufacturing to Turkey will reduce costs, but this doesn’t change the overall picture.

In February I covered a profit warning from Victoria which saw EBITDA expectations cut from £110.7m to c. £95m.

The interim report from the company disclosed negative equity of over £400m, or over £600m excluding intangibles. There are €167m of Senior Notes maturing in 2028, and then over €600m of bonds maturing in August 2029.

So I think it’s correct for the market to price these shares as options - they could multibag from here if the company finds the escape hatch, but if it doesn’t then they are worthless. Accordingly I remain RED on Victoria.

Roland's Section

Facilities by ADF (LON:ADF)

Up 1.5% at 11.7p (£12.6m) - RCF, Asset Financing and Lease Extensions - Roland - AMBER/RED =

ADF is one of the leading suppliers of production facilities to the UK film and television industry. Unfortunately this hasn’t been a particularly strong market to be in over the last couple of years. ADF’s last trading update revealed that it was cutting headcount and trimming its asset base.

Today we learn that the company has borrowed money against some of its existing fleet assets and taken other steps to improve short-term liquidity.

Refinancing - main points:

New three-year £5m revolving credit facility with HSBC replaces a previous £1m overdraft;

The group has borrowed £650k through a 60-month asset financing facility secured against certain existing assets within its fleet;

Some existing finance leases have been extended by 24 months, providing an expected annualised cash flow benefit of c.£0.8m.

I assume that lender HSBC must have some confidence in the medium-term outlook for ADF if it’s willing to extend a much larger overdraft facility to the company than previously.

However, the company’s decision to borrow against existing fleet assets and extend some of its leases suggests to me that management is in the unenviable position of having to sacrifice future profitability to support short-term cash flow.

Today’s RNS refers to the assets on which new financing has been secured as fleet assets – presumably this means vehicles, trailers or other equipment from ADF’s hire fleet that was previously unencumbered. Such assets are all depreciating assets, so borrowing against them today means any potential future cash flow from their disposal is likely to be much reduced. Similarly, additional borrowing costs will eat into future profits.

Equally, extending existing finance leases may reduce near-term cash outflows, but presumably comes at the cost of increasing total lifetime lease payments or perhaps operating ageing assets that would previously have been replaced.

Leverage concerns? The company makes no comment on its existing net debt or gearing levels today, but does reiterate its target of achieving leverage “in the range 1.0 - 1.5x adjusted EBITDA through the business cycle”.

For some context, September’s half-year results for the period ending 30 June ‘25 showed net debt of £13.2m and a leverage ratio of 1.9x EBITDA.

November’s trading update showed net debt had increased to £13.8m and indicated forecast 2025 adjusted EBITDA of £10.0m – potentially suggesting leverage of 1.4x EBITDA.

Trading & outlook

There’s no commentary on trading today but ADF’s last update in November indicated that 2025 results were expected to be “broadly in line with market expectations” – i.e. slightly below.

Mark commented on this update and noted that house broker Cavendish had slashed earnings forecasts by 39%. This followed another big profit warning early in 2025:

Roland’s view

ADF recruited a new CFO in December and I would speculate that he has concluded the company needs more near-term liquidity than was previously available.

These changes may flatter EBITDA and should improve the company’s ability to meet near-term obligations and service debt. However, I don’t think they will do much to improve bottom-line profits.

As we’ve commented before, we don’t see EBITDA as a very meaningful measure of profitability for equipment hire companies with high levels of Interest and Depreciation and assets that need regular replacement.

ADF’s share price is broadly unchanged today and the stock does look superficially cheap:

However, I would guess that a dividend cut is a near certainty this year, perhaps even a suspension.

I would also be reluctant about attaching too much significance to the stock’s low earnings multiple and price to tangible book ratio.

I’m going to leave our AMBER/RED view unchanged today ahead of the group’s full-year results, which are expected in May. ADF fits our Value Trap criteria, looking cheap but with low scores for both quality and momentum.

The problem with Value Traps is that they often lack the necessary catalyst for a recovery and re-rerating. In this case, I’d be looking for evidence of renewed revenue growth and/or a recovery in margins to justify a more positive view.

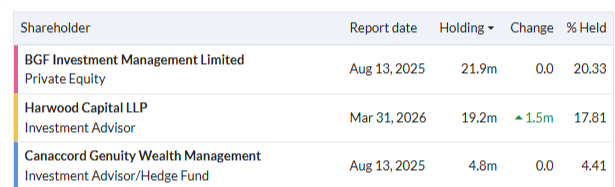

However, it’s possible that I’m being too pessimistic; I see that Harwood Capital has become a major shareholder here, recently adding to its position.

ADF shares were trading at over 50p less than 18 months ago. If 2026 brings evidence of a recovery then this might be a good time to start taking a closer look.

An investor with an insight into the current state of the UK film and television industry could have a legitimate edge when analysing this situation – if you are that person, please feel free to share your thoughts in the comments below.

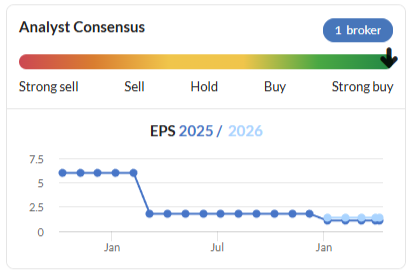

MTI Wireless Edge (LON:MWE)

Up 8.5% at 61p (£53m) - Multiple contract wins worth c. US$6m - Roland - AMBER/GREEN =

A series of primarily defence sector orders received equivalent to over 10% of FY 25 annual revenues

Mark commented on the 2025 results from this Israel-based technology group in early March, maintaining our AMBER/GREEN view. He concluded that defence spending drove last year’s growth and that this was likely to continue, given the macro backdrop.

Today’s update confirms this with details of a number of new orders totalling $6m for delivery in 2026 and 2027. They include:

A $2.2m contract for the PSK subsidiary to supply communications infrastructure to Israel’s Ministry of Defence.

A $1.9m contract to supply military antennas to “an international defence company”.

A $0.5m contract for military attenas from “a local defence company”.

Additional orders totalling $1.3m for MTI Summit to supply components “primarily to a defence company”. MTI Summit is a distributor.

CEO Moni Borovitz comments:

Importantly, every order is from an existing customer reflecting the confidence they have in our solutions and ability to deliver. Overall, the volume of orders significantly enhances our order book for FY 26 and FY 27 and supports our ability to continue to grow our business.

Outlook: broker forecasts unchanged

Today’s RNS trumpets that these orders are equivalent to more than 10% of last year’s revenues, but this seems like spin to me.

Today’s contract wins will be delivered over two years and there are no changes to broker forecasts for 2026 or 2027 today, according to house broker Shore Capital. In other words, I would assume these wins are largely priced into existing forecasts.

Roland’s view

It is no surprise to see a technology company that derives much of its revenue from the Israeli defence sector doing well currently.

I have owned MTI shares in the past and would describe this family business as well-run, with a strong balance sheet and attractive profitability.

At the same time, MTI is also a family-controlled AIM stock that’s based in an overseas jurisdiction. While geopolitical conditions are favourable at the moment – and will perhaps remain so for some time yet – the company’s governance and non-UK location mean that I would be reluctant to pay a high earnings multiple for this business.

The current valuation looks reasonable to me, noting that earnings growth is currently expected to be limited this year:

I would guess that there is also some scope for further upgrades to expectations this year. This could justify a further re-rating:

My view of this business remains broadly favourable. I don’t see any reason to change our AMBER/GREEN view today.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.